Oracle’s stock price has fallen sharply in recent weeks, but it’s still up 71% over the past five years. A key tension for investors is whether the recent decline makes the stock look cheap relative to its fundamentals, or whether the decline is simply catching up with earlier optimism about AI and cloud advancements.

- Oracle has returned 71% over five years, and its long-term story remains intact even after the recent selloff.

- Initiatives in AI infrastructure and large-scale data center projects may support long-term profitability, but large capital investments and execution risks associated with data center expansion and customer concentration may weigh on stock valuation.

- Simply Wall St’s check gives Oracle a 5 out of 6 rating. This suggests that the broad multiples of earnings and cash flow are currently leaning towards being cheap rather than expensive.

The question now is whether its high valuation score and long-term earnings track record are enough to argue that Oracle’s AI-focused repositioning is undervalued following the recent share price decline.

Find out why Oracle’s return last year was -40.3%, lagging behind its competitors.

Is Oracle a bargain in terms of earnings?

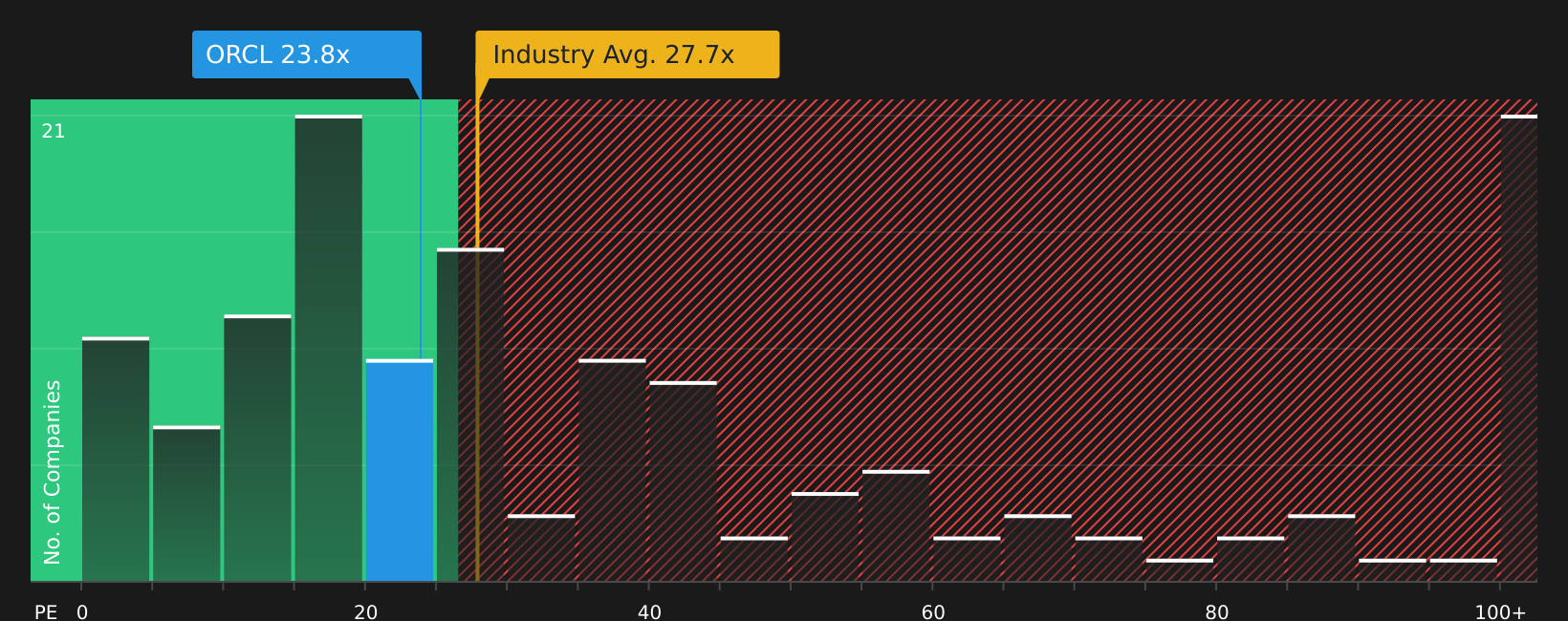

P/E ratio is a useful abbreviation for mature software companies like Oracle, where earnings are a key metric for valuation. Oracle’s P/E ratio of 23.8x is below the software industry average of 27.7x and below the peer average of 40.2x, so the stock is currently priced at a discount compared to many of its large software and AI-focused peers on this simple earnings metric.

Simply Wall Street has a fair P/E ratio for Oracle of 54.5x based on a combination of growth profile, margins, size, and risk factors. This is much higher than the current 23.8 times. This gap indicates that the market is applying a large discount to what this framework suggests could be justified. Despite recent headlines about heavy spending on AI infrastructure, layoffs, and legal scrutiny, earnings multiples remain significantly below both adjusted fair ratios and the broader peer group.

On a P/E basis, Oracle stock currently looks undervalued relative to fair ratios and its broader software competitors.

See what the numbers say about this price. Please check the rating breakdown.

The Oracle Story: What Justifies Today’s Price?

Simply Wall St Narratives for Oracle picks up where the valuation puzzle left off by detailing what path Oracle’s future growth, earnings, and earnings must take for Oracle’s stock to have more meaningful value than it currently has. Because each narrative ties fair value to a specific combination of potential catalysts and risks, we can track which version of Oracle’s story looks closer to reality over time.

The community is divided on Oracle, with one camp seeing the AI enhancements as undervalued and others warning that expectations are already high.

Bullish case: 64% undervalued

“Oracle’s story is one of a rapid and aggressive transition from enterprise powerhouse to AI infrastructure leader, and the OpenAI partnership validates the underlying technology.”

Read the full story of the Bull incident Learn why Oracle is undervalued

Bear case: 17% overvaluation

“Instead of competing for entirely new customers, Oracle can migrate existing customers to its own cloud platform…”

Read the full bear incident Learn why Oracle is overvalued

Think there’s more to Oracle’s story? Visit our community to see what others are saying.

conclusion

We believe Oracle stock is undervalued based on its earnings, with its current P/E ratio well below the adjusted fair value implied by software peers and Simply Wall Street’s framework. This difference reflects investors’ hesitance about high spending on AI and data centers, as well as execution and customer concentration risks, rather than a clear judgment about long-term profitability. The question for you is whether these AI infrastructure investments will ultimately lead to sustained, profitable demand that erases today’s valuation discounts, or whether the market is correctly treating Oracle’s low multiple as a safeguard against those uncertainties.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: AI stock screener and alerts

Our new AI Stock Screener scans the market for opportunities every day.

• Dividend country (yield 3% or more)

• Small-cap stocks that are undervalued due to insider purchases.

• High-growth technology and AI companies

Or build your own metrics from over 50 metrics.

Explore for free now

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.