Customers flock to the company, train AI models and run inference applications in the cloud.

Amazon At the time of writing, it is the fifth largest company in the world. This ranking was achieved thanks to its dominant position in the e-commerce market. He is also the largest player in the cloud computing market, but he has earned a large portion of his revenue from his e-commerce business.

The company manages an estimated 38% share of the US e-commerce market. Additionally, it has achieved solid positions in other major markets, including Europe and India. Amazon's e-commerce marketplace is used by millions of sellers to sell items thanks to solid presence around the world.

Companies looking to train and deploy artificial intelligence (AI) applications in a similar way: Oracle (orcl -3.77%)). It's no surprise that its cloud infrastructure platform is in high demand and will become Amazon in the AI infrastructure market in the long term. Let's see why it may be.

Image Source: Getty Images

Oracle is becoming an option for AI companies

Just as Amazon offers a platform to sell products to sellers, Oracle gives customers access to cloud infrastructure for AI model training and inference applications. Its customers have a wide range of chips, including both graphics cards and server processors. nvidia and Advanced Micro Devices.

Customers can rent Oracle's cloud infrastructure, run generated AI models, and build agent AI applications, among other things. The company offers many AI services to enable developers to apply AI to applications and business operations. Clients can customize pre-built AI models to suit their needs. This means you have the flexibility to increase or decrease Oracle's infrastructure usage based on your needs.

Furthermore, Oracle claims that compared to its competitors it can provide significant cost savings while running AI workloads on its infrastructure. All this explains why the company's cloud infrastructure demand is passing through the roof.

Oracle's remaining performance obligations (RPOs) refer to the total amount of contracts that are not met at the end of the term, reaching $138 billion (ends May 31) at the end of the fourth quarter of fiscal year 2025. The metric jumped an impressive 41% year-on-year in the last quarter.

Better yet, Oracle is hoping to more than double the RPO this fiscal year as it focuses on rapidly expanding data center regions around the world. Chairman Larry Ellison said in response to the company's June revenue press release that the company “has 23 multi-cloud data centres, with an additional 47 people being built over the next 12 months.”

The company has 29 dedicated Oracle Cloud Customer data centers, with 30 more being built in 2026. This rapid data center to meet the incredible market demand for training in the cloud and running AI applications explains why we are hoping for faster consumption of cloud infrastructure services this year.

Furthermore, the significant improvements Oracle forecasts in this year's revenue pipeline show that it is on track to bring about solid growth over the years. The focus is on expanding the company's infrastructure, which allows it to drive a larger share of the Services as a Cloud Infrastructure Services (IAAS) market.

The good thing is that Oracle's predicted jump in RPO suggests that it is already growing at a faster pace than the cloud IAAS market. So, thanks to increasing dominance in this sector, Oracle could become Amazon in the AI infrastructure market in the long term. That's exactly why investors can do well to buy stocks before they spike even further.

Investors can still buy this AI stock with a reasonable valuation

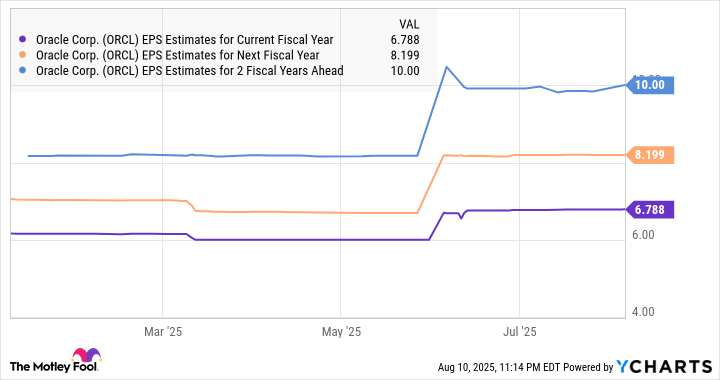

Oracle Stock has scored an impressive 50% so far in 2025. As a result, it is currently trading at an expensive 58x revenue. However, analysts hope that future final growth will be significantly accelerated following an estimated 12% increase this fiscal year.

Share-share-share estimates for current fiscal year data by YCHARTS.

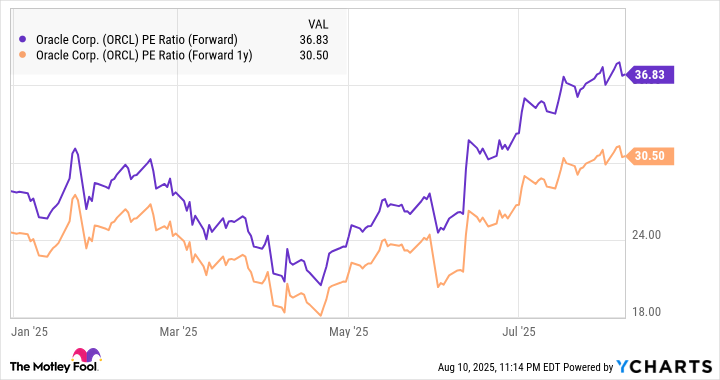

As a result, Oracle's forward multiples are significantly lower than the subsequent price and rate of return.

ORCL price return (forward) data from YCHARTS

Furthermore, Oracle's growth could effectively surpass estimates thanks to healthy demand for Cloud AI infrastructure. This allows you to build a huge revenue pipeline. Potential outperformance can pave the way for a significant long-term benefit of a stock, so buying it looks like something to do right now.

The harsh Chauhan has no position in any of the stock mentioned. Motley Fools introduces and recommends Advanced Micro Devices, Amazon, Nvidia, and Oracle. Motley Fools have a disclosure policy.