Crow by Jennifer Jarzak and Karen McDaniel

As sponsors and CROs increasingly integrate AI into clinical trials, data management, and analytics, finance leaders at both organizations are facing the pressing challenge of how to account for AI-related costs under evolving U.S. Generally Accepted Accounting Principles (GAAP).

The life sciences ecosystem is focused not only on effectively deploying AI, but also on mitigating risks and exposures, including identifying hallucinations and validating the reliability of AI data, outputs, and processes. The types of AI technologies used vary by department and at different stages of the contract lifecycle. Sponsors and CROs using AI should be aware of some of the common use cases for AI that are emerging today, understand how financial reporting may be treated differently depending on the complexity of accounting rules and associated impacts, and clarify what financial professionals should consider when embarking on an AI initiative.

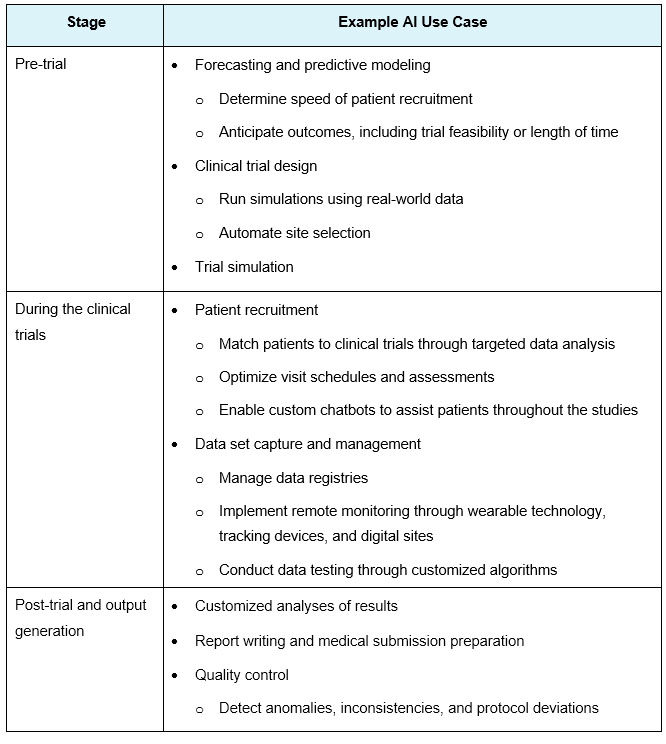

AI use cases

Life sciences organizations have ample opportunity to use AI throughout the clinical trial lifecycle. Some possible use cases are listed in the following table.

Financial reporting considerations

The uses of AI throughout the clinical trial lifecycle vary, and the costs incurred to develop or implement such technology may be capitalized as an asset or immediately expensed based on several factors.

One important consideration regarding software is its intended use: will it be sold as a product or service, or will it be used internally to provide a service? When software is sold, leased, or sold commercially, accounting follows Accounting Standards Statutory Code (ASC) 985. This requires that the software be technically feasible before the associated costs can be capitalized as an asset. If the software is for internal use or service delivery, certain AI-related costs, such as coding and direct implementation costs, can be capitalized during the application development phase and continue until the software is ready for use for that purpose.

Additionally, tools that begin as applications for internal use may later be delivered externally once measurable business value is achieved. This evolution creates additional accounting complexity, particularly with respect to reclassification and capitalization when transitioning between ASC 350-40 and ASC 985-20. Such outcomes are common in AI development, where projects often proceed in evolving environments without a clearly defined end state.

AI assets also differ from traditional software in that factors such as model drift, outdated training data, and evolving regulatory requirements can cause them to degrade more quickly, increasing the risk of impairment. Additionally, AI tools often require continuous evaluation, guardrails, and monitoring for issues such as hallucinations, all of which require additional development time and resources. As a result, the distinction between development and maintenance activities can become blurred, making appropriate accounting more complex.

