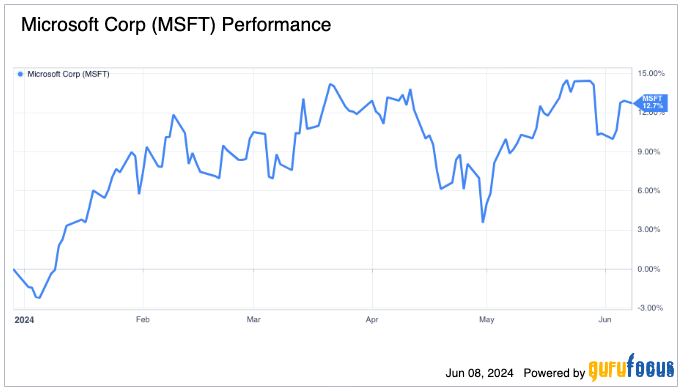

Microsoft Corporation (NASDAQ:MSFT) is the largest publicly traded company in the world, with a market capitalization of approximately $3 trillion. Following its acquisition of OpenAI, the software giant has aggressively expanded its customer base and significantly improved its overall performance. The company's stock price has soared in recent quarters, beating expectations and delivering strong profits. We expect this trend to continue as Microsoft continues to lead the way in artificial intelligence and invests heavily in new AI initiatives, building on the success it has achieved with OpenAI.

Figure 1: Microsoft Stock Has Been Soaring Since the Second Half of 2023

Source: GuruFocus

Microsoft has strategically positioned itself above its competitors through huge R&D expenditures, major acquisitions, and strategic alliances with external companies. These strategies have given the company a competitive advantage, allowing it to outperform its competitors and deploy AI services to end users faster and more effectively. The intensifying competition between Google's (NASDAQ:GOOGL) latest release Gemini and OpenAI's flagship product GPT-4 highlights the evolution of generative AI. With the emergence of multimodal interactive platforms, it is clear that a three-way race is underway in the generative AI space. Microsoft will likely benefit temporarily from its early investment in OpenAI to solidify its position as a leader in the space.

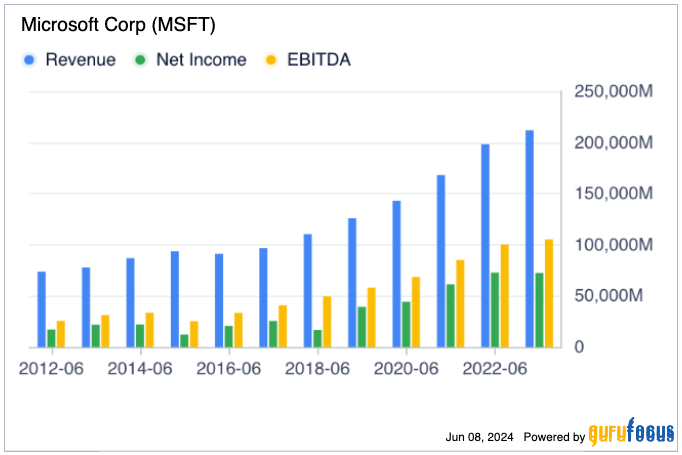

Microsoft has been aggressively introducing AI service capabilities into its Azure cloud computing platform. Azure has become one of the company's largest sources of revenue, even surpassing its Office software suite. The release of Azure in 2010 marked a pivotal change in the company's revenue trajectory. Seven years after its release, revenue grew significantly, driven primarily by the success of Azure. This trend continues today, with Microsoft's cloud computing services contributing significantly to the company's financial growth.

