- TSMC (NYSE:TSM) reported strong quarterly results, highlighting the company’s central role in supplying advanced chips for AI applications.

- The company plans to significantly increase its capital spending in 2026 to expand the capabilities of its AI accelerators and cutting-edge process nodes.

- Management is trying to link the past multi-year capex supercycle to a surge in global demand for AI infrastructure and related computing.

- TSMC is pursuing market share gains and pricing power in advanced nodes as part of its response to building AI.

TSMC is at the core of the global semiconductor supply chain, manufacturing high-performance chips for leading AI and cloud companies. The latest spending plans show that AI-focused products are becoming an even bigger part of the company’s mix, alongside traditional smartphones, PCs and data center chips. As an investor, we highlight how our chip manufacturing capabilities are aligned with building AI infrastructure around the world.

Going forward, the company’s increased capital spending, pricing approach, and focus on advanced process technologies are likely to impact how value is shared across AI hardware, from chip designers to system integrators. These moves may also shape expectations and plans for key ecosystem partners that rely on TSMC’s cutting-edge manufacturing.

Add it to your Watchlist or Portfolio to stay up to date with the most important news stories about Taiwan Semiconductor Manufacturing. Or explore our community and discover new perspectives on Taiwanese semiconductor manufacturing.

Why Taiwan Semiconductor Manufacturing has great value

What matters to us as an investor is how closely TSMC ties its multi-year capex supercycle to AI-specific demand. Management plans to spend $52 billion to $56 billion in 2026, after a budget of $41 billion in 2025, to support the advanced nodes and packaging that will be central to the AI accelerator. This strengthens TSMC’s role as a key supplier to companies such as Nvidia, Broadcom and major cloud providers.

The story of Taiwanese semiconductor manufacturing and why this AI supercycle matters

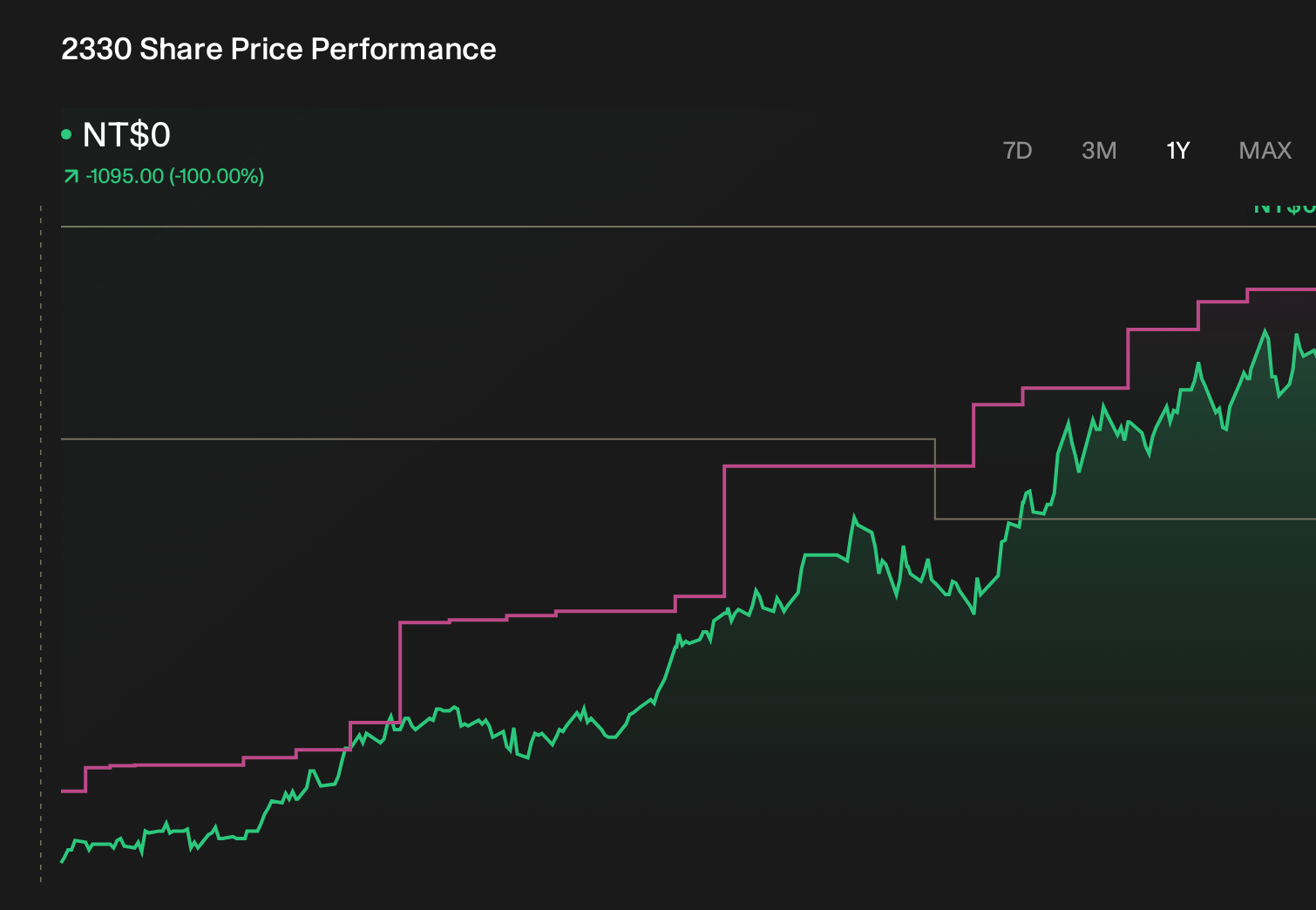

Recent commentary suggests that TSMC will set the tone for AI investments in 2026, with several investors and commentators pointing to strong fourth-quarter 2025 results, seven consecutive quarters of double-digit growth, and management signaling near 30% revenue growth in 2026 as part of what some see as a multi-year megatrend in AI infrastructure.

TSMC balances profits and risks

- 🎁 TSMC is said to have a near-monopoly in advanced AI chip manufacturing, taking full advantage of its advanced nodes and strong pricing power, including a multi-year price increase plan.

- 🎁 Analyst-focused compensation includes past year earnings growth of 48.3%, annual revenue forecast of 16.84%, and a P/E of 26.7x, compared to the industry average of 40.8x.

- 🎁 Several summaries highlight that TSMC is trading at what is considered good value relative to its peers, with its AI data center exposure and capital spending plans tied directly to customer demand signals.

- ⚠️ On the risk side, Simply Wall Street data points to high levels of non-cash income as a key risk, which can make interpretation of headline profitability difficult.

What to watch next

Looking ahead, it’s worth watching whether TSMC’s planned capital expenditures, pricing changes, and geographic expansion, including an expansion in Arizona, continue to closely align with its actual AI infrastructure orders, and how that translates into earnings and cash generation in the coming years. Stay on top of evolving views by following the community’s stories in this dedicated section.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

Evaluation is complex, but we will simplify it here.

Discover whether Taiwan Semiconductor Manufacturing is undervalued or overvalued with our in-depth analysis. Fair value estimates, potential risks, dividends, insider transactions, and financial condition.

Access free analysis

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.