When it comes to the elite group of AI stocks known as the Magnificent 7, the winners are pretty established.

Alphabet has established itself as the latest and greatest competitor, and recent stock returns bear that out. There’s also Nvidia, which maintains its position as the king chip maker.

But what happens to the worst performers?

Apple has struggled for some time with the perception that it lags behind when it comes to AI, and is working to become more relevant through partnerships. The meta is under pressure to be the least diverse of the group’s members, and it’s basically AI or perish.

This is surprising for Microsoft, which is probably the biggest laggard at the moment. The company has a well-diversified business and a thriving cloud computing platform. It has its own AI agent in the form of Copilot.

However, check recent performance statistics. Tough to say the least:

- Microsoft stock is on pace to fall 18% in June, making it the worst month since the dot-com heyday of 2000.

- The stock is down 24% so far this year, the worst level on the Richter scale of magnitude 7.

- Approximately $857 billion in market value disappeared during the same period.

- Stocks are currently trading near their lowest since 2023

Now that we have confirmed the company’s position at the bottom of the Mag 7, here are some additional considerations.

Microsoft’s unique double whammy

The company faces a set of circumstances that set it apart from other companies in the Mag7. The company is currently battling both (1) investor backlash against large capital investments in AI and (2) concerns about how AI will disrupt software. After all, despite its new AI ambitions, Microsoft remains the world’s largest software company.

This has created a situation where progress on one front can be reversed by problems on another. When you’re feeling pressured across multiple businesses, diversification suddenly becomes less appealing.

Valuations are at multi-year lows

Just last week, Microsoft’s forward P/E ratio fell to about 21 times, the lowest level in about three years. Traders are wondering whether this is a proper rerating or whether now is the time to buy at depressed valuations. Speaking of which…

Michael Barry buys

The famous “Big Short” investor is among those who like Microsoft’s valuation at current levels. In a post on Substack last Thursday, he wrote that he bought a call option on the stock that would pay off if the stock rises to the low $700s by 2028. Market influencer Burley’s post fueled a 6% rally last Friday.

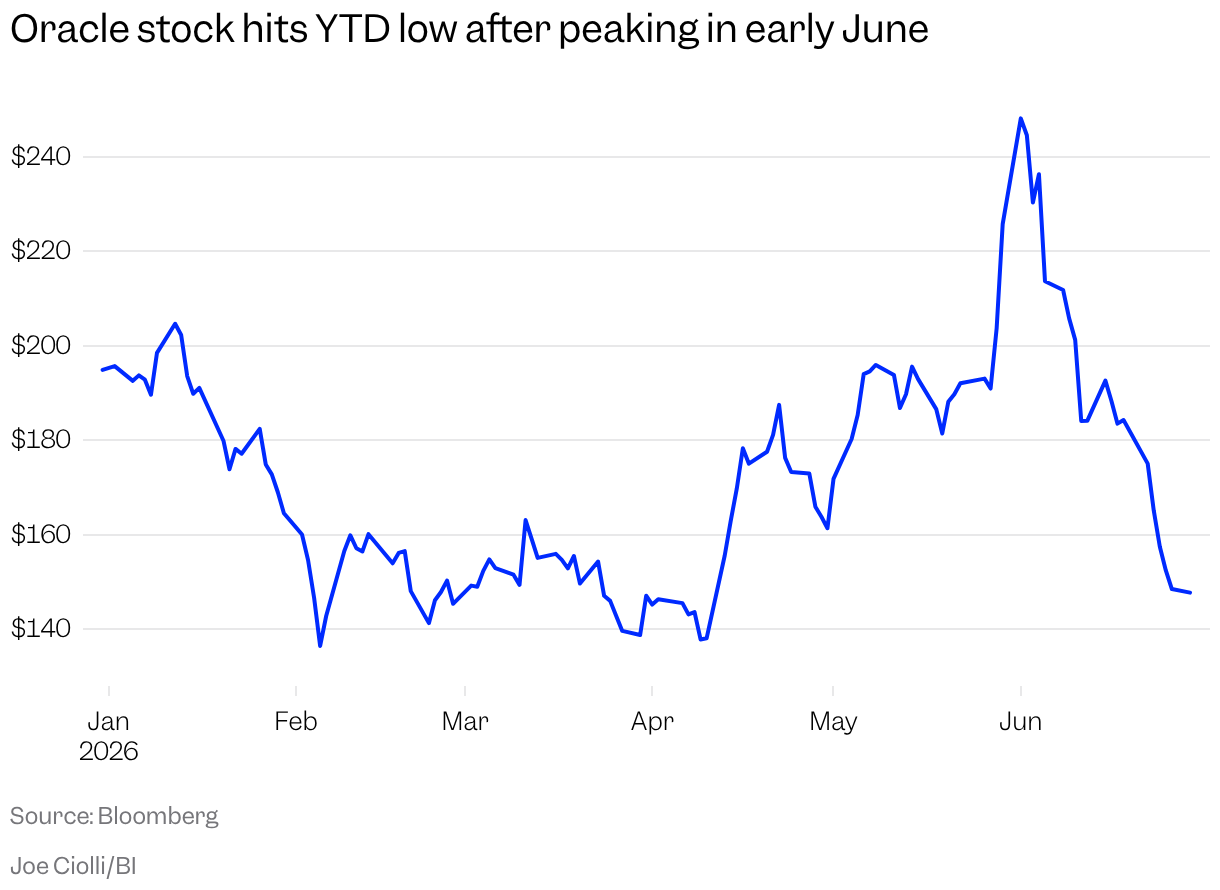

Oracle confirms that Microsoft is not alone

They say that a miserable man loves his fellow man. And in this case, fellow software giant Oracle is feeling the same pain as Microsoft. In fact, the stock chart for 2026 will look somewhat similar.

Oracle, another major hyperscaler, struggles with the same dual problems as Microsoft. Amid concerns about disruption in the software industry, Oracle is also feeling investor resistance to its capital spending.

The key difference is that Oracle is primarily debt-financed, so its corporate bond trading is closely watched. The company’s debt is a bellwether for bond AI trading.

So Oracle will be joining Microsoft in some kind of no man’s land. Both companies are committed to the ultra-expensive endeavor of building AI, but at least for now they are not suspecting investors.