- Have you ever wondered if Baidu is undervalued, or if the market is finally catching up to its true potential? A closer look at its valuation might provide some interesting insights.

- The stock has increased 44.8% since the beginning of the year and 39.2% over the past year. The stock has gained 1.6% over the past seven days, indicating renewed investor interest.

- Recent headlines have focused on Baidu’s advances in artificial intelligence and partnerships to expand its cloud services, contributing to optimism about the company’s growth prospects. Market sentiment is shifting as investors weigh the broader technology recovery against competitive pressures from peers.

- When it comes to traditional rating checks, Baidu only gets a 1 out of 6 as undervalued. In this article, we’ll use different approaches to explain what that means, and finally highlight the key factors to consider when valuing a stock.

Baidu’s rating is only 1/6. See what other red flags we found in our full rating breakdown.

Approach 1: Baidu discounted cash flow (DCF) analysis

Discounted cash flow (DCF) models estimate the value of a company by discounting expected future cash flows to their current value. In Baidu’s case, this method uses a two-stage free cash flow-to-equity model to assess a company’s potential.

Baidu’s trailing-12-month free cash flow (FCF) is currently negative C$13.7 billion, reflecting recent cash outflows as the company continues to invest in its growth initiatives. Nevertheless, analysts expect an upturn, with annual FCF expected to rise significantly and reach CA$20.3 billion by the end of 2028. Extrapolated projections over the next 10 years show that FCF is steadily increasing, although year-to-year growth varies. Simply Wall St uses analyst forecasts for the first five years and relies on an internal approach to extend the forecasts from 2029 to 2035.

