NVIDIA (NVDA) is back in the spotlight after executing on AI-driven catalysts, including its Project Glasswing cybersecurity work and new data center and OEM partnerships, even as investors weigh export controls and increased competition.

Check out our latest analysis for NVIDIA.

The stock has gained renewed momentum on the back of new partnerships and AI infrastructure deals, with a one-day stock return of 2.57% and a seven-day stock return of 6.34%, with five-year long-term total shareholder returns still exceeding 10x.

If you’re looking for other AI infrastructure names besides NVIDIA that would benefit from similar themes, now is a good time to explore the market with 36 AI Infrastructure Stocks.

NVIDIA trades at $188.63, and while analyst targets suggest significant upside, with long-term returns already exceeding 10x over five years, the key question is simple. The question is, is there still a buying opportunity here, or is future growth fully priced in?

Most popular story: 10.8% overrated

The most popular view on NVIDIA is that the current price already includes ambitious expectations, with a narrative fair value of $188.63 compared to $170.26.

The $400 billion in annual revenue assumes Nvidia continues to dominate in GPU design and AI software stacks. Successful competition from AMD, Intel, or Chinese companies could ruin this. Adopting an open source platform that is cheaper or better than Nvidia’s CUDA would seriously undermine Nvidia’s moat and allow it to steal Nvidia’s high-margin products by contracting directly with semiconductor manufacturers like TSMC to produce its own chips, much like Apple did with its M-series chips.

Read the whole story.

Want to see how revenue targets, margin profiles and profit multiples fit together? According to KiwiInvest, the entire valuation relies on some bold operating assumptions.

Result: Fair value $170.26 (overvalued)

Read the full explanation to understand what’s behind the predictions.

However, a significant slowdown in AI spending, data center capacity expansion, or CUDA dominance could challenge these assumptions and reset expectations about Nvidia’s long-term potential.

Find out about the key risks to this NVIDIA story.

Another way to look at it: multiple market opinions are “high value”

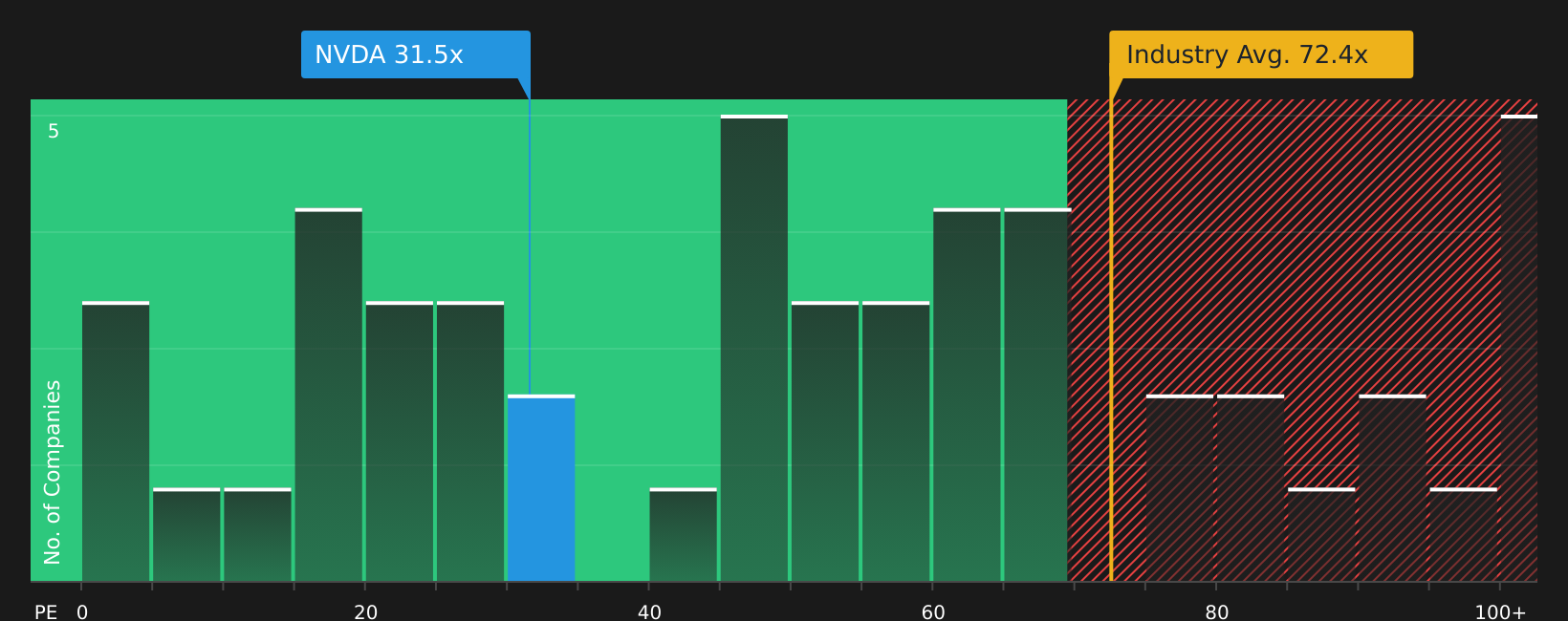

Considering the 10.8% premium to KiwiInvest’s fair value of $170.26, NVIDIA’s current P/E ratio of 38.2x looks more generous. At 95.3x, it is significantly lower than other companies in the same industry, and below a fair ratio of 46x. This suggests there is less room for valuation growth than the story suggests.

See what the numbers say about this price. Please check the rating breakdown.

next step

With mixed signals about values and expectations, it makes sense to see the big picture for yourself and act quickly if you find a discrepancy. Start with a breakdown of 4 major perks and 2 important warning signs.

Looking for more investment ideas?

If NVIDIA is already in your portfolio or watchlist, expand your options now so you’re no longer dependent on a single AI story to drive revenue.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

Evaluation is complex, but we will simplify it here.

Discover whether NVIDIA is undervalued or overvalued with our in-depth analysis. Fair value estimates, potential risks, dividends, insider transactions, and financial condition.

Access free analysis

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.