Figure 2: Azure is the driving force behind Microsoft's revenue growth

Source: GuruFocus

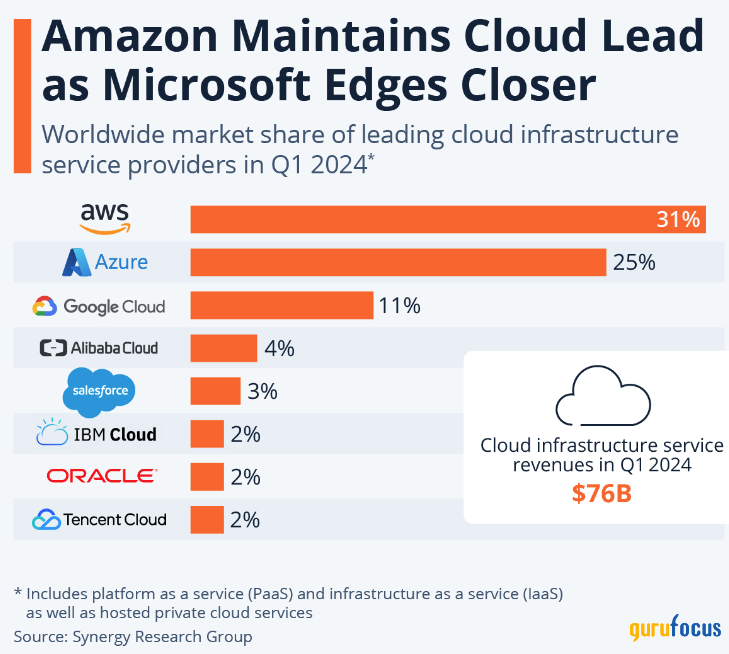

Azure is a significant contributor to Microsoft's revenues, so it's important for the company to continue to acquire new customers if it is to maintain its expected growth. Microsoft is well positioned to achieve this, as evidenced by Azure's 25% capture of the cloud market, despite Amazon's (NASDAQ:AMZN) AWS losing market share slightly. The ongoing cloud super cycle and generative AI boom are key drivers of Azure's market share growth, which now stands at 25%, gradually closing the gap with AWS at 31%.

Figure 3: Azure is closing in on market leader AWS

Source: Statista

As demand for cloud services and AI capabilities grows, Microsoft is poised to continue to exceed market expectations. Azure's strong performance and strategic advancements ensure it remains a key component to the company's overall success and strengthen its leadership in the rapidly evolving cloud and AI industries.

Microsoft made headlines when it took a large stake in OpenAI in 2019, investing an initial $1 billion. Since then, the company has invested another $10 billion in the partnership. Aside from this major investment, the company has made several other notable investments in cloud computing and AI in recent months.

In the past two months alone, Microsoft has announced a series of strategic investments, including a $2.9 billion investment in Japan to open a research center in Tokyo, $1.5 billion in the United Arab Emirates for equity and infrastructure in AI company G42, and $3.3 billion in Wisconsin to build a manufacturing-focused AI research lab. More recently, the company announced it would invest $3.2 billion over two years to expand its cloud and artificial intelligence infrastructure in Sweden. Additionally, Microsoft's venture capital fund, M12, has invested in several private AI companies. One of the most notable moves was a $650 million investment in Inflection AI, co-founded by Mustafa Suleyman and LinkedIn co-founder Reid Hoffman. Suleyman, a prominent figure in the AI field, is now head of Microsoft's AI division.

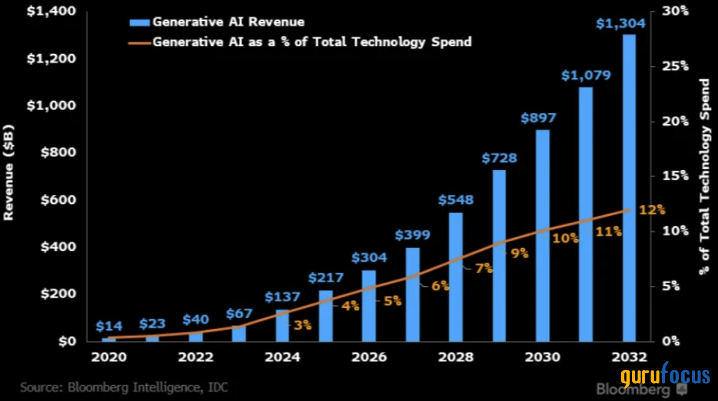

Figure 4: Generative AI will be a $1.3 trillion market by 2032 (Bloomberg Research)

Source: Bloomberg

With the generative AI market expected to exceed $1 trillion within the next decade and global IT spending projected to grow 8% this year, Microsoft is well positioned to significantly expand its business. These strategic investments provide the company with a number of catalysts to accelerate growth and solidify its leadership in the AI industry in the near future.