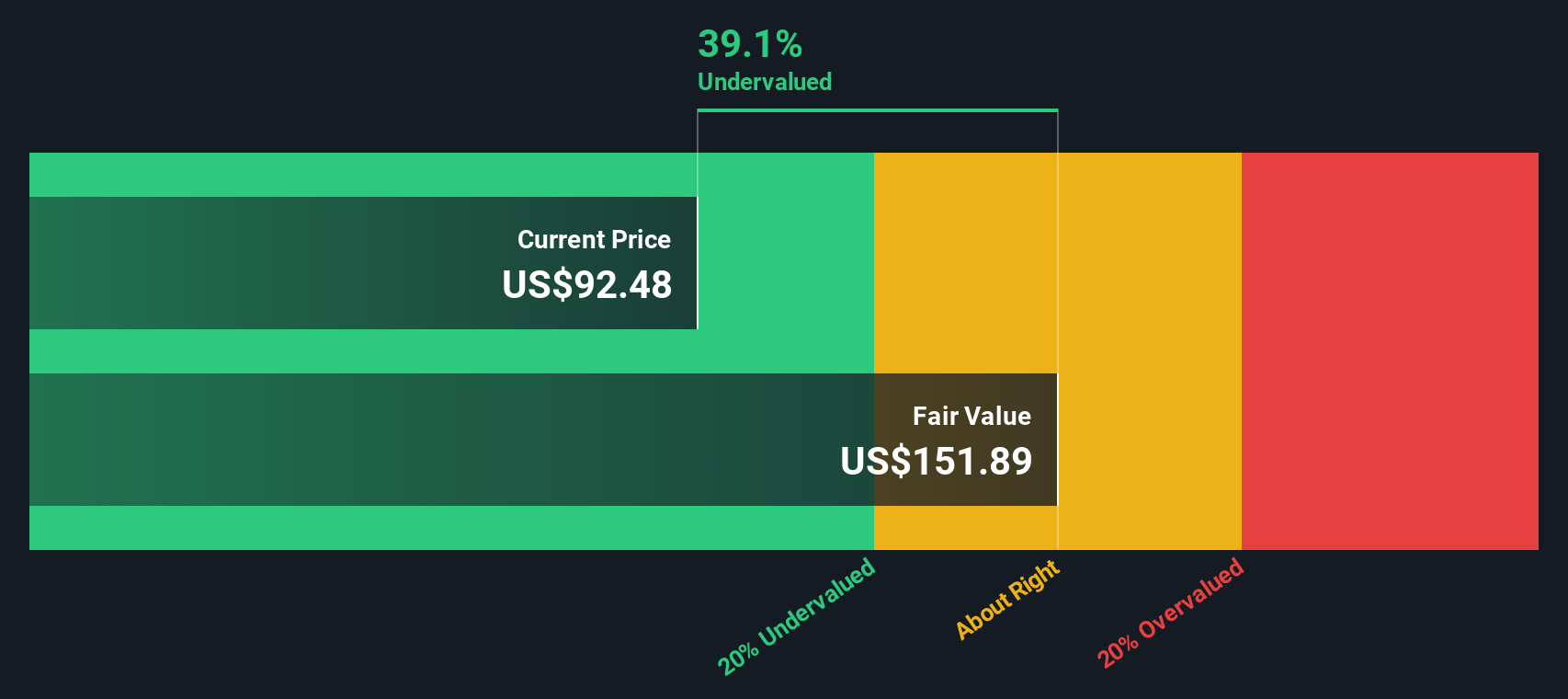

After discounting these numbers to their present value, the DCF analysis yields an estimated intrinsic stock value of $99.18. Considering Baidu’s current market price, the model shows that the stock is overvalued by approximately 20.7%.

Result: Overestimation

Our discounted cash flow (DCF) analysis suggests that Baidu may be overvalued by 20.7%. Discover 929 undervalued stocks or create your own screener to find higher value opportunities.

To learn more about how we arrived at this fair value for Baidu, please see the Valuation section of our company report.

Approach 2: Baidu price and profit (PE)

For profitable technology companies like Baidu, the price-to-earnings ratio (PE) is widely recognized as a valuation tool. P/E multiples reflect how much investors are willing to pay for each dollar of current earnings, so if a business is generating positive profits, it can quickly give you a sense of relative value.

What determines a “fair” P/E ratio is influenced by factors such as future growth expectations, profitability, and perceived risk. Companies with expected rapid earnings growth often have high P/E ratios, while companies with stagnant or unpredictable prospects tend to have low P/E ratios.

Currently, Baidu’s P/E ratio is 34.6x, which is significantly higher than the Interactive Media and Services industry average of 16.0x, but lower than the peer average of 61.3x. This suggests that while the stock trades at a premium to the broader sector, it is valued more conservatively than some of its closest competitors.

Simply Wall St’s own fair ratio to Baidu is 32.8x. The metric goes beyond simple peer and industry comparisons by taking into account Baidu’s unique revenue growth profile, industry position, profit margin, market capitalization, and risk factors. Designed to provide a more balanced view of valuation than typical market multiples.

Comparing Baidu’s actual PE multiple (34.6x) and fair ratio (32.8x), the stock appears to be roughly valued, as the difference between these two numbers is almost negligible.

Result: Almost correct

The P/E ratio tells one story, but what if the real opportunity lies elsewhere? Discover 1,444 companies where insiders are betting big on explosive growth.

Upgrade your decision making: Choose your Baidu story

I mentioned earlier that there is a better way to understand valuation. So let me introduce the narrative. A narrative is simply the story behind the numbers, your perspective on Baidu’s future, adding your own assumptions about revenue, margins, fair value, etc., and combining the company’s strategy, recent news, and your view of its potential.

The narrative connects the dots between what Baidu does and its value, allowing it to bridge real-world developments with the latest financial projections and dynamic fair value. Simply Wall St’s community page makes the narrative accessible and easy to use. There, millions of investors share and refine their investment stories as new data arrives.

This tool allows you to easily compare an individual’s fair value to Baidu’s current price, making it much easier to decide whether to buy, hold, or sell. Plus, the narrative automatically updates as new information comes in, so your perspective stays relevant even as the market moves.

For example, one investor may be optimistic about advances in AI and see Baidu’s fair value closer to $146, while another investor may be more cautious about AI risks and regulation and place Baidu’s fair value closer to $71. Your story makes a difference.

Do you think there’s more to Baidu’s story? Visit our community to see what others are saying.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

Evaluation is complex, but we will simplify it here.

Discover whether Baidu is undervalued or overvalued with our in-depth analysis. Fair value estimates, potential risks, dividends, insider transactions, and financial condition.

Access free analysis

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.