Report Overview

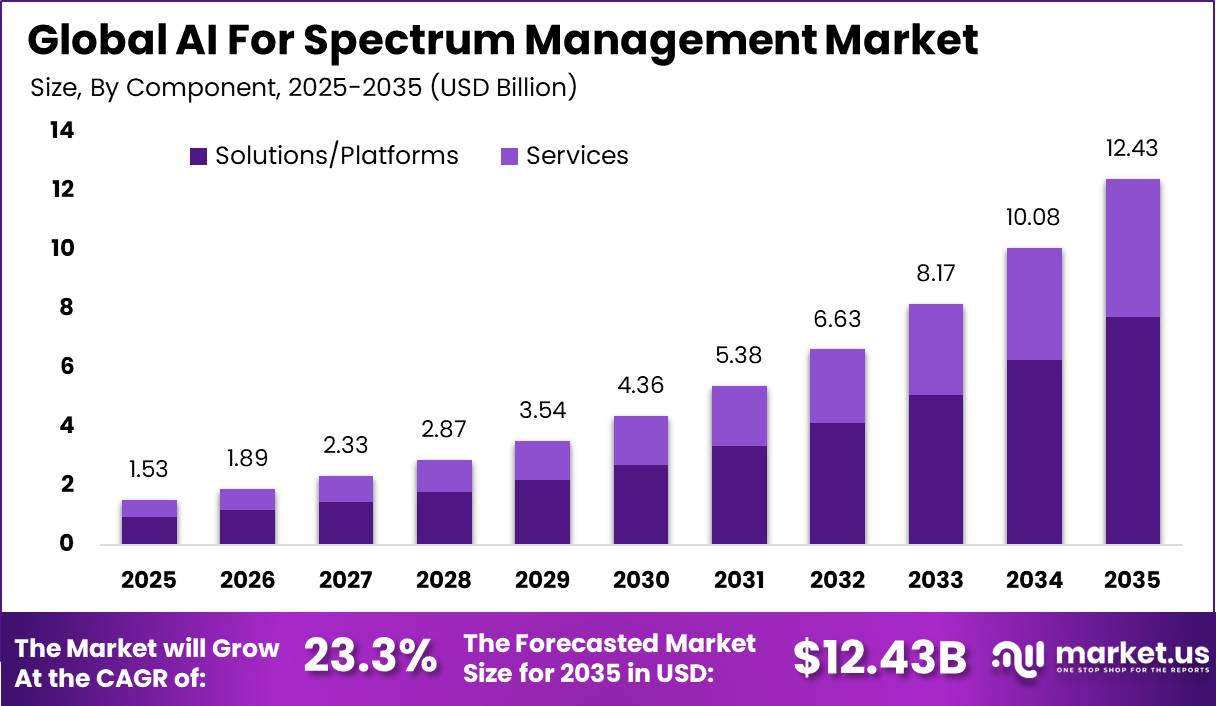

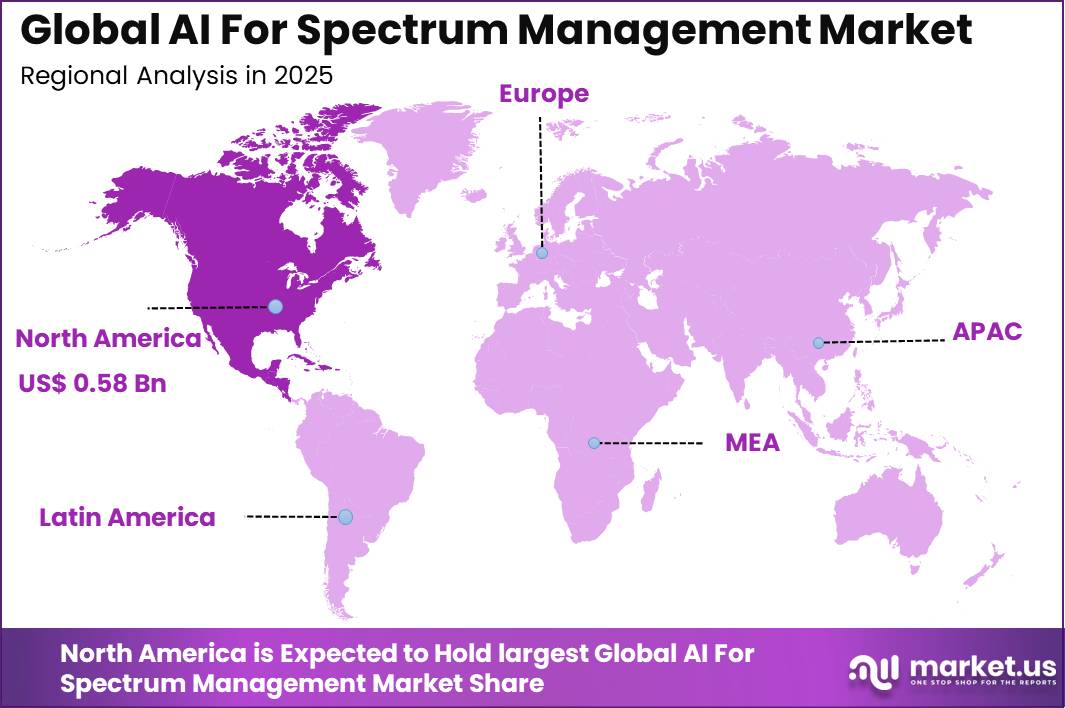

The Global AI For Spectrum Management Market size is expected to be worth around USD 12.43 billion by 2035, from USD 1.53 billion in 2025, growing at a CAGR of 23.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 38.3% share, holding USD 0.58 billion in revenue.

AI for Spectrum Management refers to the use of artificial intelligence to monitor, analyse, and optimize radio frequency spectrum. It helps operators and regulators detect interference, predict demand, allocate channels, and improve network performance. This technology supports better spectrum use across telecom, defense, public safety, and private wireless networks.

Top driving factors include the sharp growth in connected devices, tighter quality of service targets, and wider use of dynamic sharing across licensed and unlicensed bands. AI models can scan large radio environments, detect underused channels, and adjust allocations within 1 to 2 seconds, helping reduce dropped connections and improve user experience in dense urban areas.

The market for AI for Spectrum Management is driven by rising wireless data traffic, growing connected devices, and increasing pressure on limited spectrum resources. Telecom operators and regulators are adopting AI to monitor usage, reduce interference, and improve allocation decisions. The expansion of 5G, private networks, industrial IoT, and critical communication systems further supports demand for smarter spectrum management tools.

