- Wondering if Snowflake’s high reputation matches its actual value? You’re not alone. If you look beyond the headlines, the answer becomes even more nuanced.

- The stock has increased 59.5% since the beginning of the year, but has fallen 7.4% in the past month. This highlights how quickly risk perceptions can change, even for popular stocks.

- Recent headlines highlight Snowflake’s ambitious moves, including announcing partnerships with leading AI innovators and expanding its product ecosystem. These developments have triggered both bullish and bearish reactions, and investors’ attention remains high as the company is positioned to compete more directly with larger cloud players.

- Snowflake currently has a score of 0/6 on our reputation check, indicating that it’s not undervalued according to our standard measures. Next, we’ll explore what these techniques show and an alternative approach to interpreting Snowflake’s valuation in today’s volatile markets.

Snowflake received just a 0/6 rating. See what other red flags we found in our full rating breakdown.

Approach 1: Snowflake Discounted Cash Flow (DCF) Analysis

Discounted cash flow (DCF) models estimate a company’s intrinsic value by predicting future cash flows and discounting them to today’s value. This reflects current values. In the case of Snowflake, the model uses a “two-stage free cash flow to equity” approach, utilizing both analyst forecasts and extrapolated forecasts to estimate future growth.

Snowflake currently generates free cash flow of $726.87 million. According to analysts, this figure is expected to grow rapidly, reaching $1.12 billion in 2026 and $1.48 billion in 2027. Starting in 2027, Simply Wall Street’s methodology further estimates future free cash flow, estimated at $3.26 billion by 2030. These growth rates indicate strong optimism for the expansion of Snowflake’s business and market reach.

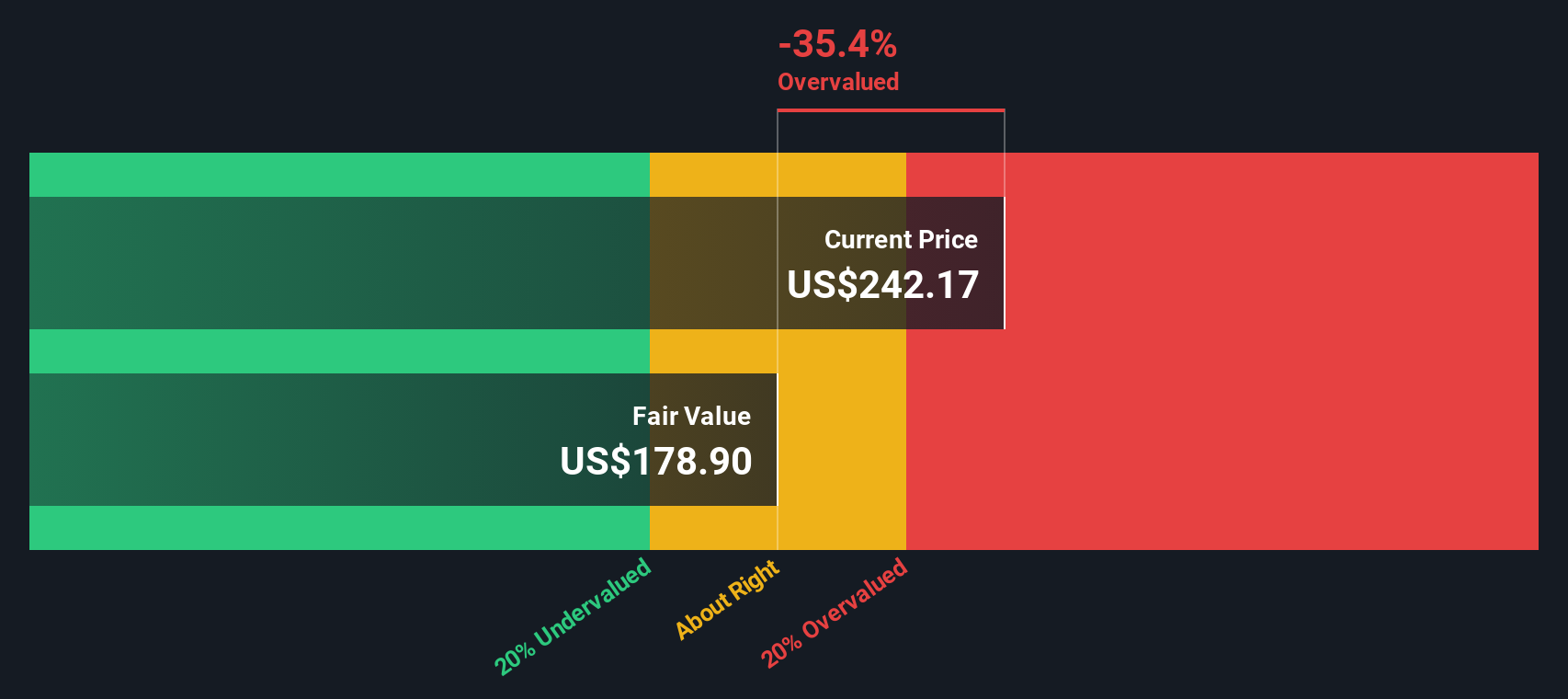

Using these projected cash flows, the DCF model arrives at an estimated fair value of $182.63 per share. However, a comparison to Snowflake’s current market value suggests that the stock is overvalued by 37.6%.

