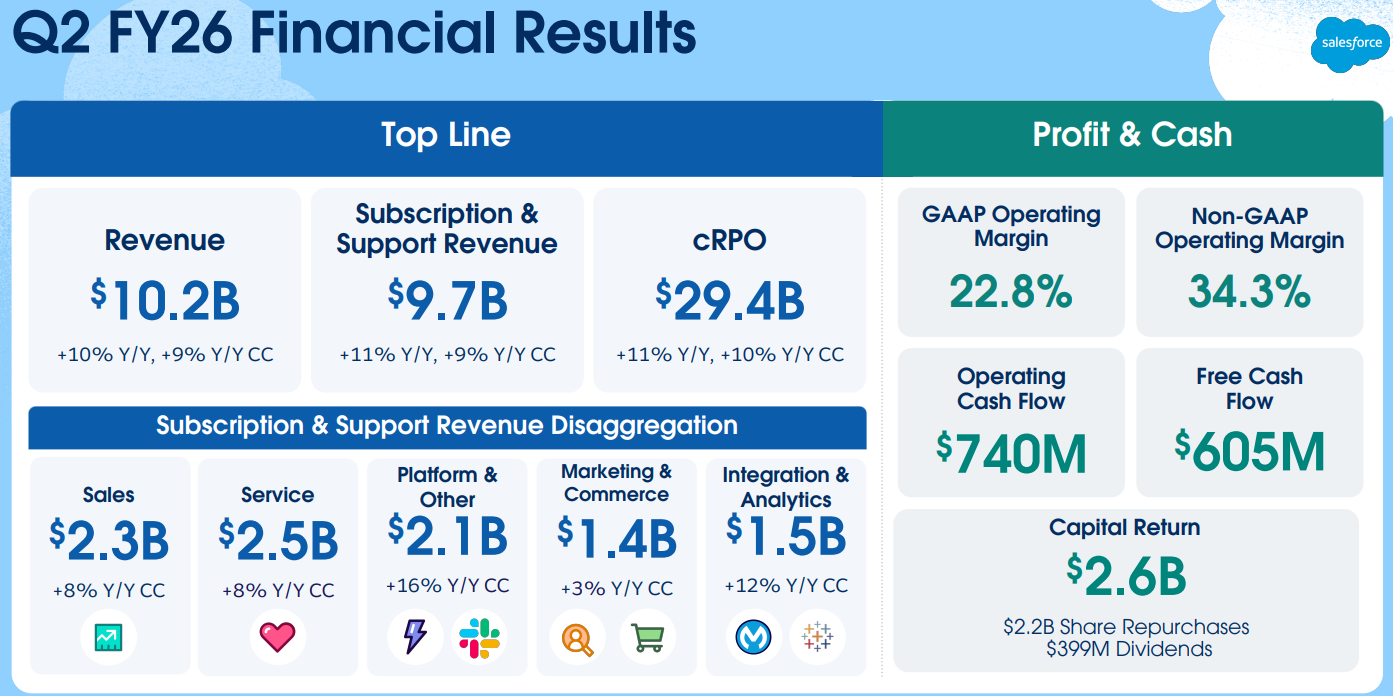

Salesforce has delivered a complex second quarter report that beats expectations for both revenue and revenue, but lacks guidance, which has led to a complex second quarter report that has dropped its stock by about 7% in pre-market trading. The company recorded adjusted earnings of $2.91 per share with analysts forecasting $2.78 and revenue of $10.2 billion. Net income rose to $1.89 billion from $1.43 billion a year ago. But despite the beat, management outlook for the October quarter disappointed investors, particularly on revenue growth and backlog metrics. Salesforce's decision to expand its stock buyback approvals another $2 billion highlighted its commitment to shareholder returns, but the careful revenue outlook over the positives, especially given the stock's struggle this year..