Demand is increasing as operators seek higher throughput, lower latency, and stronger coverage without always purchasing new spectrum blocks. Trials show AI-driven spectrum control can raise average cell throughput by double-digit percentages and cut interference probability by several percentage points, supporting data-heavy services such as video, smart factories, and industrial IoT applications.

For instance, in February 2026, Huawei sharpened its AI spectrum‑automation message in global 5G deployments, promoting machine‑learning engines that continuously retune carriers and bandwidth per cell load. The approach is aimed at dense urban networks, where small efficiency gains in mid‑band and C‑band spectrum can translate into double‑digit capacity improvements.

Key Takeaway

- In 2025, the Solutions/Platforms segment held a dominant market position, capturing a 62.3% share of the Global AI for Spectrum Management Market.

- In 2025, the Machine Learning & Deep Learning segment held a dominant market position, capturing a 50.8% share of the Global AI for Spectrum Management Market.

- In 2025, the Spectrum Monitoring & Analytics segment held a dominant market position, capturing a 27.4% share of the Global AI for Spectrum Management Market.

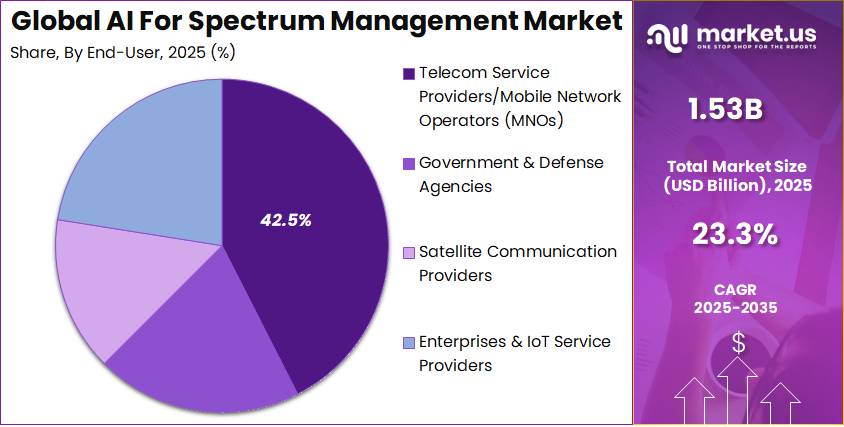

- In 2025, the Telecom Service Providers / Mobile Network Operators (MNOs) segment held a dominant market position, capturing a 42.5% share of the Global AI for Spectrum Management Market.

