Justin Sullivan

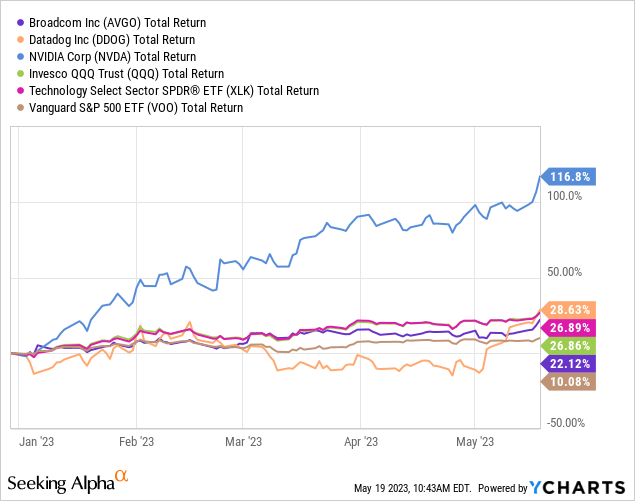

The market certainly seems to have found some of the winners in what I call the “pick and shovel” of AI. These companies provide the essential basic infrastructure to run AI/ML algorithms on Megadata and LLMs (Large Language Models). ).In the old Seeking Alpha In this article, I suggested that DataDog is the winner of the three AI infrastructure (DDOG), NVIDIA (NVDA), Broadcom (NASDAQ: AVGO) (look DataDog and Two Others Are “Definite” Winners in the AI Arms Race). In fact, all three of these stocks have surged year-to-date (Nasdaq 100 Trust (QQQ) and the SPDR Technology Sector ETF (XLK)) And the return of the Vanguard S&P 500 ETF more than doubled (VOO) After the last severe bear market correction, NVIDIA pulled out of the space Year (see figure below). Today I’m going to take a closer look at Broadcom, which has lagged behind the rest of the companies I’ve selected, but should have another strong quarterly report next week. Despite AVGO’s strong fundamentals, high margins, strong free cash flow generation, and annual dividend of $18.40 per share (2.7%), Broadcom still – somewhat puzzlingly – outperformed its peers. is trading at a significant discount (Expected PER = 16.4x).

investment paper

Despite much press coverage, Broadcom has overcome its relationship with Apple (AAPL) (” Broadcom: CEO Shakedown – Hock Tan vs. Tim Cook) and the pending acquisition of VMware (VMW), in my opinion the focus of the company is still on its high-speed networking development platform (both hardware and software) and the products that platform produces, always Broadcom at least a step forward. We are ahead (if not two…) of our competitors.

High-speed networks are essential for moving mega data to and from the cloud to feed data to high-performance computers (“HPC”) such as AI/ML algorithms and large language models (LLMs). Provided by NVIDIA.

LLM refers to AI models that can generate natural language text from large amounts of data. LLMs typically use deep neural networks to “learn” from billions or trillions of words to generate text on any topic. But LLM is just one side of him in the AI/ML revolution that could benefit Broadcom. Subsectors such as IoT, enterprise cloud, data centers, and business optimization (i.e. DataDog) also require fast access to mega data. Therefore, it is clear that there are multiple factors involved in accessing high-bandwidth, low-latency data, and Broadcom has state-of-the-art high-speed networking products to meet that demand.

product

Broadcom has three main switching platforms to benefit from AI: Tomahawk, Trident and Jericho. For example, Broadcom announced the world’s first production 51.2 Tbps (terabits per second) switch in his March. The state-of-the-art Tomahawk 5 family of Ethernet chips is specifically designed to accelerate AI/ML adoption. According to the company, Tomahawk 5’s 51.2 Tbps switching capacity is double his of other switches on the market, resulting in the fastest data transfer between AI/ML endpoints. Tomahawk 5:

… enable single-hop connectivity between 256 high-performance AI/ML accelerators with 200Gbps of network bandwidth each. This results in the fastest completion times for AI training and inference jobs, including today’s increasingly complex and prevalent generative AI models.

