The increased interest in Shopify (NasdaqGS:SHOP) stock is driven by the company’s upcoming mid-February earnings release, as well as increased focus on the company’s leadership approach, AI-related policy changes, and updates to its partner program.

Check out our latest analysis for Shopify.

Recent news about the use of AI data, founder-friendly leadership, and changes to the partner program have bucked short-term weakness, with one-month stock returns down 16.52% and 90-day stock returns down 24.12%. At the same time, the 1-year total shareholder return of 12.35% and the 3-year total shareholder return of approximately 1.5x suggest that long-term holders are still reaping the benefits.

If Shopify’s recent volatility has caused you to reevaluate the space, this could be a useful time to see which platforms are being eyed as potential e-commerce and software competitors among high-growth technology and AI stocks.

While Shopify’s stock price has fallen in recent months and months, it remains positive on its 1 and 3-year periods, and the key question is simple. The question is: Does the current price ignore the company’s growth potential, or does it already reflect it?

Most popular story: 29.7% are underrated

The last closing price was $131.23, which is a fair value of $186.64, and the current market price is well below the valuation implied by Shopify’s most followed article.

Five-year revenue (2030): $20-22 billion

why?

Current revenue trajectory indicates 26-29% growth (2024: $8.88 billion, 2025 Q2 TTM: $10.01 billion): https://www.macrotrends.net/stocks/charts/SHOP/shopify/revenue

Social commerce tailwinds at 30.71% CAGR with $6.23 trillion market opportunity

AI tools reduce onboarding friction and increase merchant adoption

Lower barriers to entry through strategic partnerships (DHL, Amazon fulfillment)

US e-commerce market share is over 12% with room to grow: https://www.stocktitan.net/news/SHOP/shopify-merchant-success-powers-q4-outperformance-across-both-top-zcq4nr2tqhzj.html

Assuming growth moderates from the current 25-30% range to 15-20% per year as the company matures, it is expected to be around $20-22 billion by 2030.

Read the whole story.

Interested in supporting a fair value well above today’s price? This story is based on specific earnings trends, margin profiles, and future earnings multiples. Want to know exactly how these moving parts make up that $186.64 number?

Result: Fair value $186.64 (undervalued)

Read the full explanation to understand what’s behind the predictions.

However, this story could change significantly if declining consumer confidence depresses merchant sales or if larger competitors reduce Shopify’s share of e-commerce spending.

Learn about the key risks in this Shopify story.

Another way of looking at it: the income of the rich.

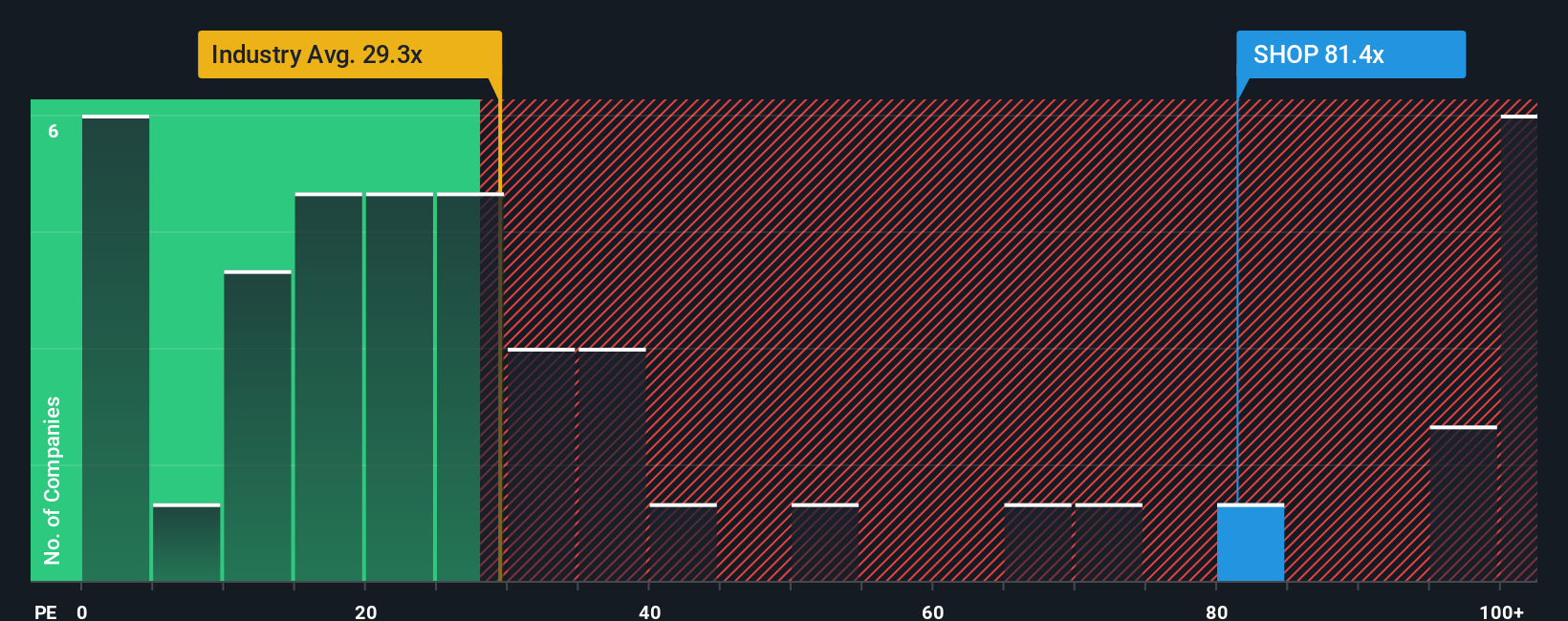

While the main narrative points to a fair value of $186.64 and argues that Shopify is undervalued, its current P/E ratio of 95.9 tells a completely different story. This is significantly higher than the US IT industry average of 27.6x, the industry average of 37.2x, and the 47.3x fair ratio that our model suggests is likely where the market is heading. Simply put, today’s investors are paying a premium multiple so that they have less room for failure if growth or margin falls short. Whether you value fair value based on earnings or richer earnings multiples depends on how familiar you are with that valuation range.

See what the numbers say about this price. Please check the rating breakdown.

Build your own Shopify narrative

If you want to see the story differently, or just want to weigh the numbers yourself, you can use Do it your way to build a new Shopify view in minutes.

A great starting point for any Shopify research is our analysis that highlights 3 key benefits and 2 significant warning signs that could influence your investment decision.

Looking for more investment ideas?

If Shopify is just one part of your watchlist, now is the time to widen your search and list a few more potential opportunities.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: Manage all your stock portfolios in one place

What we created is The ultimate portfolio companion For stock investors, And it’s free.

• Connect an unlimited number of portfolios and see the total in one currency

• Alert you to new warning signs and risks via email or mobile phone

• Track the fair value of stocks

Try our demo portfolio for free

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.