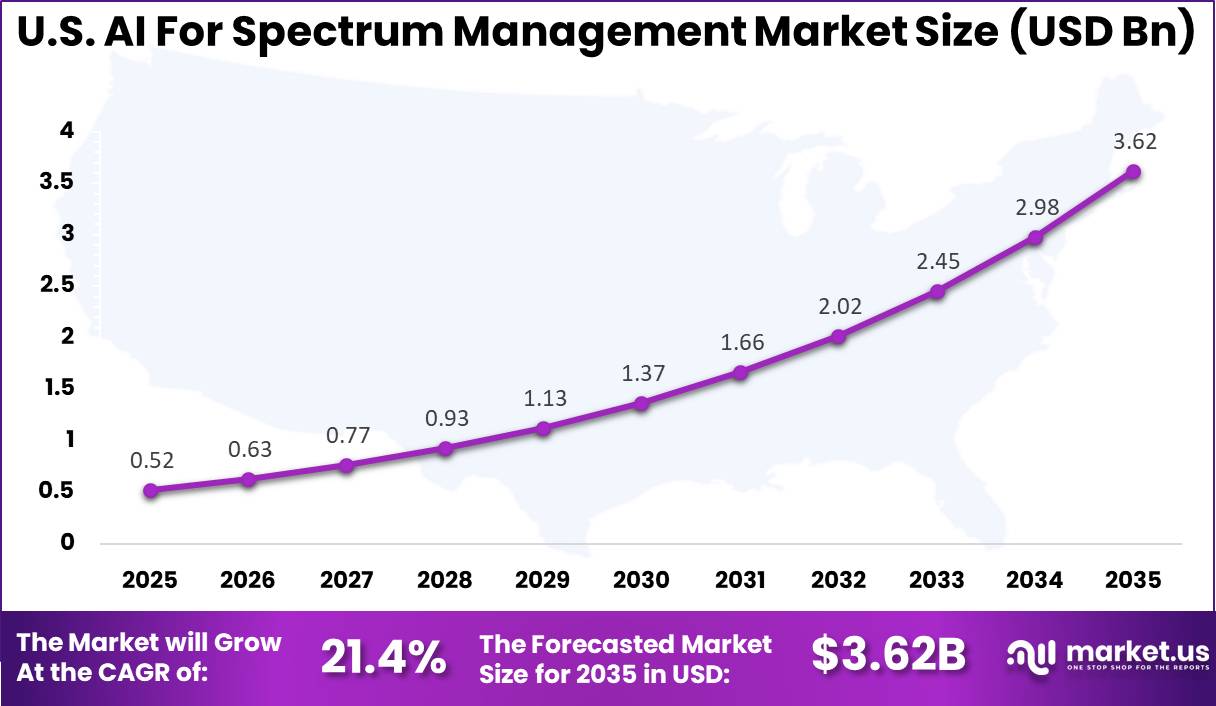

- The U.S. AI for Spectrum Management Market was valued at USD 0.52 Billion in 2025, with a robust CAGR of 21.4%.

- In 2025, North America held a dominant market position in the Global AI for Spectrum Management Market, capturing more than a 38.3% share.

Role of Generative AI

Generative AI is becoming important in spectrum management as networks face rising data use and complex radio conditions. AI-driven spectrum systems can push spectrum utilization close to 90% in simulated cognitive radio networks, helping operators predict demand, recommend channel plans, and reduce interference more effectively than static methods.

It also supports automation in planning and network operations. Learning-based methods can improve throughput and lower interference probability when compared with fixed thresholds. With generative traffic prediction, base stations can schedule users more efficiently, helping save energy, improve spectrum use, and support better decisions on bands, refarming, and sharing schemes.