Based on this DCF analysis, Snowflake shows solid growth potential, but the current stock price may not leave much room for error or further upside.

Result: Overestimation

Our discounted cash flow (DCF) analysis suggests that Snowflake may be overvalued by 37.6%. Discover 920 undervalued stocks or create your own screener to find more valuable opportunities.

For more information on how we calculated this fair value for Snowflake, please see the Valuation section of our report.

Approach 2: Snowflake price and sales

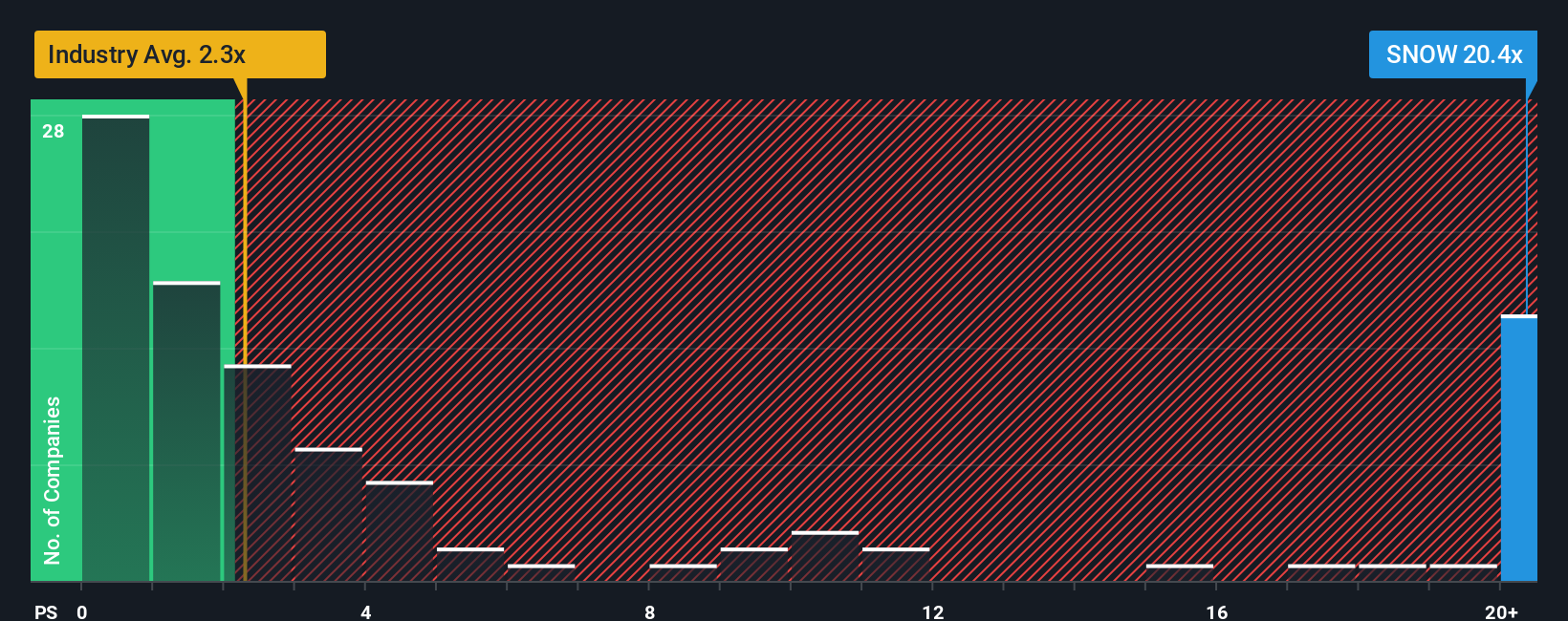

For fast-growing technology companies like Snowflake, the price-to-sales (P/S) ratio is often the preferred metric, as many companies are still investing heavily in growth and may not yet have stable profits. The P/S ratio allows investors to value these companies relative to their earnings. Revenue typically grows much faster than profits at this stage.

What is a reasonable P/S ratio depends on several factors, most notably expectations of future sales growth and level of risk. Higher growth rates usually justify a higher P/S, but higher risk or lower growth rates require lower multiples. Snowflake currently trades at 20.68 times sales. To put this into context, the industry’s average P/S is just 2.68x, while its direct peers’ average P/S is 20.17x.

