Vitage Sova/iStock via Getty Images

After doing well during the pandemic in sales of washing machines, dishwashers and ovens, major appliance makers are facing a tough 12-month period of sluggish sales.

Analysis of S&P Capital IQ Data shows that sales for the six specialist home appliance manufacturers fell 15% in the fourth quarter of 2022 compared to the same period last year. In the first quarter of 2023, the five companies that have reported so far have revealed further sales declines.

The rapid slowdown in sales appears to have put manufacturers on the back foot. The average inventory-to-sales ratio for the six companies combined was 75% in the fourth quarter of 2022, according to data from S&P Capital IQ.

This was down from the Q1 2022 peak of 104%, but still higher than the Q4 average. Quarters of the last 10 years.

Most companies do not expect a recovery until late 2023. There is no clear evidence yet on whether we will move to an inventory strategy just in case.

Cost reduction

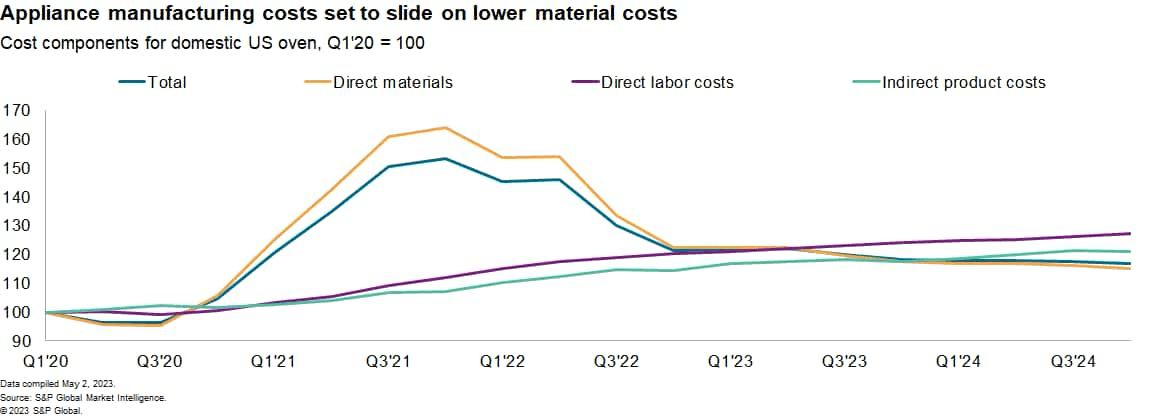

Manufacturers are trying to cut costs by simplifying their products, but they can’t escape a volatile commodity market. Direct materials, including steel, account for about a quarter of the cost of producing a home oven, according to S&P Global Market Intelligence estimates.

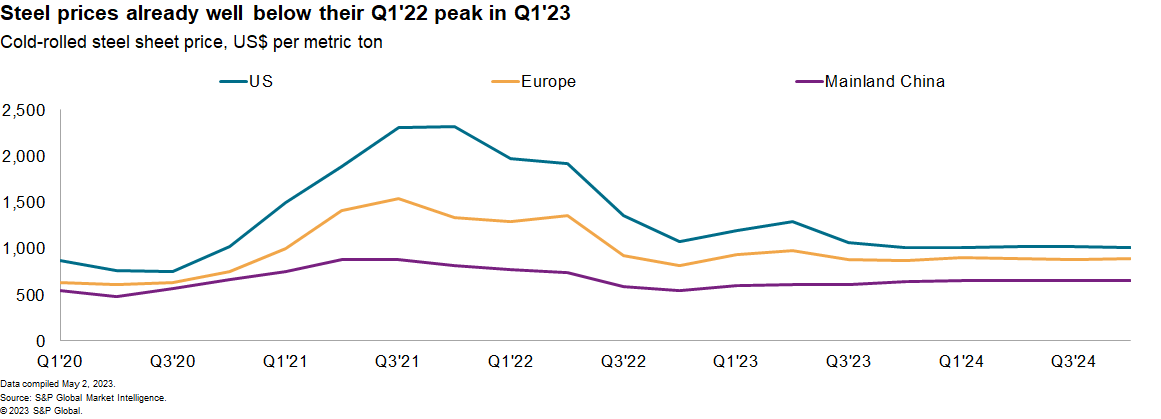

Despite the low cost of many inputs, including electricity, the price of steel in the U.S. continues to remain high relative to markets such as Europe, partly due to tariffs.