Investment and Business Benefits

Investment opportunities are emerging in AI platforms for dynamic spectrum sharing, cloud and edge-based spectrum analytics, and sensing infrastructure that feeds learning models. Early-stage capital is moving toward tools for private networks, defense communications, and critical infrastructure, where even single-digit percentage gains in spectrum efficiency can create strong commercial and operational returns.

Business benefits include lower operating costs through automation, fewer manual planning cycles, and better use of towers, backhaul, and licensed bands. AI-driven monitoring can also reduce regulatory penalties by identifying possible violations early and maintaining clear audit trails, which strengthens compliance management and improves trust with national spectrum authorities.

U.S. AI For Spectrum Management Market Size

The market for AI For Spectrum Management within the U.S. is growing tremendously and is currently valued at USD 0.52 billion. The market has a projected CAGR of 21.4%. The market is growing due to rising pressure on U.S. telecom networks, wider 5G deployment, and increasing demand for efficient use of licensed and shared spectrum. Operators are using AI to improve spectrum monitoring, reduce interference, and support faster network decisions. Growth is also supported by defense communication needs, private wireless networks, and regulatory focus on smarter spectrum use across commercial and critical infrastructure applications.

For instance, in February 2026, Cisco showcased new AI-native networking capabilities at Mobile World Congress 2026, helping operators build intelligent mobile cores and RAN transport that dynamically allocate spectrum and capacity for 5G and pre‑6G services, reinforcing U.S. leadership in AI‑driven spectrum management infrastructure.

In 2025, North America held a dominant market position in the Global AI For Spectrum Management Market, capturing more than a 38.3% share, holding USD 0.58 billion in revenue. This dominance is due to strong telecom infrastructure, early 5G adoption, and rising investment in AI-enabled network optimization across the U.S. and Canada. North America also benefits from active spectrum modernization efforts, private wireless network expansion, and strong demand for reliable connectivity in defense, public safety, industrial, and enterprise sectors. The presence of advanced cloud, edge computing, and analytics capabilities further supports AI-based spectrum management adoption.

For instance, in September 2025, Keysight Technologies expanded its AI‑enhanced spectrum monitoring and signal intelligence tools for North American operators and defense agencies, using machine learning to detect interference, classify emitters, and validate dynamic spectrum sharing schemes across crowded mid‑band frequencies.

Component Analysis

In 2025, the Solutions/Platforms segment held a dominant market position, capturing a 62.3% share of the Global AI for Spectrum Management Market. This dominance is due to the rising need for integrated solutions that can manage monitoring, analytics, allocation, and compliance from one place. Solutions and platforms help operators handle complex radio environments with better visibility, faster decisions, and reduced manual effort across network planning and spectrum operations.

These platforms are also preferred because they can connect with existing network systems and support automated workflows. As spectrum environments become more crowded, organizations need flexible tools that can identify interference, track usage patterns, and improve spectrum efficiency without depending only on traditional planning methods.

For Instance, in February 2026, Ericsson introduced AI-ready radios and RAN software that use built-in intelligence for real-time optimisation of radio resources across wide bands. The launch focused on improving coverage prediction and dynamic beam management, laying the groundwork for more automated spectrum handling in 5G and future networks.

Technology Analysis

In 2025, the Machine Learning & Deep Learning segment held a dominant market position, capturing a 50.8% share of the Global AI for Spectrum Management Market. Machine learning and deep learning lead this segment because they can analyse large radio datasets and identify patterns that are difficult to detect manually. These technologies support spectrum sensing, traffic prediction, interference control, and smarter allocation, making them highly useful for modern wireless networks.

Their adoption is further supported by the need for faster and more accurate network decisions. Telecom operators and regulators use these models to improve spectrum planning, reduce signal conflicts, and support dynamic sharing across different frequency bands, especially in dense and high-demand network areas.

For instance, in April 2026, Cisco detailed how its new networking platform applies machine learning to predict congestion and steer traffic across different paths before issues appear. The same modelling helps customers map wireless capacity needs and avoid hotspots, indirectly improving spectrum utilisation at the edge.

