- If you’re wondering whether Oracle’s current stock price reflects its true value, you’re in the right place to unpack what the market might be telling you about value.

- Oracle’s closing price was $149.68, down 3.5% over the past 7 days, down 4.2% over the past 30 days, down 23.5% year-to-date, but up 76.3% over three years and 128.2% over five years. Taken together, these provide a comprehensive picture of recent and long-term performance.

- Recent headlines about Oracle have focused on its position in large-scale software and cloud infrastructure, as well as continued interest in how Oracle fits into broader AI and data management themes. At the same time, investors are reacting to overall sector sentiment, regulatory discussions, competitive announcements, etc., which may influence how much risk or opportunity the market prices in for Oracle.

- Oracle currently has a Valuation Check score of 5 out of 6, suggesting that many of our tests consider the stock to be undervalued. In the next section, we compare different valuation methods and finally explain how to put these numbers into a broader context.

Oracle’s return last year was -0.7%. See how this compares to other software industries.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

Discounted cash flow (DCF) models aim to estimate a business’s value at present value by forecasting a company’s future cash flows and discounting them to the present.

In the case of Oracle, the model used is a two-step free cash flow-to-equity approach that works on a dollar-by-dollar basis. Free cash flow for the most recent 12 months is a loss of around $2.2 billion, so the starting point is negative. Estimates with analyst input and estimates project free cash flow for the next 10 years. The model includes projections such as free cash flow of $28.5 billion by 2030, with the interim year moving from a loss in the first half of the period to a positive level in the second half.

Combining all of these projected cash flows and discounting them to the present yields an estimated intrinsic value of approximately $259.82 per share. Compared to the recent stock price of approximately $149.68, this model implies that Oracle is trading at a 42.4% discount to this DCF estimate. This method makes the stock appear undervalued.

Result: underestimation

Our discounted cash flow (DCF) analysis suggests that Oracle is undervalued by 42.4%. Track this with your watchlist or portfolio, or discover 52 more high-quality undervalued stocks.

For more information on how we calculated this fair value for Oracle, please see the Valuation section of our company report.