Careful judgment is also required when determining whether the costs incurred are related to software, another type of intangible (such as a process or database), or something else entirely. Depending on the nature of the activity, costs may qualify as research and development expenses and are generally expensed as incurred under ASC 730. Similarly, most costs incurred for internally developed intangible assets are expensed as incurred unless specific rules governing capitalization apply (such as for software or assets acquired in a business combination).

Impact of changes in accounting standards

Accounting Standards Update (ASU) 2025-06, issued in September 2025, updates guidance for internal use software. It will be effective from fiscal years ending on or after December 15, 2027, with early adoption permitted. The types of expenses that can be capitalized remain largely unchanged. However, this update removes the project stage capitalization framework and replaces it with two criteria: 1) management approval to complete the project, and 2) the likelihood that the software will be completed and used as intended. The level of cost capitalization achieved under the revised guidance may vary significantly depending on the level of development uncertainty associated with the project. Furthermore, traditional software capitalization timelines do not necessarily map cleanly to AI, and it is unclear how to account for work that is continuously in progress under the “completion and likelihood of use” standard.

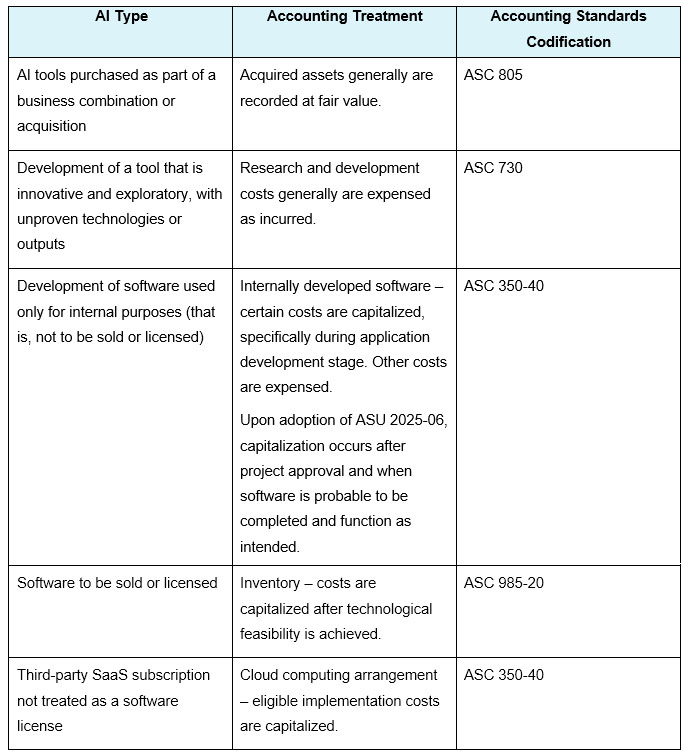

The following table shows the potential accounting implications for different types of AI tools.

Impact on financial statements

Proper cost treatment directly determines how a company’s financial condition and performance are reported based on GAAP and non-GAAP measures. Determining whether to expense or capitalize costs may require judgment consistent with applicable accounting standards. This is not an accounting policy choice or preference.

Expenses are immediately recorded as operating expenses, increasing current period expenses and decreasing net income and operating income. Capitalizing costs records the costs as an asset and prevents them from having an immediate impact on revenue. Instead, the expense is recognized gradually through depreciation or amortization, which increases net income more than if the expense were expensed immediately.

This difference also affects earnings before interest, taxes, depreciation, and amortization (EBITDA). To the extent that an item is capitalized as an intangible asset, it will flow through EBITDA as an amortization charge when its cost is expensed through earnings. Therefore, capitalizing AI-related costs typically has virtually no impact on EBITDA. In contrast, expending costs immediately reduces EBITDA in the year in which they are incurred. As a result, a firm may appear to have better current operating performance under the capitalist model, even if its cash outflows remain unchanged.

Cost classification also affects compliance with debt contracts, especially if the contracts are tied to operating income or EBITDA. Operating expenses reduce revenue and EBITDA in the year in which they occur, potentially creating a risk of covenant default, whereas total capital is neutral to EBITDA and therefore has a positive impact on the covenant ratio.

