Papers recently published in magazines Math investigated the feasibility of using a hybrid quantum-classical model developed by incorporating a quantum layer into a classical neural network to improve credit scores.

The importance of quantum machine learning

Research in quantum physics in finance/quantum finance has revealed potential applications in several areas such as risk analysis, portfolio optimization, and option pricing. Quantum finance leverages quantum machine learning and quantum computing to tackle complex financial calculations such as market trend analysis and risk management.

This work primarily focuses on credit scoring, which is an important financial task with considerable economic impact. Several studies have been conducted to improve machine learning models for credit scoring, especially for small and medium-sized enterprises (SMEs). Existing sophisticated models have limitations in accurately predicting bankruptcies, resulting in a significant number of solvent companies being incorrectly rejected.

Moderate enhancements to these models can reduce false rejections and significantly reduce lender risk. Such improvements can be achieved by applying quantum machine learning, a blend of quantum computing and machine learning, to financial analysis.

Quantum machine learning can significantly speed up data analysis by leveraging the principles of quantum physics. Despite the lack of formal theoretical underpinnings, his algorithm's search for superior heuristics in specific problem areas through domain expertise and cross-disciplinary insights is a breakthrough in quantum machine learning for finance. is important to achieve.

Proposed approach

In this study, researchers investigated the integration of quantum circuits and classical neural networks to improve credit scores for small businesses. Specifically, a new architecture that combines quantum variational circuits (VCs) and data reupload classifiers (DRCs) in a hybrid classical quantum neural network covers approximately 2,300 small and medium-sized enterprises founded after 1940. Applied to a real credit default dataset of Singaporean companies. 2016 period.

A proposed heuristic approach, the full hybrid (FH) classical quantum neural network model, was introduced with a focus on the synergy between classical and quantum models. Its performance was compared to a pure classical machine learning model/classical counterpart (CC) in credit scoring on a classical credit default dataset to demonstrate the potential of quantum machine learning .

Small and medium-sized enterprises were chosen because they often do not have formal credit ratings. The aim of the research was to improve the accuracy of financial-related predictions and explore the practical applications and theoretical limits of quantum-enhanced data analysis. In the proposed FH or neural network (NN)/VC-DRC model, the first part is a classical NN, followed by a VC-DRC circuit and a final decision layer (a single neuron layer with a sigmoid activation function). Continue.

Classical NN contains 2 neuron layers/master classical layer with modified linear activation function (ReLU) followed by another 2 neuron layer with Leaky ReLU activation function/feeding classical layer continued. Finally, the classical decision layer/final decision layer made the predictions.

After every classical layer, a dropout layer was added to both CC and quantum models with a dropout rate of 10% to prevent overfitting. Angular embeddings were used to encode the data into quantum states. Additionally, data preprocessing was performed using standard pipelines and proprietary processing before using the data as model input. Quantum computer noise is absent due to the use of the simulator, and no other noise was introduced in the experiment.

Evaluation and results

The performance of the quantum model was evaluated against the CC model and the number of blocks and qubits. Researchers used the same test, training, and validation datasets throughout the simulation.

Additionally, the average result of the receiver operating characteristic (ROC)/area under the ROC curve (AUC) score of the five simulations was used for each configuration. To ensure a fair comparison, the number of epochs for both classical and quantum models was kept at 350.

The results showed that incorporating quantum layers into traditional neural networks significantly reduces training time. His proposed NN/VC-DRC hybrid model achieved efficient training in significantly fewer epochs compared to the CC model achieving similar prediction accuracy.