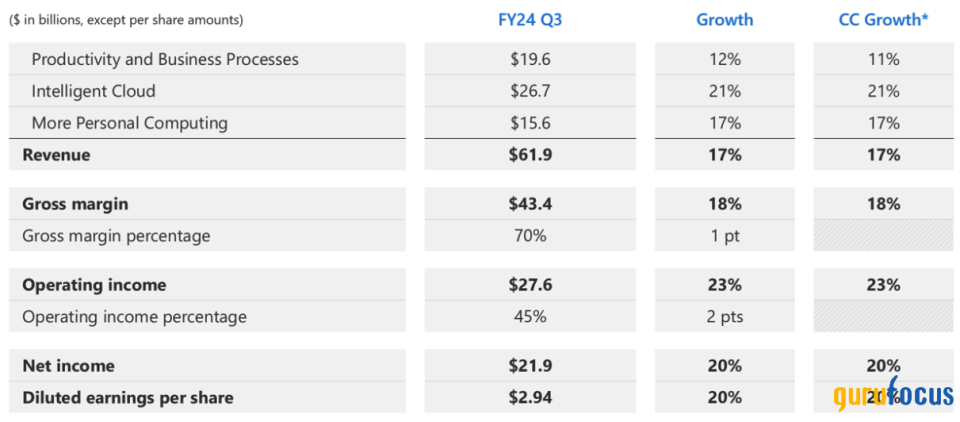

In its third quarter 2024 earnings report released last month, Microsoft reported that revenue grew 17.1% year over year to $61.9 billion. The company's GAAP earnings per share were $2.94. Operating margins expanded significantly from 42.30% to 44.60%, representing a significant improvement for a company of its size. This growth was achieved despite charges related to the Activision acquisition and accounting changes related to the useful life and depreciation of certain data center equipment. Both revenue and earnings results beat expectations.

Figure 5: Third quarter revenue summary

Source: Microsoft Investor Relations

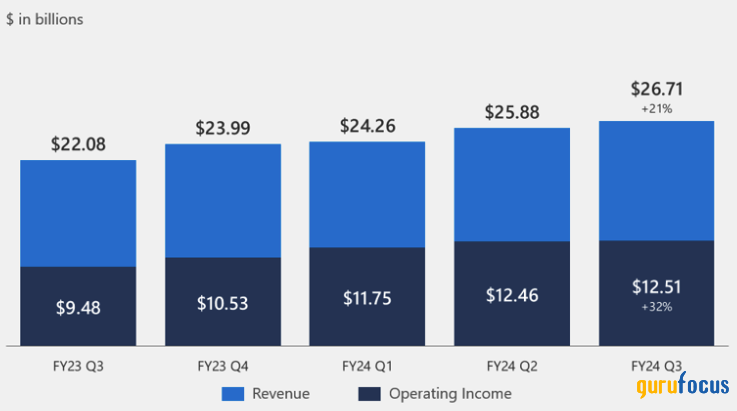

The performance was primarily driven by accelerated growth in Microsoft's largest and fastest-growing business, the Intelligent Cloud division, which saw revenue grow 21% year over year to $26.7 billion and operating margin expand to 46.80% (up 4 percentage points). In addition, search and news advertising revenue increased 3.30% year over year to $3.13 billion, supported by market share growth for OpenAI-powered Bing, which reached 3.64% of the search engine market as of April 2024. As a result of these strong results, Microsoft's quarterly leveraged free cash flow increased from $13.5 billion to $16.9 billion, despite an increase in capital expenditures of $4.3 billion.

Figure 6: Trends in sales and operating profits in the Intelligent Cloud division

Source: Microsoft Investor Relations

Revenue growth is crucial to Microsoft's future success, especially as costs continue to rise to train new AI models and improve Azure, the company's primary AI delivery method. The company has demonstrated solid growth over the past few years, posting mid-teen growth rates in 2020, 2021, and 2022. Looking ahead to Q4 2024, Microsoft is expected to continue to outperform expectations with expected revenue of $64.4 billion, growing 14.60% year over year. Adjusted earnings per share are expected to increase from $2.69 to $2.93, reflecting improved operating leverage. A big driver of this growth is Copilot, the flagship AI product that has helped drive subscription growth and revenue generation. As Copilot gains traction, Microsoft is announcing new features for its AI assistant that could create new recurring revenue streams. Moreover, the integration of GPT-4o into Bing is expected to attract more users and increase Microsoft's share of the search market. Bing recently captured over 10% of the search market, suggesting that Google's monopoly is under threat.