In summary, the judgment applied in determining asset and use types can impact the ability to capitalize or expense AI and other related costs, impacting financial performance metrics, investor perception, and code compliance, highlighting the importance of accurate and compliant cost classification.

Financial reporting for AI

To ensure AI accounting accuracy, finance leaders need to understand AI’s place within their organization, including the technology’s purpose, use, and associated costs. After defining an AI project, leaders must take the following steps:

- Understand which accounting model applies and whether expenditures are treated as assets or expenses.

- For internal use software under ASC 350-40, determine when to apply the guidance in ASU 2025-06. Will this guidance be adopted early or will we wait until it is necessary (for fiscal years beginning after December 15, 2027)?

- If ASU 2025-06 is adopted early, it will determine when the new capitalization criteria (management approval plus completion and availability) are met. Judgment may be required to assess whether “material development uncertainties” exist.

- Maintain simultaneous documents.

Store key project records such as feasibility assessments, design approvals, meeting notes, and milestone review sign-offs to support capitalization decisions.

- Accurately track internal and third-party costs.

Accurate cost recording and allocation is essential to determining which expenses are eligible for capitalization.

- Implement a time tracking system to allocate effort by project. Develop internal cost allocation policies for AI projects, including guidance on sharing full-time equivalents and mixing project work.

- Use cost codes to differentiate between capitalizable and non-capitalizable tasks.

- Require vendors to specify the nature, scope, and schedule of deliverables in the statement of work.

- Support your useful life and amortization estimates with evidence.

Document the basis for the useful life estimate, including considerations such as technology obsolescence, model performance degradation, and expected service life. Significant judgment may be required.

- Monitor impairment indicators.

Establish procedures to assess whether capitalized AI assets are still in use, continue to produce the intended economic benefit, or have become obsolete due to regulatory, technological, or operational changes.

- Stay current with evolving accounting guidance.

Rapid advances in AI technology continue to evolve the interpretation of existing standards. It is essential to monitor developments in U.S. GAAP, International Financial Reporting Standards, and related industry guidance that may impact the accounting for AI software and infrastructure costs. Consider the need to seek assistance from a technical accounting advisor.

About the author:

Jennifer Dzierzak, CPA, is a partner in Crowe’s Audit and Assurance Group. She provides deep expertise in financial statement and compliance auditing, as well as acquisition and consolidation accounting for commercial organizations, with a particular focus on the life sciences sector. Jennifer has over 20 years of experience serving both public and private companies, is well versed in complex accounting and reporting matters, and has extensive knowledge of International Financial Reporting Standards and U.S. GAAP requirements.

Jennifer Dzierzak, CPA, is a partner in Crowe’s Audit and Assurance Group. She provides deep expertise in financial statement and compliance auditing, as well as acquisition and consolidation accounting for commercial organizations, with a particular focus on the life sciences sector. Jennifer has over 20 years of experience serving both public and private companies, is well versed in complex accounting and reporting matters, and has extensive knowledge of International Financial Reporting Standards and U.S. GAAP requirements.

Karen McDaniel, CPA, is a partner in Crowe’s Audit and Assurance Group and has extensive experience serving life sciences and manufacturing companies across all stages of the business life cycle. She advises clients with a focus on accounting for complex transactions and financial reporting matters, from the early stages of development to IPO preparation, SEC reporting, and ongoing public company compliance. She has deep expertise in SOX 404 compliance, internal control design and improvement, and technical accounting under U.S. GAAP. Karen brings a disciplined, risk-focused approach to help high-growth organizations meet regulatory and reporting requirements efficiently and effectively.

Karen McDaniel, CPA, is a partner in Crowe’s Audit and Assurance Group and has extensive experience serving life sciences and manufacturing companies across all stages of the business life cycle. She advises clients with a focus on accounting for complex transactions and financial reporting matters, from the early stages of development to IPO preparation, SEC reporting, and ongoing public company compliance. She has deep expertise in SOX 404 compliance, internal control design and improvement, and technical accounting under U.S. GAAP. Karen brings a disciplined, risk-focused approach to help high-growth organizations meet regulatory and reporting requirements efficiently and effectively.