Industry Voices are editorials by industry experts and analysts commissioned by Fierce staff and do not necessarily represent the views of Fierce.

Open RAN is gaining momentum as major network operators like AT&T, DoCoMo, and Vodafone make their plans more real, more immediate, and more concrete.

But a word of warning to our friends in open RAN: What will happen when the top network vendors build AI enhancements into RAN?

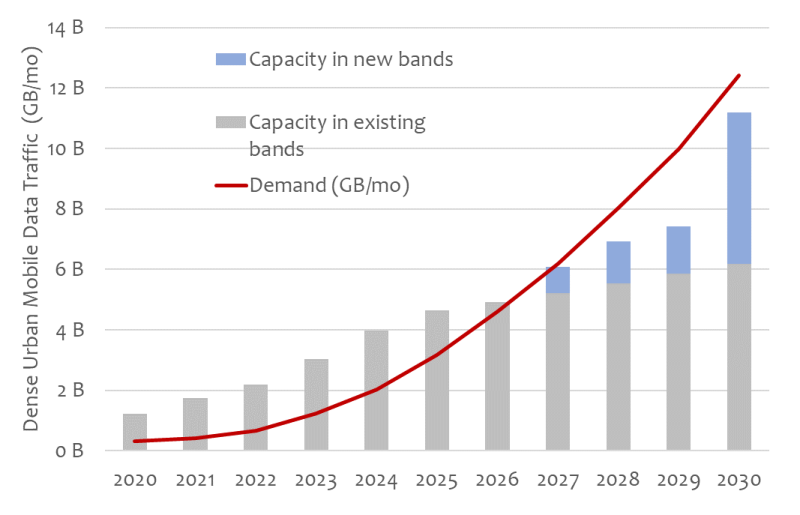

I just finished a six-month project that culminated in a report on the impact of AI on RAN capacity. Capacity is a key topic for our customers right now. Mobile operators are predicting a “capacity gap” from 2027 to 2029, where demand in dense urban hotspots will exceed capacity. Applying AI/ML techniques to the RAN can help close that gap with a 20-30% improvement (see the report for more details on uplink and downlink improvements).

The chart above shows capacity and demand for the busiest 10% of cell sites in major US networks. The remaining 90% of sites will not experience the same “capacity gap,” but dense urban centers are expected to experience capacity shortages in 2028 and 2029. The grey bars show capacity in existing bands, while the blue bars show new DoD bands and expected 6G bands. Even with minor spectrum sharing limitations, there is a problem here. AI/ML can fill this gap across a large number of sites.

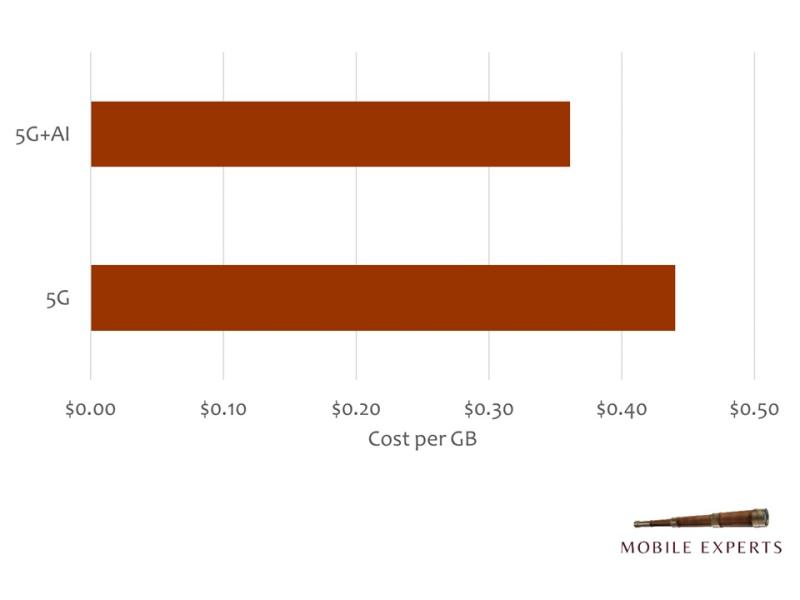

AI will be one of the best investments mobile operators will ever make. A software upgrade will reduce total cost of ownership by $0.08/GB and prevent a surge in churn due to capacity shortages. The cost is minimal, just a few more processor cores and a couple of GPUs.

AI is not magic – it won't extend Shannon's Law as advertised – but it will improve the average performance for the average user, and that's the key outcome for operators.

data form

Here are some issues between AI and Open RAN: AI/ML models rely on hard data to refine and improve themselves. If Vendor A built and trained an AI model using their own radio hardware, the real-time data in the AI/ML training set will be formatted in a very specific way. It might use I/Q samples, RF power measurements, or temperature sensors in the RU to make a particular decision. Substitute with Vendor B's radio and all the data will be in a different format. Will the model be able to retrain itself with a different data format? We don't know yet.

The O-RAN Alliance is addressing this issue. There is a study item in the O-RAN Alliance Working Group 2 looking at alternatives, and some vendors have proposed a good framework for sharing standardized data between RICs and SMOs, such as RSRQ data and RB allocations. However, this is not as rich or real-time as individual RF measurements directly from each antenna element, and the O-RAN spec has not been updated since 2021. So the O-RAN approach offers some benefits, but not all.

Will Ericsson or Nokia step up to close the performance gap? Each will leverage their AI/ML models as a means of differentiation to provide the best possible performance for their hardware. If a major vendor can deliver 20% higher capacity performance with their radios, it will encourage operators to use their incumbent vendor in urban areas where capacity is most important.

In rural and suburban areas, AI/ML models prioritize energy efficiency over capacity. In these cases, a combination of Open RAN vendors may work well: actions are taken at a slower pace (non-real-time) and decisions to turn off radio channels or hardware are based primarily on traffic data rather than real-time RF measurements.

We live in interesting times. We have multiple technology disruptions happening at the same time. In this case, we have two technology disruptions that can disrupt each other. Be careful not to get caught off guard.

Joe Madden is a Principal Analyst at Mobile Experts, a network of market and technology experts analyzing the wireless market.