The timing of purchases within the supply chain is also important. Falling steel prices have already reduced production costs. For example, according to models from S&P Global Market Intelligence, the cost of manufacturing ovens has already fallen by he 16% in Q1 2023 compared to Q1 2022.

It turns out that non-commodity costs are getting tighter. Labor costs have risen 5% for him over the past year. Total costs in Q4 2024 are expected to be 17% higher than in Q1 2020.

Return to shore or not?

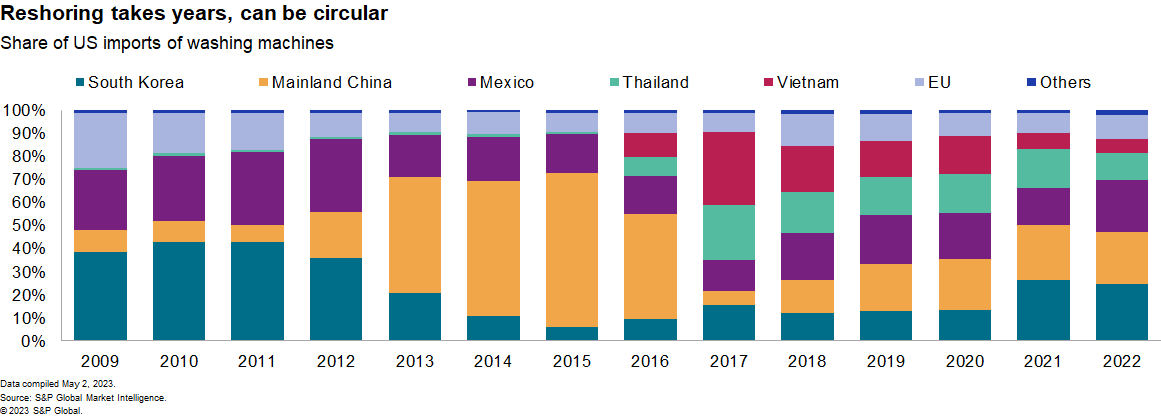

A supply chain cost optimization strategy includes determining the number, size and location of your suppliers. Tariffs will cause U.S. washing machine imports to evolve over a decade, with South Korea, mainland China, and Mexico each accounting for a quarter of imports by 2022.

Changes in US tariffs did not stop exporters from the “new” hub centers. Rather, it has since shifted exports to other target markets, sometimes downsizing its operations.

Decisions about reshoring production require decisions that balance manufacturing costs, logistics costs, and risk considerations. These considerations change over time.

They are seen in the rising risk of labor strikes in Thailand and Vietnam, based on the S&P Global Market Intelligence risk score. Still well below Mexico’s risk score.

Proximity does not reduce cargo risk. Although not directly comparable, Mexico’s surface cargo risk score significantly exceeds that of Thailand and Vietnam at sea.

new challenges

The widespread use of steel in home appliance manufacturing means that supply chains are increasingly exposed to environmental regulations such as the European Union’s Carbon Border Adjustment Mechanism.

The carbon intensity of the eight largest manufacturers differs by more than 20% on either side of the group average. Companies will have to notify their supply chain emissions from October 2023, even if the actual costs will be incurred later. This will give you time to reorient your supply chain if necessary.

This may provide a reason to pursue regionalized supply chains to separate shipments to Asia and shipments to the United States, and to separate shipments to Asia and supplies to the United States.

original post

Editor’s Note: The summary bullet points for this article were chosen by the editors of Seeking Alpha.