Application Analysis

In 2025, the Spectrum Monitoring & Analytics segment held a dominant market position, capturing a 27.4% share of the Global AI for Spectrum Management Market. Spectrum monitoring and analytics hold a strong position because operators and regulators need clear visibility into how spectrum is being used. These tools help detect interference, monitor occupancy, and identify abnormal signal activity, which supports better planning and more reliable wireless service delivery.

The segment is also gaining importance as networks become more complex and data traffic continues to rise. AI-based analytics can support faster issue detection, improve spectrum utilization, and help decision makers understand usage trends before they affect network quality or customer experience.

For Instance, in March 2026, Huawei showcased solutions that collect radio performance data and run intelligent analysis to guide network tuning, particularly in the upper mid-band range. The company emphasised closed-loop control, where monitoring outputs instantly informs decisions on scheduling and channel use.

End-User Analysis

In 2025, the Telecom Service Providers / Mobile Network Operators (MNOs) segment held a dominant market position, capturing a 42.5% share of the Global AI for Spectrum Management Market. Telecom service providers and mobile network operators lead this segment because they manage large networks with heavy traffic, limited spectrum resources, and strict service quality needs. AI helps them improve capacity, reduce interference, and make better use of available licensed and shared bands.

Their demand is also driven by the shift toward advanced mobile networks, private connectivity, and high-bandwidth services. With AI-based spectrum tools, operators can strengthen coverage, improve network reliability, and reduce the pressure of manual spectrum planning across dense urban and enterprise environments.

For Instance, in May 2026, Nokia described a strategic shift towards AI-driven network infrastructure, pointing to demand from operators that want more automation across their assets. Using AI to tune radio, transport, and core helps telecom customers stretch existing spectrum resources while planning for future bands.

Emerging trends

A key trend is real-time AI-driven spectrum allocation for advanced 5G and 6G networks. Research on reinforcement learning and federated learning shows sub-millisecond allocation decisions in simulations. Multi-agent systems are also improving convergence stability and spectrum utilisation compared with static policies or single-agent control.

Another trend is the rise of end-to-end spectrum management assistants. These tools are moving beyond frequency planning to support licensing workflows, band sharing reviews, and economic cost-benefit analysis. AI is also being used for interference risk scoring, cross-border coordination, and data-driven consultation with stakeholders.

Growth Factors

Growth is supported by rising wireless demand and new services that need lower latency and stronger reliability. Policy discussions increasingly connect future AI leadership with access to suitable spectrum and reliable wireless infrastructure. As 5G expands and 6G research advances, manual monitoring and static allocation are becoming less practical.

Adoption is also helped by better algorithms, open datasets, and computing platforms built for radio networks. Research shows growing use of reinforcement learning, deep learning, and generative models for dynamic access, sensing, and interference management. Energy-efficient AI is also becoming important as spectrum decisions move closer to the radio edge.

Key Market Segments

By Component

- Solutions/Platforms

- Dynamic Spectrum Sharing/Scheduling

- Spectrum Monitoring & Sensing

- Interference Detection & Mitigation

- Spectrum Forecasting & Analytics

- Radio Frequency (RF) Planning & Optimization

- Services

- Professional Services

- Consulting

- System Integration

- Support & Maintenance

- Managed Services

- Professional Services

By Technology

- Machine Learning (ML) & Deep Learning

- Natural Language Processing (NLP)

- Computer Vision

- Others

By Application

- Spectrum Monitoring & Analytics

- Interference Mitigation

- Dynamic Spectrum Access/Sharing

- Spectrum Forecasting & Planning

- Network Optimization

- Others

By End-User

- Telecom Service Providers/Mobile Network Operators (MNOs)

- Government & Defense Agencies

- Satellite Communication Providers

- Enterprises & IoT Service Providers

Drivers

Surge in Wireless Data and Connected Devices

The market is driven by the rapid rise in wireless data traffic and connected devices. Telecom networks are handling heavier demand from smartphones, IoT systems, video services, and industrial applications. AI helps operators use available spectrum more efficiently by identifying congestion, reducing interference, and supporting faster allocation decisions.

The need for better network quality is also increasing adoption. As users expect stable coverage and low latency, operators are turning to AI-based spectrum tools to improve planning and real-time monitoring. This helps reduce service disruption and supports stronger performance across dense urban, enterprise, and critical communication environments.

