Important points

-

Nvidia’s physical AI revenue grew impressively last quarter.

-

The company has significant growth opportunities in this space, as shipments of physical AI devices are set to increase at an impressive rate over the next decade.

Nvidia(NASDAQ:NVDA) is the biggest beneficiary of massive investments in artificial intelligence (AI) data center infrastructure over the past few years. The company’s chip systems are widely deployed by hyperscalers, governments, and AI companies to support the training and deployment of AI models.

But now, AI is moving from the data center to edge applications such as smartphones, drones, vehicles, robots, industrial automation, and healthcare. Edge AI devices can process AI workloads locally rather than sending them to the cloud, enabling faster real-time decision making. The good news for Nvidia stock investors is that the company is already raising money from growth in edge AI applications.

Will AI create the world’s first millionaire? Our team published a report on one little-known company called an “essential monopoly” that provides critical technology needed by both Nvidia and Intel. Continued “

Image source: Nvidia.

Nvidia’s physical AI business is growing at an impressive pace

Physical AI refers to the integration of AI into edge devices, such as cars and robots, to enable them to make autonomous decisions in real time. Robotaxis, factory robot arms, and humanoid robots are examples of physical AI.

Market research firm Counterpoint Research estimates that shipments of physical AI devices could reach 145 million units between 2025 and 2035. The research firm adds that robots, self-driving cars, and drones will drive the growth of this market. Nvidia has already begun to take advantage of this opportunity.

In its latest earnings report, the company noted that physical AI revenue exceeded $9 billion in the past 12 months. For comparison, Nvidia’s physical AI revenue was $6 billion in fiscal year 2026. That means quarterly revenue run rate for Nvidia’s physical AI business increased by 50%. Importantly, this segment is poised to grow at a stronger pace. That’s because the company has partnered with major physical AI companies. In a recent earnings call, CFO Colette Kress pointed out that:

Our partnership with Uber will enable robotaxis to operate in approximately 30 cities on four continents by 2028. Additionally, in the field of robotics, leading companies across a wide range of industrial, surgical, and humanoid applications are building on Nvidia technology and deploying it at scale.

CEO Jensen Huang also recently said $5 trillion will be spent building factories around the world. Major manufacturers etc. TSMCPegatron, Wistron, Foxconn, and others are already using Nvidia’s platform to build digital twins of their factories before starting actual construction, and importantly, integrating physical AI solutions to boost production.

Nvidia is also collaborating general motors Help automakers build factories equipped with robots. The semiconductor expert also released foundational models and physical AI tools to help developers train robots and self-driving cars.

Grand View Research predicts that the physical AI market could generate $960 billion in annual revenue in 2033, up from just $81 billion last year. Therefore, Nvidia is making the right moves to become a major player in the rapidly growing physical AI market in the long term.

It’s never too late to buy stocks

Nvidia’s focus on expanding its addressable opportunities by entering new markets should help it maintain its impressive growth. Physical AI isn’t the only new area Nvidia is targeting. The decision to sell Vera server central processing units (CPUs) as standalone products will help the company generate an additional $20 billion in revenue this year.

Nvidia has traditionally offered server CPUs as part of rack-scale server solutions that include other chips. But the company can’t ignore the standalone demand for these chips, and management believes the decision to sell Vera CPUs to customers opens up a potentially $200 billion addressable market.

It’s no surprise that analysts have significantly raised their growth forecasts.

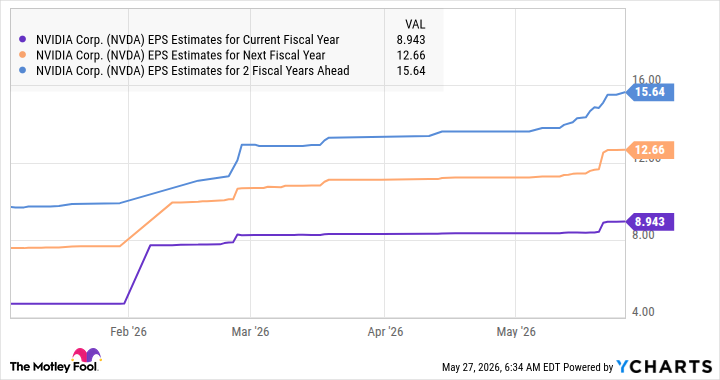

Data by YCharts

Nvidia reported earnings per share of $4.77 for fiscal 2026 (ending in January of this year). The consensus estimate for fiscal 2029 earnings per share of $15.64 suggests that NVIDIA’s revenue will grow at a compound annual growth rate (CAGR) of 48%. At a price-to-earnings ratio of 33 times, it discounts the 35.6 times earnings multiple of the tech-heavy Nasdaq 100 index, making this AI stock a good buy now.

The company expects AI infrastructure investments to reach an annual run rate of $3 trillion to $4 trillion by the end of the decade. This means the company’s core data center business is poised to continue to grow steadily. Throw in additional catalysts like physical AI, and it’s easy to see why it makes sense to buy and hold Nvidia over the long term.

Should you buy Nvidia stock now?

Before buying Nvidia stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors can buy right now…and Nvidia wasn’t among them. These 10 stocks have the potential to generate impressive returns over the next few years.

when to think about it Netflix This list was created on December 17, 2004…if you invested $1,000 at the time of recommendation. you have $465,733!* or when Nvidia This list was created on April 15, 2005…if you invested $1,000 at the time of recommendation. you have $1,313,467!*

Now, the important thing to note is that stock advisor Total average return is 985% — compared to the S&P 500’s 211%, an overwhelming market outperformance. Don’t miss our latest Top 10 list. stock advisorjoin an investing community built by retail investors, for retail investors.

See 10 stocks »

*Stock Advisor will return on May 29, 2026.

Harsh Chauhan has no position in any stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool recommends General Motors. The Motley Fool has a disclosure policy.