Shatifong Chandaeng

investment paper

Soundhound AI Inc. (NASDAQ: SOUN) is a voice AI technology company. Its platform allows users to be more productive by operating the product via voice commands.

The main problem I have as an investor is We believe that voice AI has the potential to become absolutely massive in the near future as it simplifies tasks for users.

Rather, my issue is that by investing in SoundHound, investors are purely speculating. And the chances of an investor making a profitable investment here are rather low.

Why Choose SoundHound AIWhy Now?

SoundHound is a voice AI platform. This voice-enabled AI company has the right story at the moment, and that’s why investors are interested in it.

The idea here is that conversational AI users can provide better results.

SOUN Investor Presentation

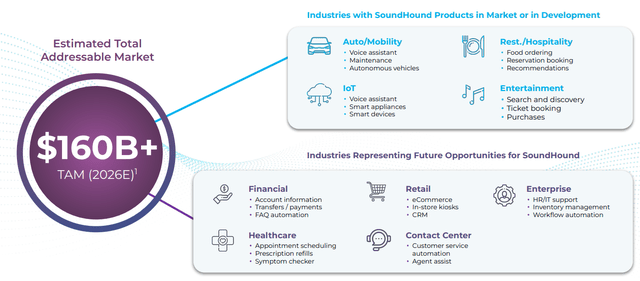

SoundHound estimates that sum is addressable The market could reach $160 billion in the next three years. For a company with a market capitalization below his $1 billion, this clearly shows the extent of potential.

Additionally, an important use case for SoundHound is appealing to car manufacturers for electric vehicles. In response to this, SoundHound said at its earnings call:

We are able to extend our existing customers and are constantly adding new ones. For example, in the automotive field, sales volume more than doubled in the first quarter, and unit prices increased.

As a potential investor, I’d rather see a rapid adoption of a platform that grows with a significant increase in customers than a price hike. At least in the growth stage of the business.

And ultimately, it’s important that compelling stories lead to rapid revenue and booking growth, which we’ll cover next.

Earnings growth continues to be strong

Early clouds

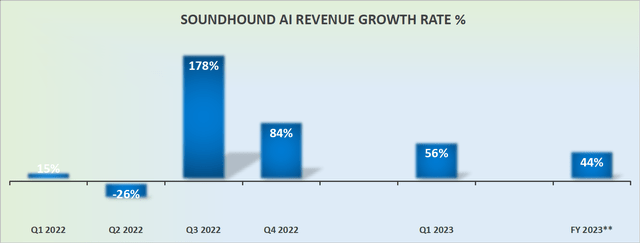

SoundHound’s bullish case is that its growth rate is very high. A good example of this is the expected growth rate of about 44% year-on-year in 2023.

That being said, check if there are any patterns in your booking profile.

- Q1 2022: +134% YoY

- Q4 2022: 59% YoY

- Q1 2023: 46% YoY

Bookings are a leading indicator of revenue growth. In an ideal situation, you want your booking to be stable. Alternatively, if your company is growing rapidly, you may want more bookings.

But as we saw above, neither side is happening here.

Some might argue that SoundHound is still in its early stages. And I would argue that investing in high-growth companies is always difficult.

Especially when investor expectations are already very high. Because when investor expectations are so high, companies need to actively surprise investors on a continual basis. And not here.

In fact, as you may recall from last week’s Q1 2023 results, SoundHound actually underperformed consensus earnings expectations.

Problematic profitability profile

Let me focus on why I’m not bullish on SoundHound.

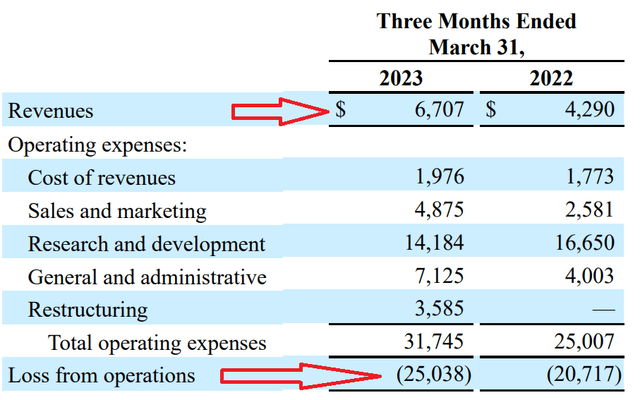

SOUN Q1 2023

Above we can see that despite SoundHound’s increasing revenue, this is achieved by increasing losses. Even if we consider the restructuring charges as temporary non-recurring items, in reality we have not seen any significant progress in improving the company’s healthy profitability.

Second, note that SoundHound ended Q4 2022 with 157 million shares outstanding.

Then, in the next quarter, Q1 2023, total shares outstanding increased by 31%. This consideration alone, perhaps more than any other aspect, should make investors very cautious about putting their hard-earned money into this business.

Soundhound AI Inc. increasing equity capital to pay off debt. This makes no sense economically. And if the underlying business was more stable, the company wouldn’t have embraced this kind of financial engineering.

Conclusion

Just to be clear, I believe voice AI will change our habits a lot. Voice AI improves our productivity every day and continues to deliver unimaginable benefits for both consumers and businesses.

My only argument is that investing in SoundHound AI, Inc. is not the right way to profit from this long-term growth opportunity.