During the first quarter conference call in March, Broadcom CEO Hock Tan reported on a companion networking product that fits well with Tomahawk 5 switches.

So this week, we announced the industry’s first integrated silicon photonics networking solution, codenamed Bailey. Integrated active optical interconnect with next-generation Tomahawk 5 switches 51.2 terabits per second. Bailey doubles switching performance, but reduces overall system power.

Tan went on to explain the impact AI is having on hyperscaler customers. Customers have already deployed the company’s Jericho 2 switches in their AI networks. In 2022, he estimated that the company’s Ethernet switch shipments, which he introduced to AI, will exceed $200 million.

We anticipate that this could be significantly exceeded as we anticipate a surge in demand from hyperscale customers. $800 million in 2023. We expect this trend to continue to accelerate, keeping in mind the need for even higher performance networks in the future.

That’s because the company’s switch business is expected to quadruple in a year, so we expect the impact to start showing up on the top and bottom lines in next week’s second-quarter report. In fact, Broadcom’s networking division could easily grow up to 15% this year.

In addition, Broadcom also has a strong custom application-specific integrated circuit (“ASIC”) business (approximately $2 billion in fiscal 2022), which also could grow an estimated 40% this year with strong AI-related tailwinds going forward. There is

Second Quarter Earnings Preview

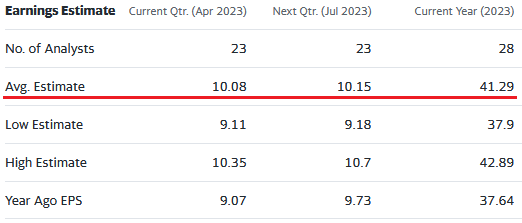

As you can see in the chart below (by Yahoo Finance), Broadcom is widely supported (more than 20 analysts), and the current consensus estimate for the second quarter is EPS of $10.08.

Yahoo Finance

It will be +11.1% compared to the previous year. Second quarter sales are expected to be $8.7 billion, up 7.3% year-over-year.

evaluation

Given the full-year EPS forecast above ($41.29), Broadcom now trades at 16.5 times expected earnings. The graph below compares Broadcom’s current valuation to his two other AIs of my choice, and also adds AMD (AMD).

| TTM PER | Future forecast PER | Division | yield | |

| broadcom | 23 times | 16.5 times | $18.40 | 2.70% |

| Nvidia | 178 times | 69.8 times | $0.16 | 0.06% |

| data dog | N/A | 80.7 times | N/A | N/A |

| AMD | 506x | 37.4 times | N/A | N/A |

The ‘value’ of the four picks is clearly Broadcom, with AMD, Nvidia, and DataDog rising in risk/reward. But don’t let the DataDog fool you. DDOG posted a 32.8% year-over-year revenue increase despite posting a first-quarter GAAP net loss, and during the quarter he generated free cash flow of $116.3 million, raising its forward-looking outlook .

Broadcom is greatly underrated in my book. I say that because of Broadcom’s strong performance during last year’s tech sector bear market. Here’s what Broadcom did for his 2022 fiscal year.

- Revenue increased by 21%.

- Profits increased by 76.9%.

- Dividend increased 12%.

- Generated free cash flow of $16.3 billion (49% of earnings).

Is it just me, or does a company that achieves all of this during a bear market in its own tech sector deserve a future P/E ratio higher than 16.5x?