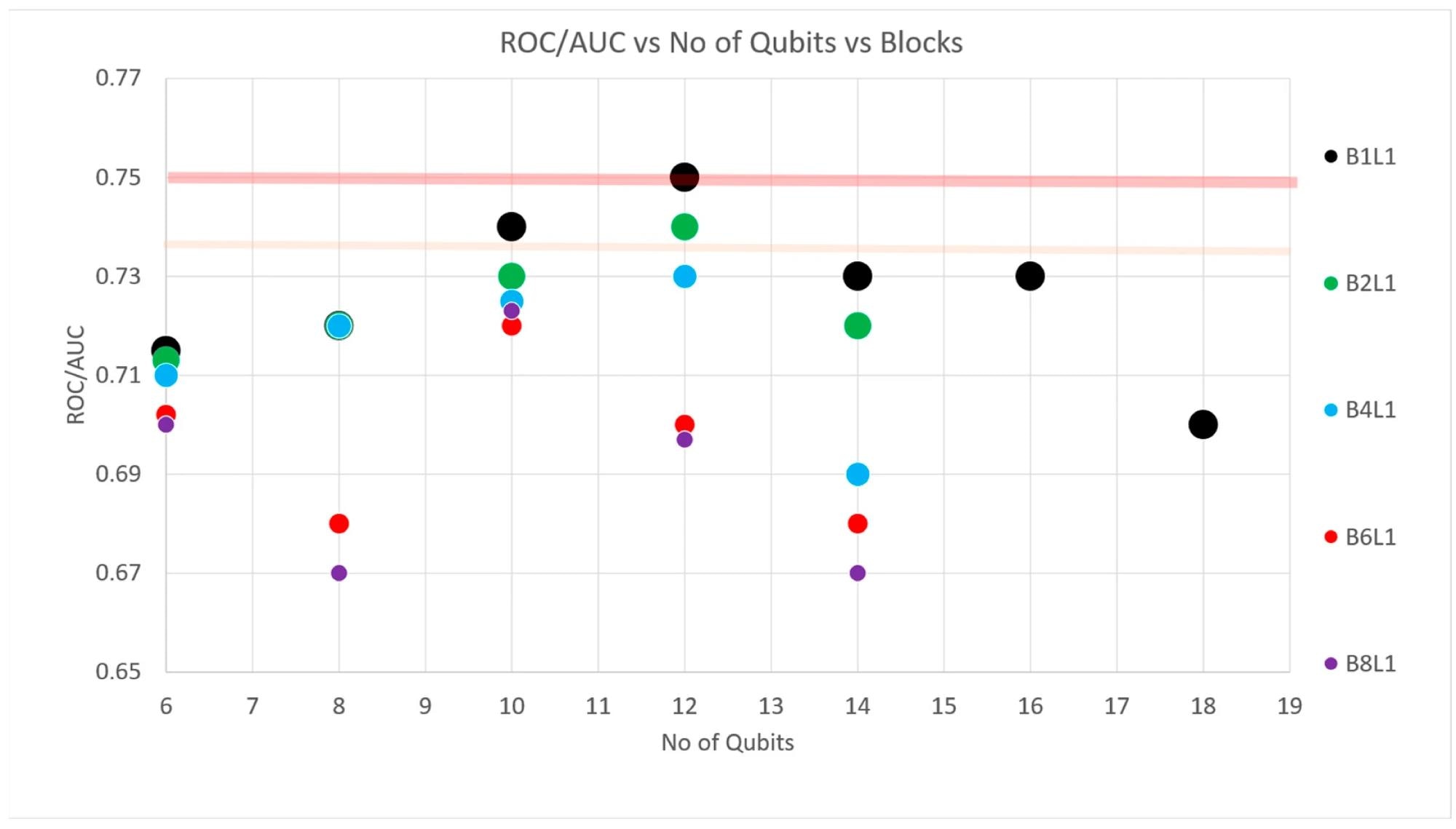

For example, the FH model achieved a ROC/AUC of 0.75 with 350 epochs, while the CC model achieved the same ROC/AUC score of 0.75 with 3500 epochs. Similarly, the performance of the FH model was affected by changes in the number of blocks and qubits.

For example, the ROC/AUC of FH increased up to 12 qubits with block = 1 and decreased beyond 12 qubits. The same behavior was observed when the number of blocks increased and the best result/best performance was achieved without doing anything. Re-upload data.

In summary, the results of this study demonstrated that the proposed quantum-classical hybrid model for credit scoring has great potential in the financial sector. However, to advance the use of quantum machine learning algorithms in real-world applications, two key challenges must be addressed, including the over-parameterization problem in quantum circuits and the sterile plateau phenomenon, which can affect accuracy. need to do it.

Journal reference

Shetakis, N., Agamaryan, D., Boguslavsky, M., Rees, A., Rakotomalala, M., and Griffin, P. R. (2024). Quantum machine learning for credit scoring. Math, 12(9), 1391. https://doi.org/10.3390/math12091391, https://www.mdpi.com/2227-7390/12/9/1391