Shatifong Chandaeng

prologue

Shutterstock (New York Stock Exchange: SSTK) has fallen by up to 25% over the past month, despite its recent strong performance and strong balance sheet. The company has a D/E ratio of 0.07 and an EPS CAGR of 34% over the past five years.The company is betting forward We offer revamped business models and generative AI services to drive future growth. My valuation model targets a fair value of ~$87.01.

Transition to a subscription-based model

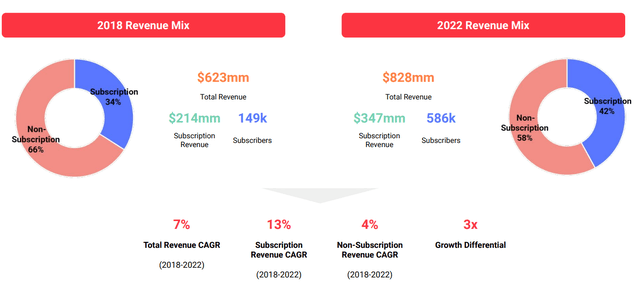

SSTK continues to move to a subscription-based business model that helps modernize the business and reduce transaction friction. Previously, customers only had the option to download and pay for each piece of content individually. This was not an ideal business model for someone actively searching for multiple pieces of content during the creative process. You have to pay for each piece of content separately, breaking your creative flow and creating unnecessary additions. It creates friction in the creative process. The advantage of the subscription model is that each user is assigned a fixed number of credits for licensing content.most of the time Recent investor presentations, subscription-based revenue now accounts for 42% of revenue mix, up from 34% in 2018. Overall, SSTK’s business model transition continues to be successful and will be key to its future performance.

Investor Day 2023

OpenAI Partnership

SSTK has a strategic partnership with OpenAI as of October 2022. This will allow OpenAI’s tools to be integrated within his SSTK to generate his AI content on the platform through keywords entered by the customer. This partnership has so far been very effective in increasing SSTK subscriptions and increasing content on the platform.

In January, we last reported that users had created 3 million assets in the first two weeks after launch.

While the platform’s revenue potential is not yet clear, the partnership will undoubtedly benefit SSTK from a marketing perspective as it capitalizes on the curiosity surrounding AI at this time. If SSTK can convert a certain percentage of all new users who sign up for its platform into customers for its other products, this partnership will not only bring short-term benefits to the business, but will also allow integration with AI. will also bring long-term benefits from

2022 10k

3D platforms and generative AI

SSTK also partners with NVIDIA (NVDA) to develop generative 3D products. Generative AI is still in its early stages, but we believe there will be many monetizable use cases in the future. Something as simple as avatar generation has already proven successful with the Lensa app. The app exploded in his late 2022 boom, generating over $30 million in revenue for him in a single month. His 3D partnership with SSTK positions the company as an early player in the space and gives it a favorable footing as it continues to add content to its catalog.

2023 Investor Presentation

Consensus forecasts and revenue growth

stock analysis.com

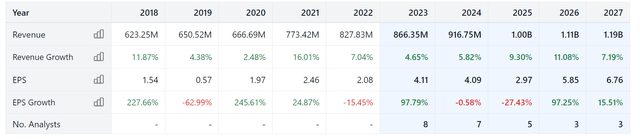

EPS is expected to grow from $2.08 in 2022 to $6.76 in 2027, a CAGR of 26.55%.

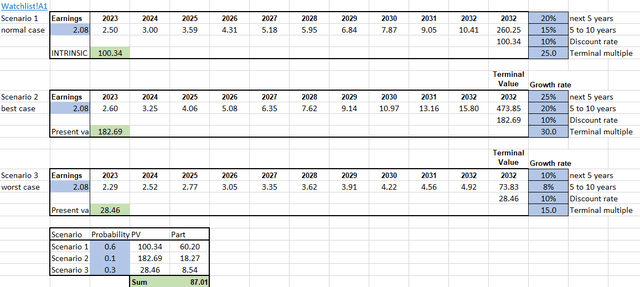

In the next section, we select growth rates for scenario analysis and evaluation. My best case scenario assumes his highest growth rate of 25% for his first five years. Also notice that the value calculation for this scenario only gave a probability of 10%.

To be conservative, we choose a growth rate slightly below the consensus in the normal case, and a growth rate significantly below it in the worst case. The worst case is assigned a probability of 30% and given more weight than the best case in calculating the overall value.

Let’s move on to calculating the value in the next section.

Evaluation and scenario analysis

Author’s representative

All value calculations use a 10% discount rate. 10% is my minimum required return. Because historically, this is the return you can expect if you decide to invest in an index fund that tracks the S&P 500. Finally, keeping the discount rate the same allows for comparisons between different investments.

It also assigns a weight of 0.6 to the base case, 0.1 to the best case, and 0.3 to the worst case. That aside, let’s move on to individual scenarios.

Scenario 1 is my base case, assuming 20% growth over the next 5 years, 15% growth in years 5-10, and a final multiple of 25x. Discounting the 2032 selling price to present value gives a fair value of $100.34 for an investor with a 10% target rate of return.

Scenario 2 is my best case, assuming 25% growth over the next 5 years, 20% growth in years 5-10, and a final multiple of 30x. Discounting the 2032 selling price to present value gives a fair value of $182.69 for an investor with a 10% target rate of return.

Scenario 3 is my worst case, assuming 10% growth over the next 5 years, 8% growth in years 5-10, and a final multiple of 15x. Discounting the 2032 selling price to present value gives a fair value of $28.46 for an investor with a 10% target rate of return.

The total weighted PV is $87.01, representing an increase of about 66% from the current level.

risk

Inability to monetize AI content

Growth may be slower than expected if SSTK does not find a way to monetize its AI content.

Oversaturation of AI content

AI art content is everywhere today, but it could become saturated in the future. Producing the highest quality content is key for SSTK to become a go-to provider.

speculative investment

This is a speculative investment. Because it is based primarily on future growth driven by new and unproven products and services.

Conclusion

Overall, I rate SSTK as a speculative buy due to the fact that it is betting on the future of 3D and generative AI. Whether or not these bets pay off remains to be seen, but based on my scenario analysis, the risk reward is compelling.