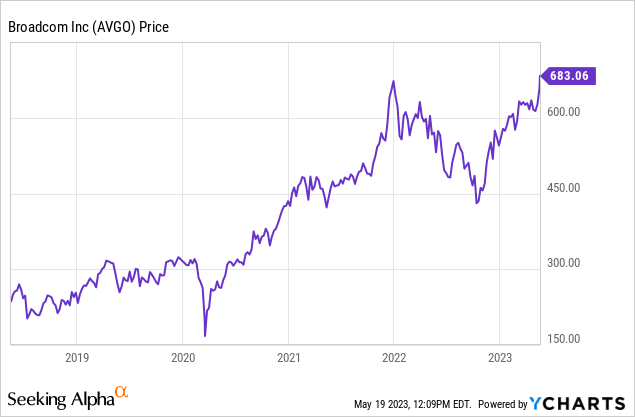

As you can see from the chart above, Broadcom has bounced back sharply from its 2022 bear market lows and is now trading at or near all-time highs, so I’m not the only one who thinks so. is. In fact, the stock has risen more than $50 per share in the last five trading days alone.

risk

I think the chances of getting a deal with VMware are 50/50. As many of you know, the UK recently blocked Microsoft’s (MSFT) bid for Activision Blizzard (ATVI), while the EU and China approved antitrust laws. This may be the flip side of Broadcom’s bid to buy VMware, but CEO Hock Tan recently met with EU regulators and reportedly offered a remedy to move the deal forward. Let’s be honest, your guess is as accurate as mine in terms of the final approval of the transaction by all the necessary global regulators.

Nevertheless, AVGO had $38.2 billion in debt and $12.6 billion in cash at the end of the first quarter, which is arguably a relatively large amount of net debt. Note, however, that in the first quarter Broadcom generated free cash flow of $3.9 billion (+16% year over year). As such, an investor should think of AVGO’s debt in terms of a high-margin business that generates high FCF on a quarterly basis. That said, there could be some short-term downsides in terms of the obvious increase in debt burden if the VMware deal goes through. Remember, the deal was a 50:50 cash-and-stock deal in which Broadcom also assumed about $8 billion of his VMware net debt.

As for second-quarter earnings, the downside risk is that the quarter could soften further, as business with Apple was weaker than expected in an already seasonally weak quarter.

Upside risks include faster-than-expected increases in high-speed network sales and orders.

Summary and conclusion

Broadcom is likely to meet its goal of returning with a strong quarterly report featuring slow but steady revenue growth, strong profit margins and strong free cash flow. Shares surged ahead of Thursday’s earnings report. For current Broadcom holders, I rate this stock as a hold. For those who don’t already own Broadcom and would like to establish a position, buy a small starter position (such as 10% of the final allocation) and add more shares as the price drops due to market volatility. We recommend that you wait until In any case, I’m relatively confident that Broadcom’s stock will be significantly higher a year from now than he is now.

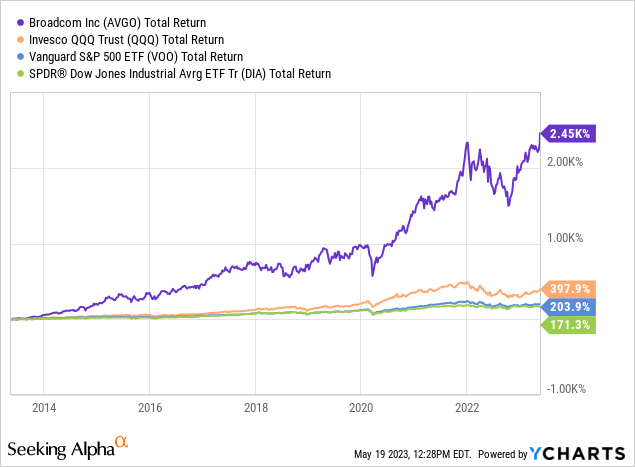

Finally, Broadcom and QQQthe S&P 500 represented by the VOO ETF, and the DJIA represented by the SPDR DJIA ETF (DIA):

As you can see, Broadcom has dominated major broad stock market indices for the past decade. Additionally, Broadcom has made multiple large acquisitions within the time period shown, and that his CEO Hock Tan has acquired those businesses with high profit margins and free his cash his flow. Note also that I proved myself time and time again by creating . There’s no reason to doubt that your contract with VMware (if it does) would be anything different. Or perhaps Broadcom will continue to outperform major market indices over the next decade.