McDonald's Corporation (NYSE:MCD) released its 2023 Q4 earnings report on February 5th, leading to selling. However, at the time of writing, the stock was up 5.50% on a three-month basis even after falling 3.73%.

Zooming out even further, the stock is up more than 200% in 10 years. The decrease in profits could be justified as just a technical retracement and profit reduction. In fact, there is nothing in the financial report that can point directly or indirectly to a company's mistakes or strategic flaws. My investment theory is that, given the unwarranted stock price decline, attractive future valuations, new CosMc concepts, and the exciting implementation of artificial intelligence in business, the stock price is now on the rise for future investors who missed out on the year-end stock price rally. So it's at an interesting entry point. .

Earnings Bounce: Opportunity to Jump on a Trade at the Last Hour

Let's take a closer look at the reported earnings. Earnings per share (EPS, company earnings per share outstanding, or net income), came to $2.95, beating the Street's estimate by $0.13. This is a staggering 18% increase over the previous year (YoY comparison), especially for a company this large. The reason for the stock price drop was disappointing sales. Sales were $40 million lower than expected. Considering $6.41 billion in revenue, that's a margin of error of 0.6% (a whopping 8.1% year-over-year increase). Wall Street can be picky, and the market doesn't tolerate the slightest mistake. As mentioned above, from a quantitative perspective the mistake is minimal and there is no way it could justify erasing $6 billion of market capitalization. In reality, the nature of the mistake may be a more important issue. In fact, McDonald's is an international company with presence all over the world. The ability to adapt menus to local cultures has been key to the company's expansion across all continents and has supported the company's continued growth. Therefore, events outside the United States can have a material financial impact. Looking at quarterly same-store sales in various regions, we found that the U.S. saw a 4.3% increase versus the expected 4.45%, while overseas expectations were higher (4.79%) and only 3.4% was achieved. I missed it significantly. The decline in overseas sales is the cause of the decline in stock prices, and the biggest concern is the situation in the Middle East, especially the Israeli-Hamas conflict, which is the reason for the decline in overseas sales.

McDonald's Israeli franchisees announced on Instagram plans to provide thousands of free meals to Israeli soldiers during the conflict with Hamas, sparking a huge controversy on social media. The announcement was surprising because McDonald's has long maintained neutrality in disputes, which has been key to its worldwide presence of more than 41,000 stores in more than 100 countries. The decision sparked massive boycotts in Muslim countries with large populations and growing markets, namely Malaysia and Indonesia. The wave of boycotts also reached France, one of its largest and most profitable markets.

In my opinion, the reason why the market sold the stock was a short-term situation and a short-lived event. Even if the boycott continues, the downside is limited as it is unlikely to escalate further (the peak of the boycott was the day after the controversy). More importantly, McDonald's revenues depend more on food sales than real estate operations, which reduces the further downside of boycotts. Harry J. Sonneborn, an early McDonald's insider, once said, “We (McDonald's) are not strictly in the food business.” We are in the real estate business. The only reason we sell 15 cent hamburgers is because hamburgers are our biggest source of revenue and our tenants can pay their rent from it.

McDonald's is first and foremost a real estate business. Of the more than 41,000 stores I mentioned earlier, only just over 2,000 are operated by his company (the rest are operated by franchisees). The company provides products to its franchisees, and the franchisees sell the products and pay rent to the company. In 2021, rental income accounted for more than one-third of total revenue, becoming the fast food chain's main source of income. This is the real moat of your business against your competitors. Premium ratings reflect the quality of your business.

Great company with attractive prospects reflected in generous valuations

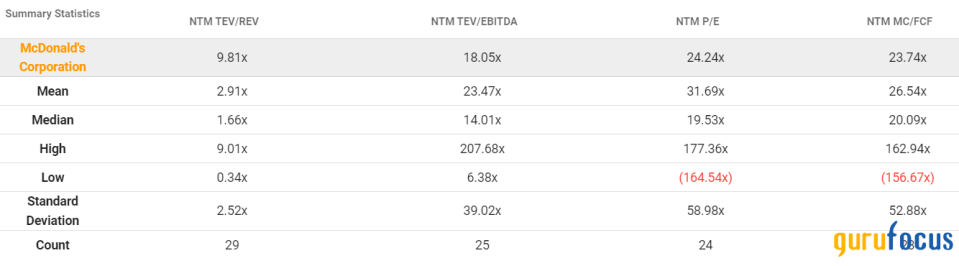

Compared to the broader fast-food industry operated by competitors such as Yum Brands (NYSE: YUM), Chipotle (NYSE: CMG), and Starbucks (NASDAQ: SBUX), McDonald's ranks fairly highly. Based on the movement of stock prices, stocks become richer and richer over time.

Source: TIKR.com

A decade ago, the stock was valued at less than 4 times trailing 12-month revenues and approximately 10 times EBITDA. It is now about double, which means that the stock price has doubled compared to 10 years ago. The reason why the valuation is rising is because of the moat I explained earlier. The company has been able to mitigate the cyclical nature of its food business with a fixed portion of its revenue derived from franchisees' rental income. The company's growth prospects have also improved year on year, and its sales, EBITDA, profit, and free cash flow multiples are all above the sector median, giving it a premium valuation.

