courtneyk

Snowflake (New York Stock Exchange: Snow) built a cloud-based warehouse on AWS in 2014 and then began building platforms and applications to run workloads beyond data warehousing. Over the past few years, Snowflake has seen tremendous growth, with sales up from his $100 million. It is expected to exceed $2 billion in FY2019 and over $2 billion in FY23. They are taking market share from traditional incumbents like his Teradata (TDC), Oracle (ORCL), IBM (IBM), EMC.

I believe Snowflake combines database management, data analytics, machine learning, cyber security, and data sharing to break down siled and structured data. Additionally, the Snowflake Marketplace allows enterprise customers to combine internal data with external third-party his data products for better data analysis and decision making. From my perspective, Snowflake will be the most relevant cloud platform for machine learning and data analytics.

How big is the market?

According to the Gartner database, Administrative spending will outpace the broader software market, growing from 13% of software spending in 2021 to 17% in 2026. One obvious reason for this growth is the migration of workloads to the cloud. As workloads migrate, the cloud’s share of the database market is growing and is expected to reach 71% by 2025.

Data infrastructure and data cloud are two key factors. Enterprises need a cloud data infrastructure to store and aggregate data from various sources such as CRM, cybersecurity, HRM, and more. Businesses need to share data, perform data analytics, and leverage machine learning for AI capabilities with structured and unstructured data. The ideal approach is to run all these workloads in the data cloud.

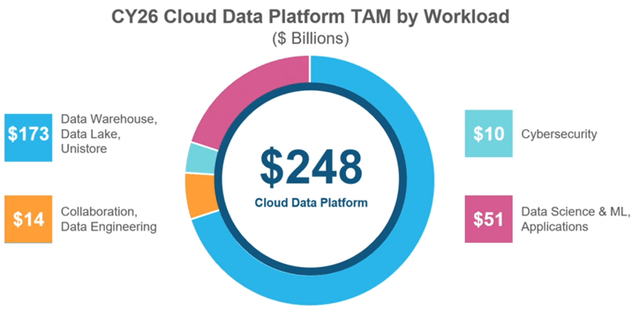

The data cloud includes all workload execution, data sharing, and data marketplaces. According to Snowflake, the market addressable across cloud data platforms is estimated to be $248 billion in 2026. This is definitely a huge market for Snowflake.

Snowflake Investor Day 2022

How much growth can Snowflake capture?

Data analytics and machine learning are still in the early stages of adoption: We believe that data analytics and machine learning are perpetual trends regardless of the macro environment and that industry adoption is still in its early stages. Deploying machine learning and data analytics requires moving all data to the cloud, designing workloads and applications for the cloud, and running these applications on the data cloud.

I think Oracle and Teradata are losing the game. why? Oracle and Teradata provide data warehouses, but the data sets are siled and structured. In some cases, customers use spreadsheets to download and share data across platforms/departments. In other words, data clouds and workloads are not fully integrated and data is siled. Instead, Snowflake’s platform empowers data, breaks down siled data, whether structured or unstructured, and supports all these workloads in the data cloud. These features are important for data analytics and machine learning.

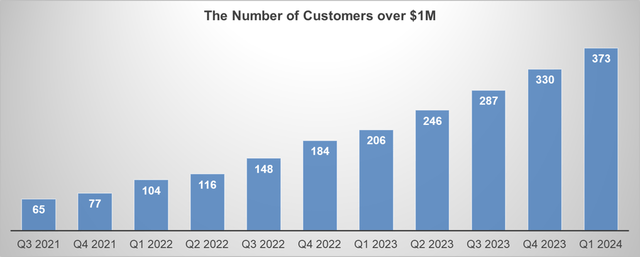

Great customer growth potential: Snowflake focuses on customers who have the potential to generate more than $1 million in sales over the next 12 months. It’s important to note that Snowflake follows a consumption-driven model, not his SaaS pricing model. Their earnings depend on the amount of consumption that occurs over a period of time. Of the current million dollar customers, only 45% are Global 2000 customers, 55% are corporate accounts, and 1% are corporate accounts. In other words, Snowflake has great growth potential within these large accounts. The chart below shows the growth in the number of customers with sales over $1 million.

Snowflake Quarterly Results, Author’s Calculations

Increased net earnings retention rate: In its first quarter 2023 earnings call, Snowflake indicated that it expects net earnings retention to be well above 130% over the long term. Snowflake operates on a consumption-driven revenue model, so customers can grow their usage over time as data cloud workloads, data sharing, and analytics continue to deliver value. In my opinion, achieving a net revenue retention rate of over 130% is exceptional among software companies.

Why is Snowflake disrupting the data cloud industry?

I am using Teradata as a comparison. The two main differences between Snowflake and Teradata are architecture and flexibility.

Teradata warehouses use hardware and software components that must be installed on-premises for optimal operation. They offer cloud services, but they are not as popular as using their own software and hardware. Teradata uses a shared-nothing architecture, where each node operates independently at optimal speed using on-premises software and hardware.

For capacity and flexibility, Teradata relies on fixed capacities specified in hardware and software. When data exceeds this capacity, customers must purchase more hardware and software to scale. In other words, data warehouses are inflexible to meet the demands of growing datasets.

In contrast, Snowflake utilizes a combination of shared-nothing and traditional shared-disk architecture. This new architecture enables Snowflake to provide database storage, query processing layers, and cloud services. As a result, Snowflake operates as a cloud solution, with all components residing on the cloud. No software or hardware installation required, no capacity limits. All queries using SQL leverage cloud infrastructure providers such as AWS, Azure, and GCP.