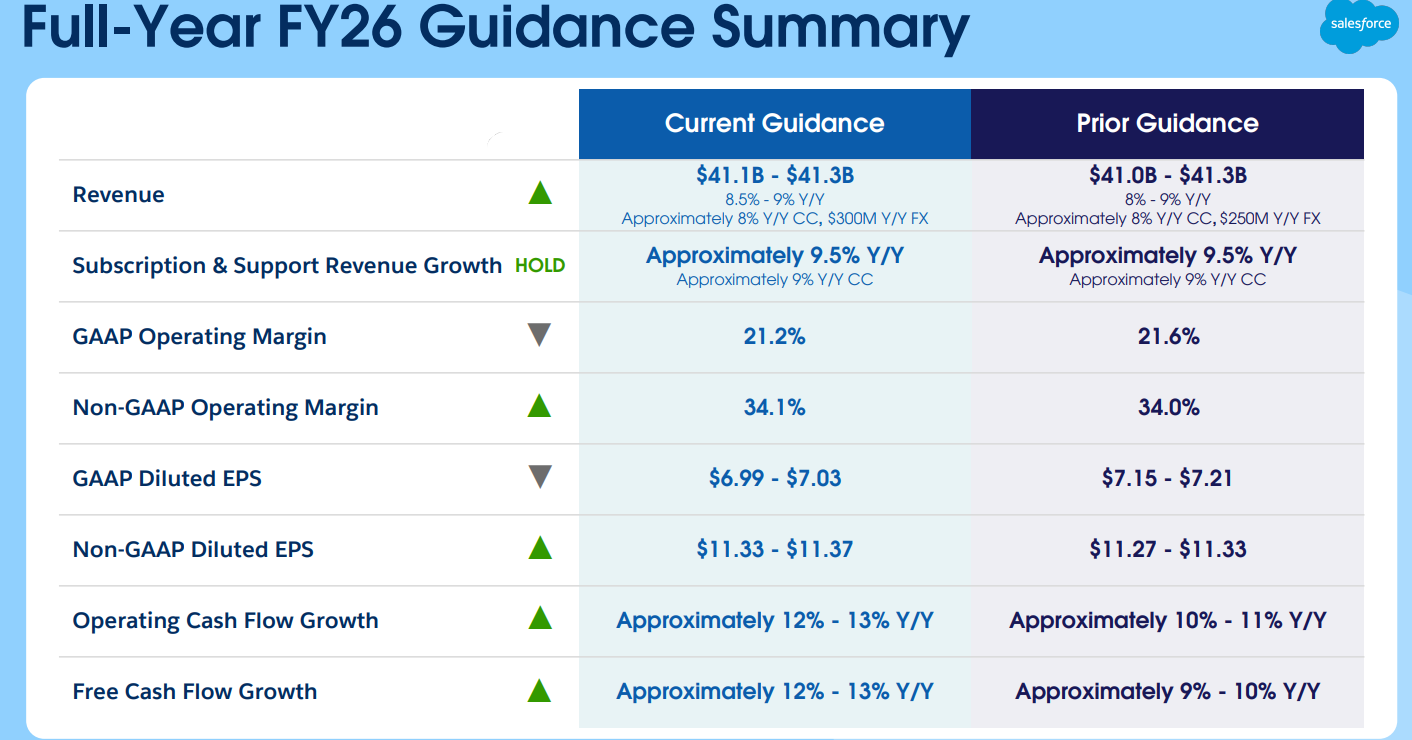

To break down the results, Salesforce's 10% revenue growth rate was stable, driven by strong performance in its core cloud and data cloud and AI momentum, with annual repetitive revenues increasing 120% year-on-year to $1.2 billion. In particular, the company has shown traction in its efforts to monetize artificial intelligence by closing 60 transactions worth more than $1 million, including both data clouds and AI products. The current remaining performance obligation (CRPO), a closely monitored backlog metric, rose 11% to $29.4 billion, slightly above estimates, providing relief at future demand. The operating margin is also bright, with the adjusted operating margin increasing by 34.3% and 60 basis points, while the GAAP margin rose to 22.8%, reflecting the ongoing efficiency initiative. However, management has raised the low end of its full-year revenue outlook to $41.1 billion, while the top end is stable at $41.3 billion, representing approximately 8% growth. This careful guidance sent a clear signal that short-term topline acceleration remains elusive.

For investors, the concern is clear. Salesforce has struggled to regain the growth spark that once became the name of the flying SaaS, and revenue has remained in single-digit range since mid-2024. Analysts and investors are not convinced that its AI initiative, particularly Agentforce, will create the explosive growth seen in peers such as Microsoft and Nvidia. CFO Robin Washington acknowledged the ongoing challenges of marketing and commerce products, as well as slow growth in some regions, allowing us to consider future performance. CEO Marc Benioff has taken the tone confident in Cole, claiming that demand for AI-driven SaaS is strong, but Wall Street's skepticism is evident in stock's performance.

From a technical standpoint, Salesforce stocks have gotten even worse. Heading towards revenue, the stock was testing resistance on a 50-day moving average, but the post-revenue decline decisively boosted both the 50-day and 20-day moving average. This breakdown further increases the risk of negative aspects, focusing on the lows in August at nearly $226 as a key level of support. It is the accumulation/distribution of stocks that exacerbate the technical weaknesses, suggesting that the institution has been a net seller for the past 13 weeks. That pattern suggests that large investors may be pulling back, reducing confidence in the sustainability of short-term bounce. The $226 test could serve as a litmus of whether buyers within the facility will recede or whether sales pressure will deepen.

However, despite these concerns, ratings could offer a backstop. Analysts note that the company's value for Salesforce's free cash flow multiple has been declining 10 years low, reflecting investors' concerns about disruption from AI-Native's competitors. This cheap profile could make stocks attractive to long-term buyers who are willing to see past short-term sluggishness, particularly as annually raised free cash flow guidance and $25 billion is now available in an expanded buyback program. Furthermore, heavy tech peers in stocks leave room for an average return, especially when sentiment improves, especially around AI adoption and the October Dreamforce meeting.

In summary, Salesforce's second quarter results were better than feared on paper, with solid beats in revenue, EPS and backlog metrics, but the guidance reinforced the narrative of slowing growth, and left investors were disappointed. Evidence of technical breakdown and institutional distribution suggests that pressure may last in the short term. However, in the long run, a combination of improved margins, AI momentum, and unusually inexpensive valuations can rekindle institutional interest, especially when Dreamforce brings positive surprises. For now, Salesforce remains caught up between a careful short-term foundation and the possibility of long-term reassessment, if AI initiatives begin to contribute meaningfully to growth. The path forward may be choppy, but both traders and investors are seeing if CRM will stabilize with support, or if this latest disappointment shows even more pain.