Source: TIKR.com

In my opinion, this high valuation is also justified by exciting innovations. McDonald's has launched a new concept that is being introduced in several U.S. stores and is named after the company's little-known mascot from the 1980s, “CosMc.” This new chain, CosMc, focuses on beverages and snacks and clearly aims to be an undeclared competitor to Dunkin' Brands (DNKN) and Starbucks. The latter has been repeatedly criticized for raising prices unbearably in an environment of high inflation. CosMc has proven to be a huge success in its first open store. This store saw three times as many customers per square foot as the average McDonald's restaurant.

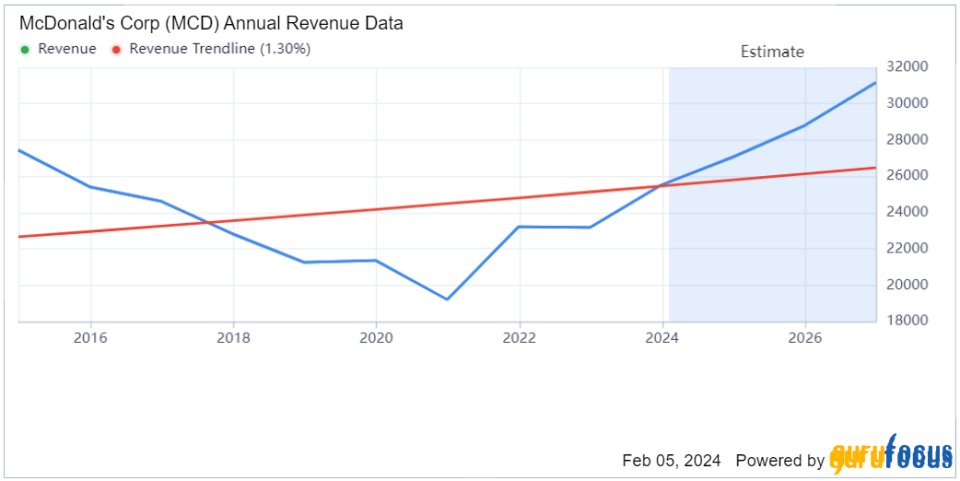

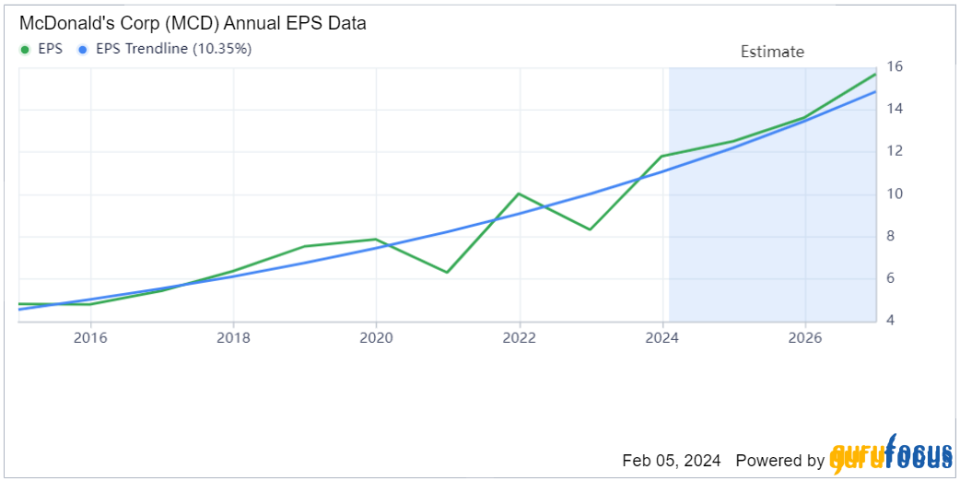

Last but not least, there is another exciting innovation underway when it comes to artificial intelligence. In December, McDonald's announced a partnership with Alphabet (NASDAQ:GOOG) and Google to gradually roll out its AI system in the U.S. through 2024. For now, the project is pretty secretive, with little public information about it. McDonald's has so far said its aim is to provide customers with warmer, fresher food and help operators quickly find and implement solutions to reduce business interruptions. only declared. AI systems could help with ordering, perhaps speeding up order processing, and in some ways could even fill in for staff vacancies. It is not impossible that the introduction of AI could reduce the number of employees and increase profits. These innovations are still in the implementation phase and it may take months, or even years, for their positive impact to be reflected in your finances. What is certain is that the revenue growth outlook and earnings per share growth forecast continue to improve, as shown below.

CosMc and AI could boost revenue growth with significantly above-trend line performance.

Earnings per share are also expected to be above the 10-year trendline.

These events could invalidate my bull case

Despite these great prospects and fundamentals, my bullish case could be invalidated if McDonald's becomes too political. In fact, this company has been able to expand its presence and, thanks to its ability to adapt to local culture and consistently ignore its involvement in geopolitical debates, is unparalleled, with the exception of perhaps Yams KFC. It has become a brand.

Additionally, the new CosMc pilot project and Google AI partnership are too uncertain to model cash flow growth projections for 2024. If they prove unprofitable, one or both projects could cause him to increase his spending in 2024.

conclusion

McDonald's is a great and highly regarded company for the restaurant industry. In my view, this return does not justify the decline in the stock price, thus providing a great opportunity to enter into a position or continue accumulating the stock. Despite the cyclical nature of the business, the continued growth in the number of franchisees and the rental income generated therefrom provides a reliable basis for the company's financial health. Exciting pilot projects like CosMc and the Google AI partnership provide reassurance that the stock is likely to remain highly valued and the business will continue to grow.

This article first appeared on GuruFocus.