From the customer’s perspective, there is no upfront investment associated with data storage or data analysis. This means that customers do not need to purchase any hardware or software upfront. Instead, move your workloads to the cloud, use Snowflake as your data cloud, and pay for the service on a pay-as-you-go model. As more and more workloads move to the cloud, Snowflake promises to transform the data management industry.

Outlook and key risks

Data cloud weakness consumption: As mentioned earlier, Snowflake’s business model is primarily consumption-based. This means customers have the flexibility to reduce their spending on Snowflake, even during difficult macroeconomic conditions. During the Q1 2024 earnings call, there were questions about the macro environment and corporate data consumption. Snowflake’s management acknowledged that the consumption-based model makes short-term growth difficult to predict, as customers may change their consumption patterns. Additionally, companies may postpone cloud migration projects to cut costs. This could lead to short-term disruptions to workload migrations and adversely affect Snowflake’s revenue.

Conflicts with hyperscalers: Snowflake has partnered with all major hyperscalers, including AWS, Azure, and GCP, and offers massive usage on these platforms. About 80% of Snowflake’s sales come from his AWS platform. At the same time, Amazon offers services such as Amazon RedShift, Athena, and Amazon EMR that focus on workload analytics. However, Snowflake provides a comprehensive platform that covers the entire spectrum of data warehouses, data lakes, data science, data analytics, and data application development. On the other hand, Amazon only designs some data analysis capabilities for simple applications, and they are more suitable for small businesses.

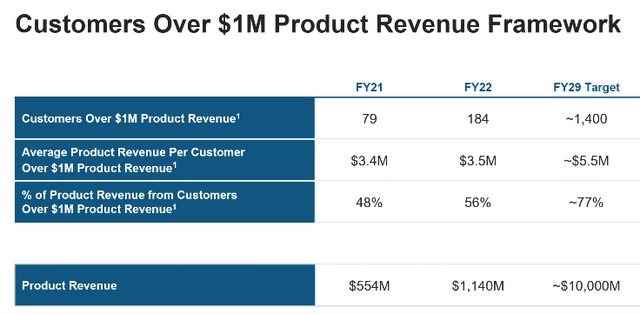

But despite this uncertainty, I remain optimistic about Snowflake’s long-term growth. The company’s platform plays a mission-critical role for its customers, and many of them continue to adopt data analytics and machine learning. Snowflake maintains his FY29 growth goal, aiming to reach $10 billion in revenue. This translates to a compound annual growth rate of 36% over the next seven years.

Snowflake Investor Day 2022

Snowflake provided guidance of a 34% increase in product sales in fiscal year 2024. We expect product gross margins to be approximately 76% and an adjusted free cash flow margin of 26%. In addition, Snowflake is adjusting its hiring plans for the current fiscal year and expects to add 1,000 employees in fiscal year 24, including potential mergers and acquisitions.

evaluation

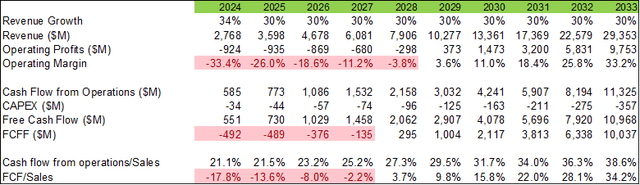

We use a two-stage DCF model to estimate the fair value of Snowflake. The model assumes a normalized sales growth rate of 30%, which is consistent with our long-term guidance of $10 billion in FY29 sales.

We expect to be profitable in FY2017, and expand the operating margin to 33.2% in FY2033. I think it’s pretty normal for a software company to have an operating margin of 30-40%.

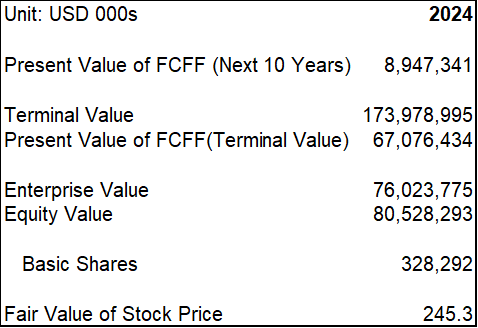

DCF Model – Author’s Calculations

In this model, the free cash flow conversion is estimated to reach 34% in FY33. Again, this is very normal for software companies. In addition, 10% of WACC is used for the model.

The present value of the company’s free cash flow over the next 10 years is estimated at $8.9 billion, giving a terminal present value of $67 billion. The total enterprise value is therefore estimated at $76 billion. My estimate is that the fair value of the stock is $245 after adjusting for total debt and cash balance.

DCF Model – Author’s Calculations

In addition to the DCF model, we compare growth software companies such as ServiceNow, Adobe, and Microsoft using the ratio of current market capitalization to projected five-year sales. As the table below shows, Snowflake’s sales multiple is not significantly different from its competitors. However, it is important to note that Snowflake is targeting a 36% compound annual growth rate over the next few years, which is the highest growth rate among these peers.

Author’s calculation

Conclusion

Throughout my 15-year investment career, I have always sought out technology disruptors before they were widely recognized by the market. I always ask myself some important questions.

- What is the potential market size that the new technology could create or replace within the next decade? How steep is the adoption curve?

- How much growth can your company achieve, and does it have the resources and strong leadership needed to deliver that growth?

- What competitive advantage or “moat” does the company establish to prevent other companies from entering the same space?

Analyzing Snowflake, it meets all the criteria I have for a future unstoppable disruptor. The company has demonstrated significant growth potential, has the technology and effective leadership to realize that potential, and has the ability to create and sustain a competitive advantage in the market.

Based on my assessment, I would strongly advise long-term investors to consider owning this remarkable company at its current price.