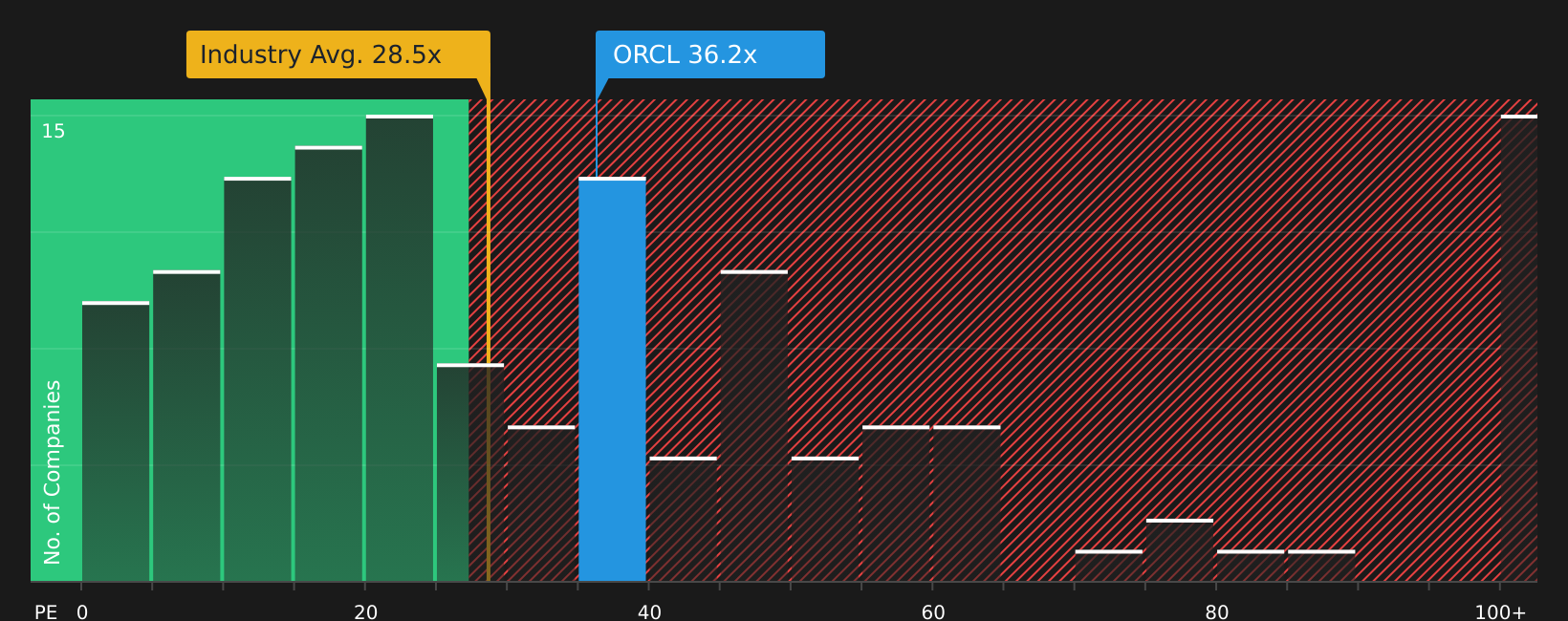

Approach 2: Oracle price and revenue

For profitable companies, the P/E ratio can help you figure out how much the company is paying for each dollar of its current earnings. This summarizes the market’s view of growth potential and risk into one number, making it easier to compare across similar businesses.

Higher expected growth or lower perceived risk usually supports a higher or “richer” P/E, while slower growth or higher risk usually indicates a lower or “cheaper” P/E. Oracle’s P/E ratio is currently 26.59. This is lower than the software industry average of 29.37x and significantly lower than the peer average of 56.35x. This suggests that the market is pricing Oracle differently than many of its peers in the space.

Simply Wall St’s Fair Ratio is a proprietary estimate of what a company’s P/E ratio “should” be, taking into account its earnings growth, industry, profit margin, market capitalization, and risk profile. This customized view is more informative than a simple comparison to industry or peer averages because it is tailored to Oracle’s unique characteristics, rather than treating all software companies as the same. In Oracle’s case, the fair ratio is 56.54x, which is higher than its current P/E ratio of 26.59x, indicating that the stock may be undervalued by this metric.

Result: underestimation

P/E tells one story, but what if the real opportunity lies elsewhere? Start investing in legacy, not management. Check out the 20 top founder-led companies.

Upgrade your decision making: Choose your oracle narrative

I mentioned earlier that there is a better way to understand valuation. This is where the narrative comes into play. This provides an easy way to connect your view of Oracle’s story to a set of numbers, such as fair value, future earnings, earnings, and margin, to see how it compares to the current stock price.

In Simply Wall St, the narrative is a plain language version of the oracle’s story behind the prediction. For example, an investor might describe Oracle as a high-performance cloud infrastructure provider coupled with AI data centers that has a fair value per share of approximately $119.97. It also focuses on long-term AI infrastructure needs, potentially pushing the fair value closer to US$400 per share.

Each narrative on the community page links its story to a financial model and fair value estimate, and by comparing it to the latest market price, you can quickly see whether your view of Oracle suggests opportunity or risk. The platform updates the narrative as new information, such as news or earnings, is added, keeping your decision-making framework up-to-date without having to rebuild everything from scratch.

However, for Oracle, there are two major Oracle Narrative previews that make it very easy to navigate:

🐂 oracle bull case

Fair value in this story: USD 389.81 per share

This implied discount to fair value: approximately 62% compared to the recent stock price of $149.68.

Revenue growth assumption used: 28%

- This narrative focuses on Oracle as an AI infrastructure partner, focusing on large-scale superclusters, relationships with OpenAI, and very large data center projects tied to high computing demands.

- This is highly dependent on the extremely rapid growth of multi-cloud database activity and AI-related workloads, as well as remaining performance obligation numbers reaching hundreds of billions of USD.

- Key risks flagged include carrying out large-scale capacity increases, securing energy and hardware supplies, and managing volatility if market skepticism and AI project failure rates impact sentiment.

🐻Oracle Bear Case

Fair value in this story: USD 119.97 per share

This implied premium to fair value: approximately 25% compared to the recent stock price of $149.68.

Revenue growth assumption used: 15,057.17%

- This narrative sees Oracle as a strong but mature enterprise software and cloud business, and while the AI story makes sense, it doesn’t necessarily justify paying much more than its revenue-based fair value range.

- This article highlights Oracle’s large installed database base, profitability, and AI-focused cloud infrastructure, which are configured to support steady growth rather than incremental change.

- Risks center around intense competition from major cloud providers, the capital intensity of data center expansion, and the potential for market expectations to grow beyond what current business can support.

If you want to go beyond these two previews and see all the community’s thoughts on Oracle, including different growth, margin, and valuation assumptions, you can check out our broader set of narratives to decide which one best aligns with your expectations for the stock.

Think there’s more to Oracle’s story? Visit our community to see what others are saying.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: AI stock screener and alerts

Our new AI Stock Screener scans the market for opportunities every day.

• Dividend powerhouse (yield 3% or more)

• Small-cap stocks that are undervalued due to insider purchases.

• High-growth technology and AI companies

Or build your own metrics from over 50 metrics.

Explore for free now

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.