- Corning (NYSE:GLW) has signed a multi-year agreement with Meta Platforms to supply advanced fiber optics and connectivity products for AI data centers.

- The agreement includes a manufacturing expansion in North Carolina that is expected to create new jobs and increase U.S. manufacturing capacity.

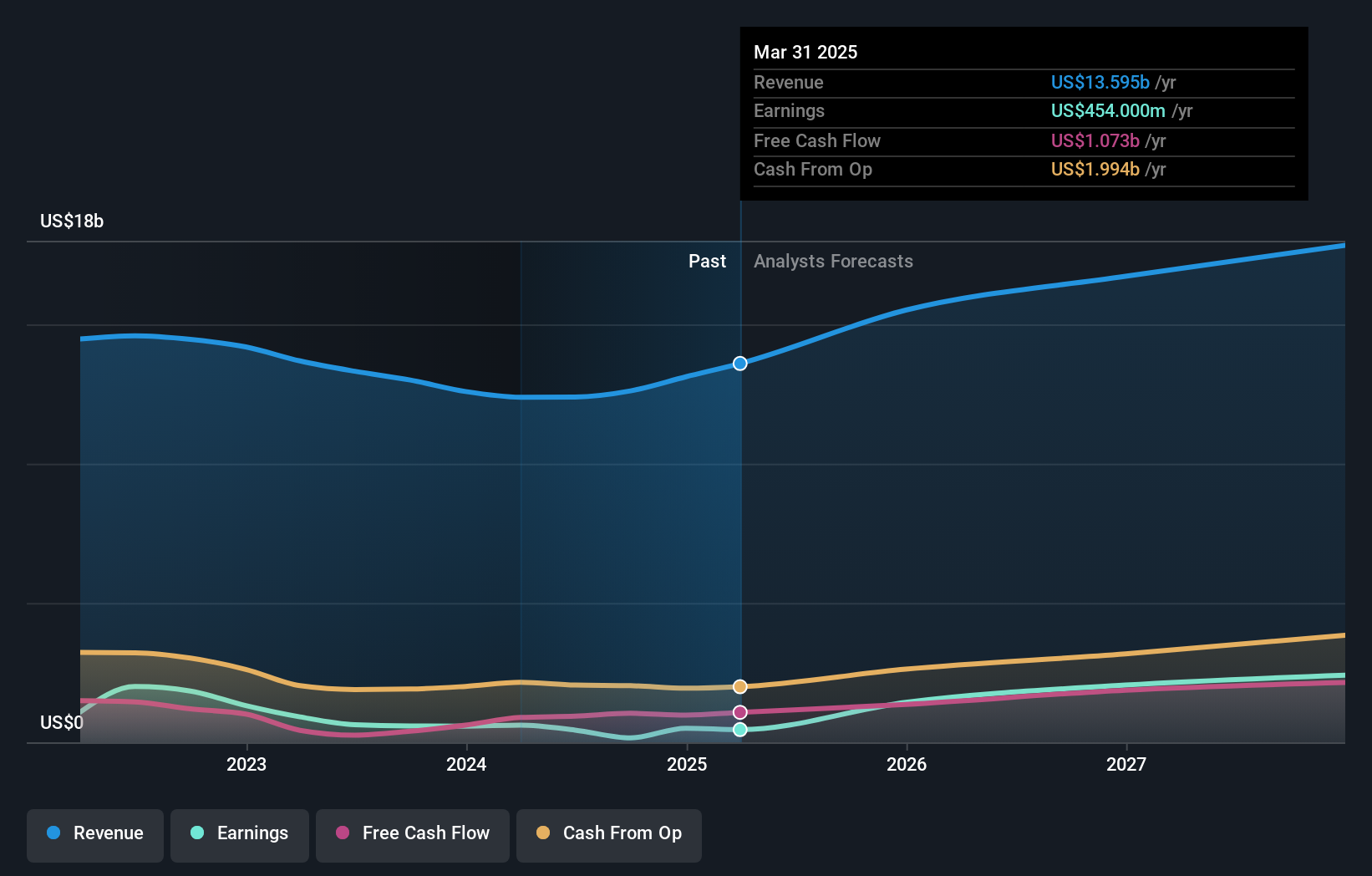

- In connection with this agreement, Corning has updated its long-term sales growth goals through 2028.

For investors looking at NYSE:GLW, this meta-contract provides additional details about Corning’s role in building out AI infrastructure. The stock last closed at $103.25 and has returned 10.7% over the past week, 17.9% over the past month, and 13.9% since the beginning of the year. Based on reference data, the 1-year and 3-year returns are said to be very large.

The new deal shows Corning is tying more of its business to AI data center demand, which could give it clearer visibility into future orders and revenue streams. The latest sales growth targets to 2028 present this as a long-term opportunity. Investors will now be able to track how these commitments relate to North Carolina’s capacity expansion, job additions and reported segment trends in the coming years.

Add to your Watchlist or Portfolio to stay up to date on Corning’s most important news stories. Or explore our community and discover new perspectives on Corning.

How Corning stacks up against its biggest competitors

The meta-agreement provides Corning with greater visibility into optical communications demand, with up to $6 billion in multi-year order commitments tied directly to building AI data centers. For you, as a shareholder, this ties Optical Products’ recent earnings strength to certain hyperscale customers, and helps explain why management felt comfortable upgrading Springboard growth plans and supporting North Carolina’s massive capacity expansion, even as peers like Cisco and Ciena also compete for AI data center spending.

How does this fit into the Corning story?

This deal ties directly into both the more cautious and more optimistic narratives surrounding Corning, as it signals a shift in AI and data center themes from narrative to signed contracts. Bulls focused on long-term light and solar demand get new evidence that large customers are willing to sign multi-year contracts, while more cautious views on execution and capital recovery are likely to focus on whether this US$6 billion commitment and higher growth targets can be met without stretching the balance sheet or overbuilding production capacity.

Main risks and benefits to keep in mind

- The contract size of up to US$6 billion provides greater revenue visibility for Corning’s optical communications business and supports higher incremental revenue targets through 2028.

- North Carolina’s manufacturing expansion and Meta as a major customer could help Corning strengthen its position as a core supplier of large-scale AI data centers, alongside competitors such as Cisco, Ciena, and Broadcom.

- Management highlights a wide range of macro, trade, supply chain and execution risks associated with large-scale manufacturing investments, which could depress returns from the expanded facility if orders are delayed or lower than expected.

- Analysts note that expectations for AI-driven optical communications growth are already reflected in the stock price to some extent, and upside could be limited if contract economics and optical communications margins fall below current expectations.

What to watch next

From here, it makes sense to watch how fast new capacity in North Carolina increases, how much of Springboard’s sales growth comes from Meta and other hyperscalers, and whether optical fiber margins continue in line with recent company guidance. To learn how different investors are connecting this meta contract to the long-term growth and valuation discussion, check out the community stories on Corning’s dedicated page.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: AI stock screener and alerts

Our new AI Stock Screener scans the market daily to discover opportunities.

• Dividend powerhouse (yield 3% or more)

• Small-cap stocks that are undervalued due to insider purchases.

• High-growth technology and AI companies

Or build your own metrics from over 50 metrics.

Explore for free now

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.