Simply Wall St’s exclusive ‘Fair Ratio’ is designed to exceed these comparisons. Fair ratios weigh a company’s profitability, future growth potential, industry dynamics, market capitalization, and risk profile, providing a holistic perspective on where multiple factors should land, especially for Snowflake. Taking these nuances into account provides a more accurate baseline than simply comparing to peers or the broader industry.

Snowflake’s fair ratio is 15.06x, which is below its current P/S. This suggests that Snowflake stock is trading at a premium relative to what its growth and risk profile may justify.

Result: Overestimation

The PS ratio tells one story, but what if the real opportunity lies elsewhere? See the 1,438 companies where insiders are betting big on explosive growth.

Upgrade your decision making: Choose your snowflake story

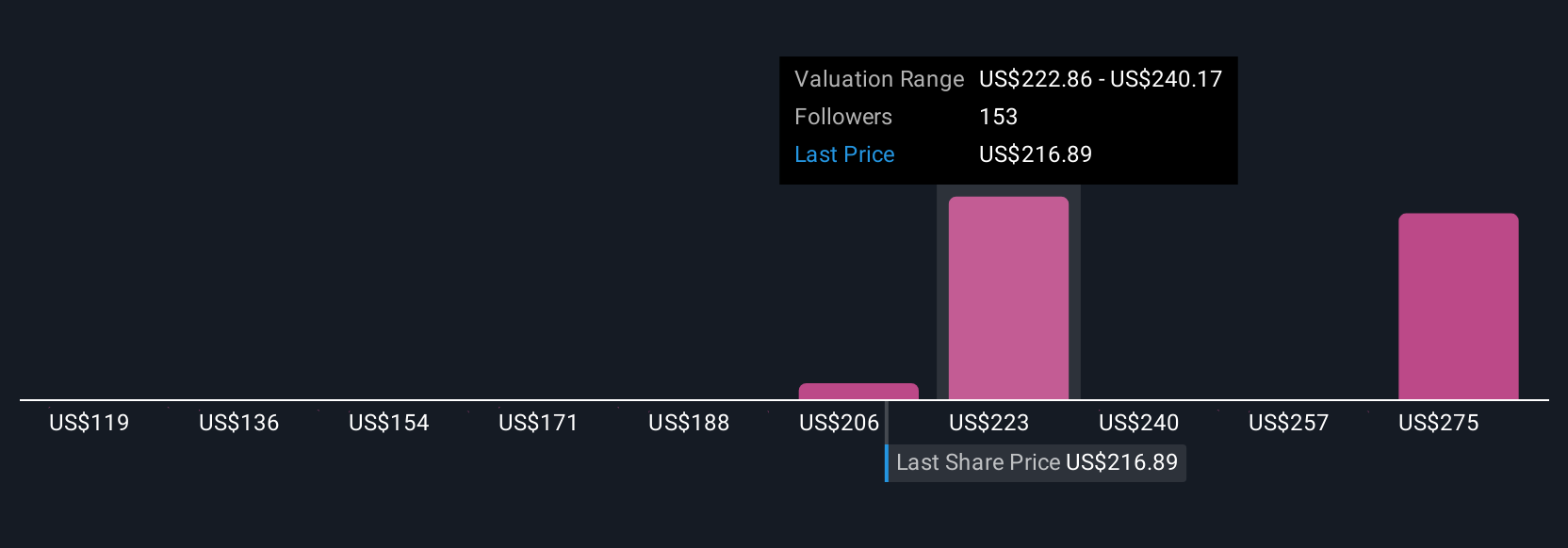

I mentioned earlier that there is a better way to understand valuation. So let me introduce the narrative. A narrative is simply your story, your perspective on the future of your company, distilled into the numbers you expect for revenue, profits, and profits. Here, we’ll combine everything we’ve learned about the company with financial projections and see how that translates to fair value.

Narratives allow you to go beyond headline analysis by building your own view and seeing how the stories you believe compare to current prices. On Simply Wall St’s community page, investors of all experience levels use narrative as an intuitive tool to determine whether a stock is undervalued, fairly priced, or overpriced. Automatically updates as news and results are published, keeping your narrative relevant in a rapidly changing market.

For example, the most optimistic Snowflake narrative sees the stock rising toward $440 based on explosive AI-driven growth, while the most cautious narrative values the stock at $170, reflecting competitive and margin risks. This approach allows us to compare ratings to the extremes and the consensus in between.

Do you think there’s more to Snowflake’s story? Visit our community to see what others are saying.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: Manage all your stock portfolios in one place

What we created is The ultimate portfolio companion For stock investors, And it’s free.

• Connect an unlimited number of portfolios and see the total in one currency

• Alert you to new warning signs and risks via email or mobile phone

• Track the fair value of stocks

Try our demo portfolio for free

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.