Meiko Electronics (TSE: 6787) has announced plans for a business alliance with Allied Circuit, aiming to grow the AI server market. This partnership will create a new Vietnamese joint venture and manufacturing facility.

Check out the latest analysis from Meiko Electronics.

Meiko Electronics' latest strategic partnership with Allied Circuit arrives at a fascinating moment, with a positive momentum muted total shareholder return rate of 0.57% in the ambitious expansion plan. The announcement could mark a turning point in market sentiment as investors weigh the growth potential of the AI server sector against the recent stability of the stock price.

If this moves to AI hardware, if it piques your interest, you can see how other tech innovators are moving forward. Check out the complete list for free.

Given the solid foundations of Meiko Electronics and current discounts on analyst price targets, the question for investors is whether this strategic expansion presents an undervalued growth story, or whether the market is already priced in the next chapter.

From 15.8x price to revenue: Is it justified?

Meiko Electronics sells on a large amount of revenue from 15.8x the price, so investors are paid slightly less for each unit of revenue compared to peer groups, but is a premium and a peer average for the wider industry. The latest close price at 9,450 yen is below the target of analysts, making this an interesting rating setting.

The price-to-revenue ratio measures how willing an investor pays for each yen in current revenue. It specifically communicates for established tech manufacturers like Meiko Electronics, as it reflects the balance of revenue quality, growth outlook and the broader market sentiment towards the company's core business.

At 15.8x, Meiko stands as a relative value compared to the peer average (17.3x). This suggests that the market is not exaggerating its growth and profitability outlook and its direct competitors. However, this multiple appears to be expensive for the overall Japanese electronics industry (14.2 times). This indicates that the market is allocating a modest premium. This is potentially driven by Meiko's market profit growth and improved margins. In particular, this multiple is still below our estimated fair price vs. return rate (21.5x), meaning there may be room for reassessment if the story of strengthening profitability and market conditions remains supportive.

Explore Meiko Electronics' SWS fair ratios

Results: From 15.8x Price to Revenue (Right)

However, competitive pressures in uncertainty over the AI hardware space and the global supply chain could quickly change Meiko Electronics' current trajectory.

Find out about the key risks to this Meiko Electronics story.

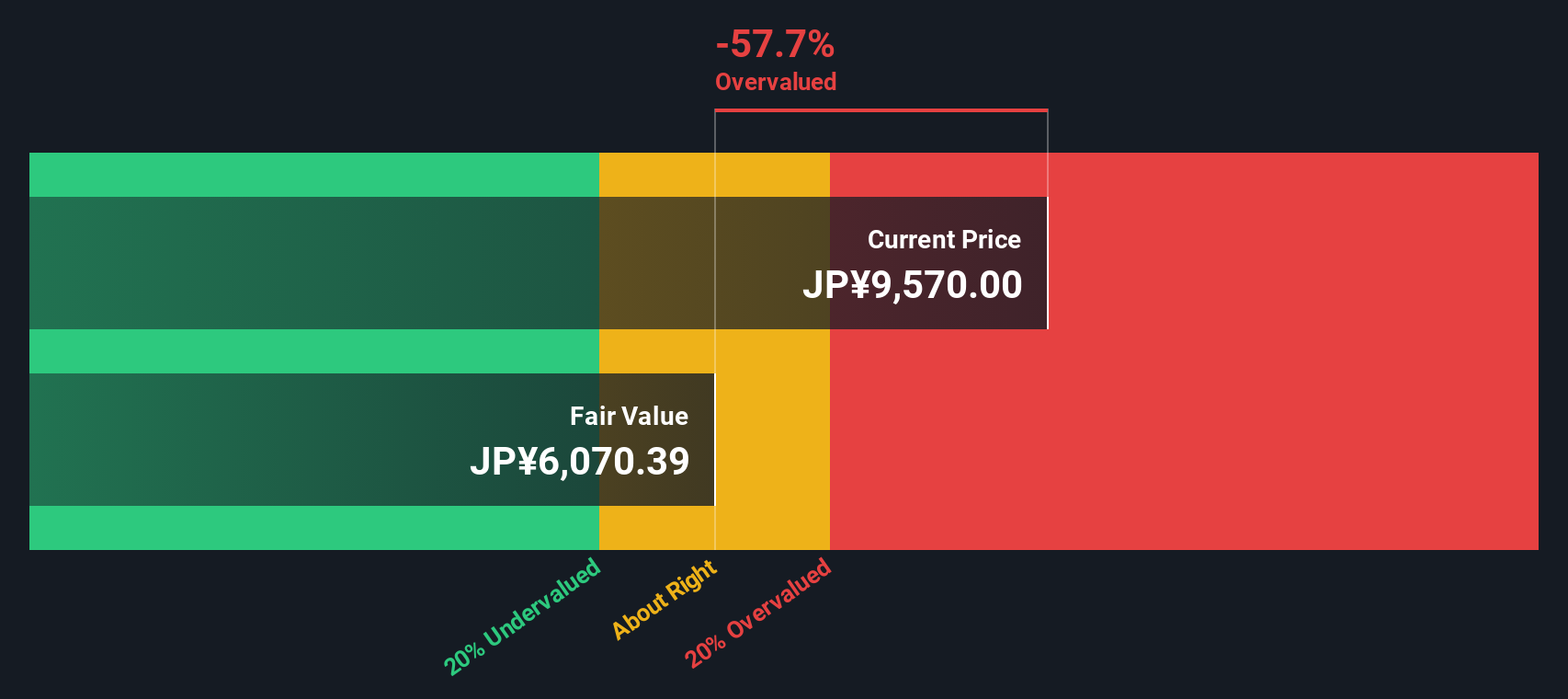

Another view: SWS DCF model suggests overestimation

While valuations based on multiples of revenue suggest potential rises, the SWS DCF model offers a different perspective. This suggests that Meiko Electronics may be trading beyond its estimated intrinsic value, suggesting that the market may be overestimating its future cash flow. Facing uncertain growth, can multiples be misleading?

Find out how the SWS DCF model reaches fair value.

Simply Wall St performs discounted cash flows (DCFs) on any inventory around the world every day (check out Meiko Electronics, for example). This complete description of the entire calculation. You can track your results in a watchlist or portfolio and alert you when this changes, or use a stock screener to discover undervalued stocks based on cash flow. When you save a screener, you may even warn you when a new company matches. So you won't miss out on potential opportunities.

Build your own Meiko Electronics story

If things look different or you prefer to dive into the details yourself, you can create your own analysis in minutes. Do it your way.

A great starting point for Meiko Electronics' research is an analysis that highlights two important rewards and two important warning signs that can influence investment decisions.

Looking for more investment ideas?

Don't miss out on stocks that make headlines for the right reasons. Simply use Wall Street's powerful screeners to find fresh opportunities to electrify your portfolio.

This article simply by Wall Street is inherently common. We provide commentary based on historical data and analyst forecasts, and use impartial methodologies, and our articles are not intended for financial advice. It is not a recommendation to buy or sell stocks and does not take into account your goals or financial situation. We aim to deliver long-term intensive analysis driven by basic data. Please note that the analysis may not take into account the latest price-sensitive company announcements and qualitative material. Simply put, the Wall ST has no position in the stock mentioned.

new: Manage all your inventory portfolios in one place

I've created it The ultimate portfolio companion For stock investors, And it's free.

Connect unlimited number of portfolios and check totals in one currency

•Announce new warning signs or risks via email or mobile

•Track the fair value of your inventory

Try our demo portfolio for free

Do you have feedback in this article? Are you worried about the content? Please contact us directly. Alternatively, please email editorial-team@simplywallst.com