Applied Materials (AMAT) stock gained momentum after UBS raised its outlook, saying DRAM spending is expected to increase due to growth in AI and data centers. With the company’s expanded research and development efforts and advanced chip technology, it is well positioned to meet future demands.

Get our latest analysis for Applied Materials.

Applied Materials has delivered impressive results, buoyed by new highs in demand for AI and semiconductors. The stock’s seven-day return of 12.6% and an impressive 56.9% increase over the past three months indicate growing investor optimism. The total shareholder return of 45.8% over the last year confirms the extensive rewards for long-term holders.

If you’re interested in finding the next standout company in the world of technology and AI, now is the perfect time to explore. See the complete list for free.

But after such impressive performance, is Applied Materials still trading at an attractive valuation, or has the market already priced in the next wave of growth, leaving investors with little upside room?

Most popular story: 4% overrated

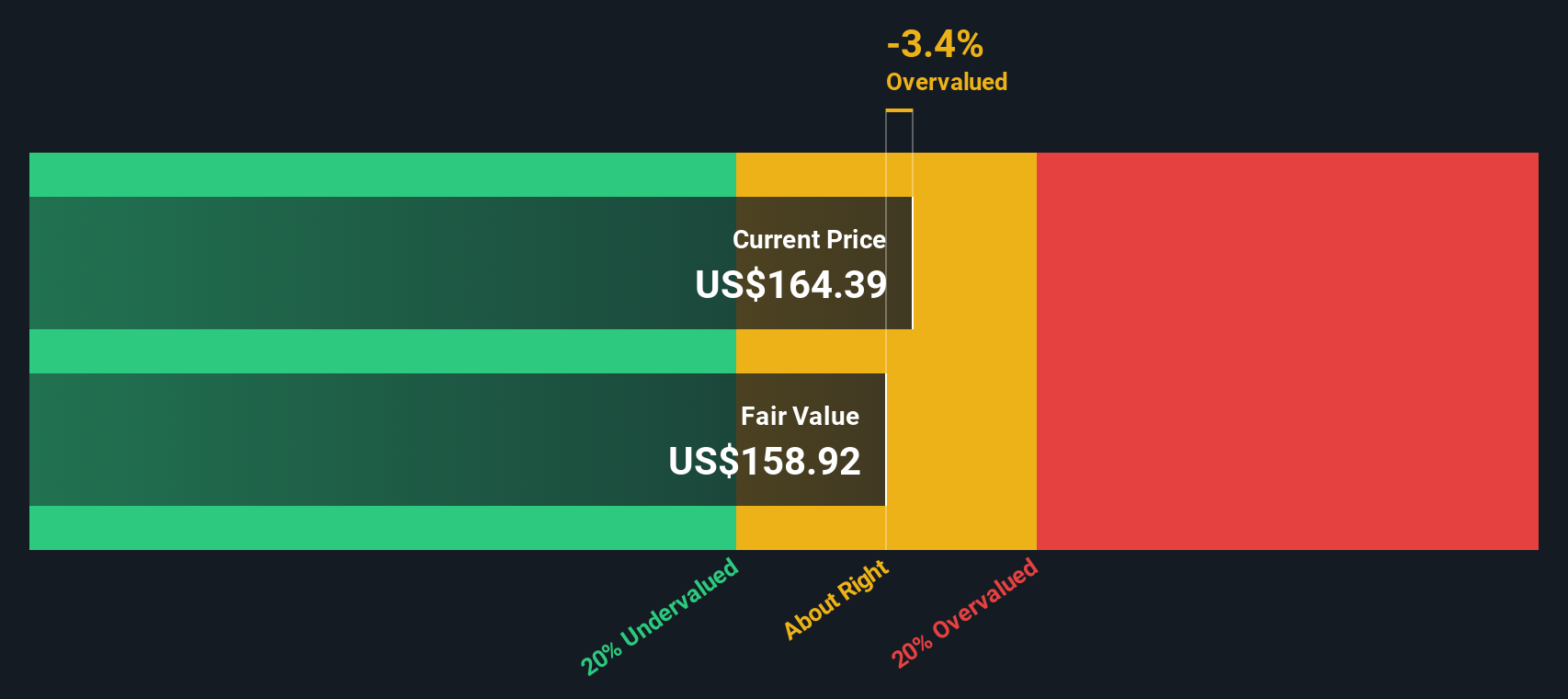

The prevailing theory is that Applied Materials’ fair value is slightly below its current price, at a small but noticeable premium. This prepares us to take a closer look at analyst outlooks and the factors driving future expectations.

The explosion in data creation and rapid adoption of digital transformation (IoT, automotive, industrial automation) continues to accelerate the construction of wafer fabs globally as governments encourage local manufacturing. With Applied’s broad portfolio and investments in local manufacturing infrastructure, including new centers in Arizona and EPIC, we are positioned to capture a larger share of this growing and geographically diversified capital investment and support both revenue growth and margin resilience.

Read the whole story.

Interested in the bold assumptions behind this challenging stock price?The story is filled with forward-looking margins and significant revenue growth. Unraveling the financial logic that can justify or challenge Applied Materials’ premium valuation.

Result: Fair value $241.69 (overvalued)

Read the full explanation to understand what’s behind the predictions.

However, there are also real risks that could rapidly change Applied’s outlook, including increased competition from China and continued geopolitical uncertainty.

Learn about the key risks to this Applied Materials story.

Another perspective: Comparing value to the market

While the narrative-driven model suggests Applied Materials is trading at a premium, our DCF model paints a more bleak picture. We estimate the fair value to be close to $158.08, which is significantly below today’s share price. This calls into question the idea that recent growth and optimism is fully justified by future cash flows. Could risk be trending downwards now?

Find out how the SWS DCF model arrives at fair value.

Build your own applied materials narrative

If you think the stories here don’t quite fit your point of view, or you want to dig into the details and give your own direction, you can easily create your own in just a few minutes. do it your way

A good starting point for any research into Applied Materials is our analysis that highlights 3 key benefits and 1 key warning sign that could influence your investment decision.

Looking for more investment ideas?

Don’t miss your chance. Smart investors have already discovered attractive stocks with serious upside potential. Simply Wall Street’s powerful screener guides your next action.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: Manage all your stock portfolios in one place

What we created is The ultimate portfolio companion For stock investors, And it’s free.

• Connect an unlimited number of portfolios and see the total in one currency

• Alert you to new warning signs and risks via email or mobile phone

• Track the fair value of stocks

Try our demo portfolio for free

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.