- Qualcomm is facing a global shortage of memory chips that is limiting smartphone production and weighing on its latest outlook.

- A surge in demand from AI data centers has tightened supply, with cell phone makers in particular in China canceling orders and adjusting inventory plans.

- In response, Qualcomm is placing greater emphasis on areas such as automotive, IoT, robotics, data center solutions, and AI-enabled devices to expand its revenue base.

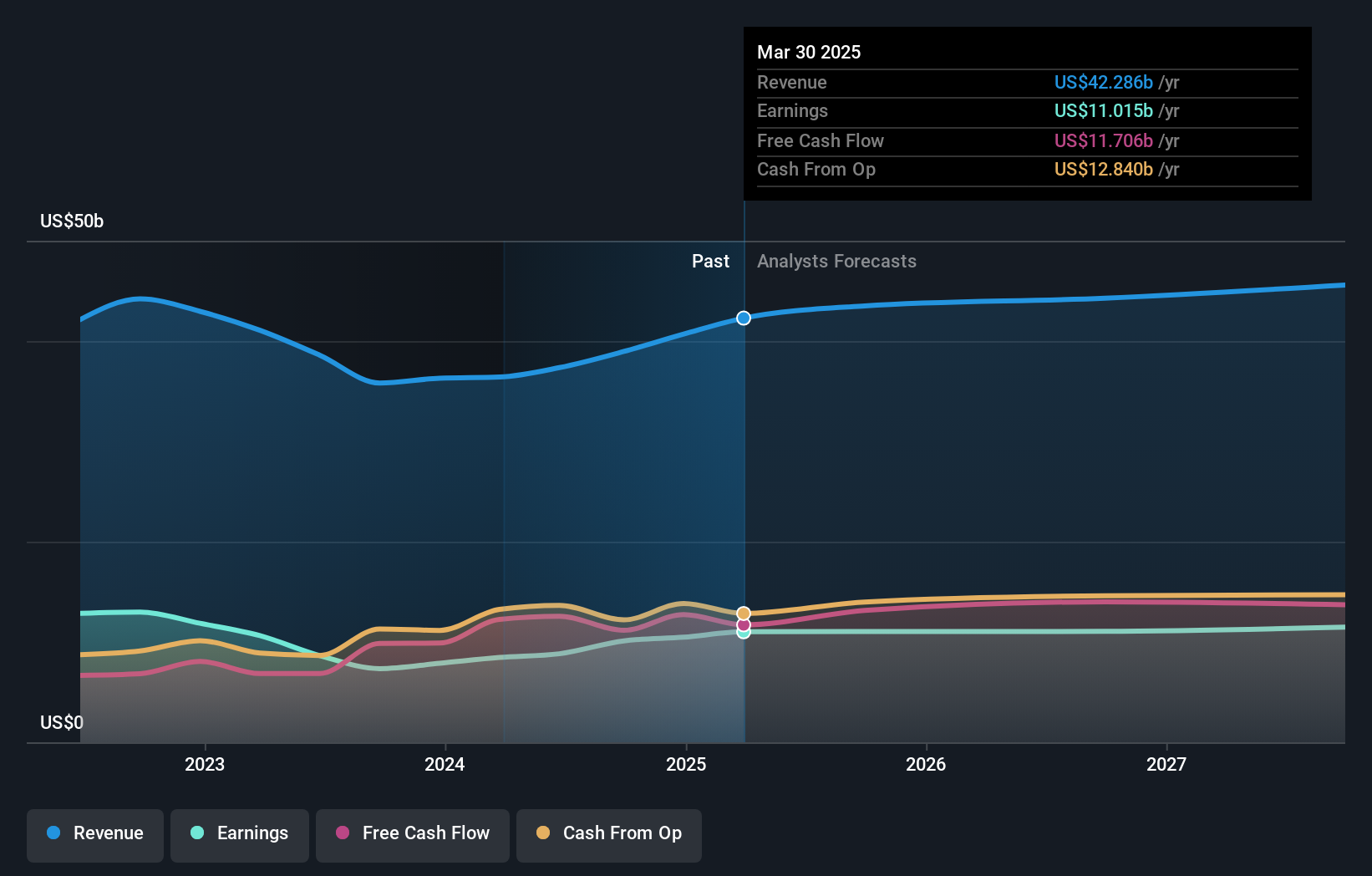

NasdaqGS:QCOM is currently trading at $137.34, and the stock has returned 14.0% over three years and 3.4% over five years. Recently, the stock has fallen 9.4% over the past week, 22.7% over the last month, and 20.6% year-to-date, reflecting pressure from supply constraints and accommodative guidance related to the mobile device market.

The key questions for you as an investor are how much the memory chip shortage will impact Qualcomm’s smartphone-related revenue, and how quickly new revenue streams in automotive, IoT, robotics, data center solutions, and AI-enabled devices will expand. The company is expanding its partnerships with global automakers and working on RISC V and data center technologies. This points to a broader business mix that is less dependent on mobile phone cycles over time.

Stay up to date with Qualcomm’s most important news stories by adding them to your watchlist or portfolio. Or explore our community and discover new perspectives on Qualcomm.

How Qualcomm stacks up against its biggest competitors

quick evaluation

- ✅ Price and analyst targets: At $137.34 versus the consensus target of $163.31, the price is about 19% below what analysts are modeling.

- ✅ Simply Wall Street Ratings: The stock is listed as trading 11.1% below its estimated fair value and is considered undervalued.

- ❌ Recent momentum:The 30-day return has fallen by approximately 22.7% as the chip shortage worsens, indicating weakness in short-term sentiment.

Check out Simply Wall St’s detailed valuation analysis for Qualcomm.

Key considerations

- 📊 This supply shock is mainly weighing on mobile phone-related revenues, while management is focusing more on automotive, IoT, data center, and AI products.

- 📊 Keep an eye on how the revenue share evolves away from smartphones, the trend in margins compared to last year’s 25.8%, and whether the Forward P/E of around 15.9 is lower than the industry’s P/E of around 44.

- ⚠️ Profit margin is 11.96%, lower than last year, so prolonged stockouts could push profit margin below the industry average of approximately 15.45%.

dig deeper

For the complete picture, including more risks and rewards, check out our complete analysis of Qualcomm.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

Evaluation is complex, but we will simplify it here.

Discover whether Qualcomm is undervalued or overvalued with our in-depth analysis. Fair value estimates, potential risks, dividends, insider transactions, and financial condition.

Access free analysis

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.