For instance, in March 2026, Ericsson discussed AI‑powered receivers that improve spectral efficiency by learning from complex radio conditions, helping operators handle rising data traffic without constantly adding new spectrum. This supports more stable mobile broadband as connected devices and 5G fixed wireless lines grow in number.

Restraint

Data and Integration Barriers

Data and integration barriers remain a major restraint for the market. AI tools need clean, timely, and consistent spectrum data to deliver accurate decisions. Many operators and regulators still depend on legacy monitoring systems, fragmented databases, and different technical standards, which makes smooth implementation difficult.

Integration also becomes complex when AI platforms must connect with existing radio equipment, licensing systems, and network management tools. Poor data quality can reduce model accuracy, while system gaps may slow automation. This creates a higher deployment effort and limits adoption among organizations with older infrastructure.

For instance, in February 2025, IBM’s report on cloud and AI for telecom networks underlined that many operators still struggle with fragmented data and legacy systems when they try to deploy AI. For spectrum management use cases, this kind of fragmentation slows training, limits visibility, and complicates integration of AI insights.

Opportunities

Smarter Spectrum Sharing

Smarter spectrum sharing is creating a strong opportunity for AI-based platforms. As demand for wireless capacity grows, regulators and operators need better ways to share bands without causing harmful interference. AI can analyse usage patterns, predict congestion, and recommend more flexible allocation across commercial, enterprise, public safety, and defense networks.

This opportunity is also supported by the rise of private networks, industrial IoT, and future 6G planning. AI can help improve coordination between licensed, unlicensed, and shared bands. This makes spectrum use more flexible and helps stakeholders improve capacity without depending only on new spectrum availability.

For instance, in June 2025, Nokia introduced Autonomous Network Fabric, a suite of telco trained AI models that can observe network traffic patterns and adjust resources. This type of AI fabric provides a foundation for more dynamic spectrum use, where allocation decisions respond quickly to changing local demand.

Challenges

Trust and Regulatory Acceptance

Trust and regulatory acceptance remain key challenges for the market. Spectrum is a sensitive public resource, so regulators and operators need clear proof that AI decisions are reliable, explainable, and safe. Automated recommendations must be tested carefully before they are used in allocation, monitoring, or interference control.

Adoption may also slow if stakeholders cannot understand how AI models reach decisions. Incorrect recommendations can affect network quality, public safety communication, or cross border coordination. Clear audit trails, transparent governance, and strong validation standards will be important for wider acceptance of AI-based spectrum management.

For instance, in January 2025, while presenting AI RAN at the Future Wireless Summit, Samsung and its partners still framed the work as research and demonstration. This reflects ongoing efforts to validate AI behavior under real spectrum conditions before regulators and operators will rely on it for live network decisions.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

One of the leading players in March 2026, Cisco expanded its AI‑enabled routing and private 5 G portfolio, adding spectrum analytics features that ingest RAN and Wi‑Fi telemetry into a single dashboard. Operators and large enterprises can now visualise band congestion, run what‑if scenarios, and apply automated policies that shift traffic to cleaner channels in near real time.

Top Key Players in the Market

- Ericsson

- Huawei Technologies

- Nokia

- Cisco Systems

- IBM

- Microsoft

- Google (Alphabet Inc.)

- Qualcomm

- Intel Corporation

- Samsung Electronics

- NEC Corporation

- Keysight Technologies

- Viavi Solutions

- Rohde & Schwarz

- Motorola Solutions

- Amdocs

- Red Hat (IBM)

- SAS Institute

- Cognitive Systems Corp.

- Spectrum Effect

- Others

Recent Developments

- In January 2026, Qualcomm broadened its IE‑IoT portfolio with new edge‑AI processors aimed at dense wireless and industrial IoT deployments. By pairing these chips with AI‑driven spectrum sensing and interference mitigation, U.S. and global operators can squeeze more capacity from existing bands and prepare for advanced 5G and pre‑6G services.

- In February 2026, Microsoft deepened its focus on AI‑enabled networks by positioning Azure as a control plane for dynamic spectrum management, building on prior 5G and private‑network initiatives. The company is working with telecom partners to use cloud‑based machine learning for automated frequency planning, congestion prediction, and real‑time interference detection.