Management guidance states that full-year operating margins are expected to increase by more than two percentage points despite investments in cloud and AI, the impact of the Activision acquisition, and changes to useful life accounting. This margin expansion highlights Microsoft's efficiency and disciplined cost management, and is expected to drive continued growth in investments in cloud and AI, both of which are higher-margin revenue streams, next year. These factors are expected to support the same margin improvement trajectory through 2025.

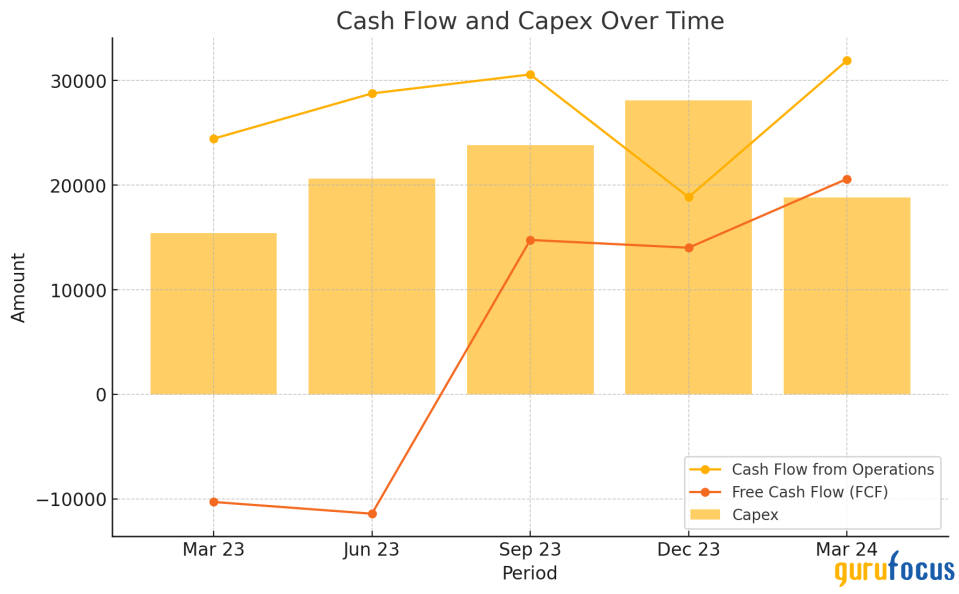

Beyond the impressive revenue and margin numbers, Microsoft's free cash flow is a notable financial strength. The company is cash-rich, with $80 billion in cash to support its acquisition and talent-hiring strategy. Free cash flow generation reached $70.57 billion in the last 12 months (up 22.90% quarter-over-quarter), enabling aggressive partnering and M&A activity, including the recent acquisition of Activision Blizzard for $69 billion. After declining last year, the company is on track to exceed and increase free cash flow this year, providing ample resources for future acquisitions. The gap between operating cash flow and free cash flow has widened as management has invested heavily in cloud and AI infrastructure, which could lead to much faster FCF growth in the mid-to-long term once the infrastructure buildout is complete.

Figure 7: Trends in CFO, FCF, and capital expenditures

Source: Microsoft Investor Relations

Microsoft has committed significant resources to R&D and capital expenditures, with R&D expenses of $28.19 billion, up 3.20% sequentially, and capital expenditures of $39.54 billion, up 51.9% sequentially, during the last 12 months. These investments ensure that Microsoft has ample capital to pursue growth opportunities. Management's commitment to maintaining momentum in the cloud and AI businesses is evidenced by the rapid increase in investments in these areas.

As of the end of the third quarter, Microsoft had $80 billion in cash and short-term investments and $65.44 billion in long-term debt. The company's debt-to-EBITDA ratio of 0.60 indicates a strong financial position and ability to repay long-term debt efficiently.

Evaluation Considerations

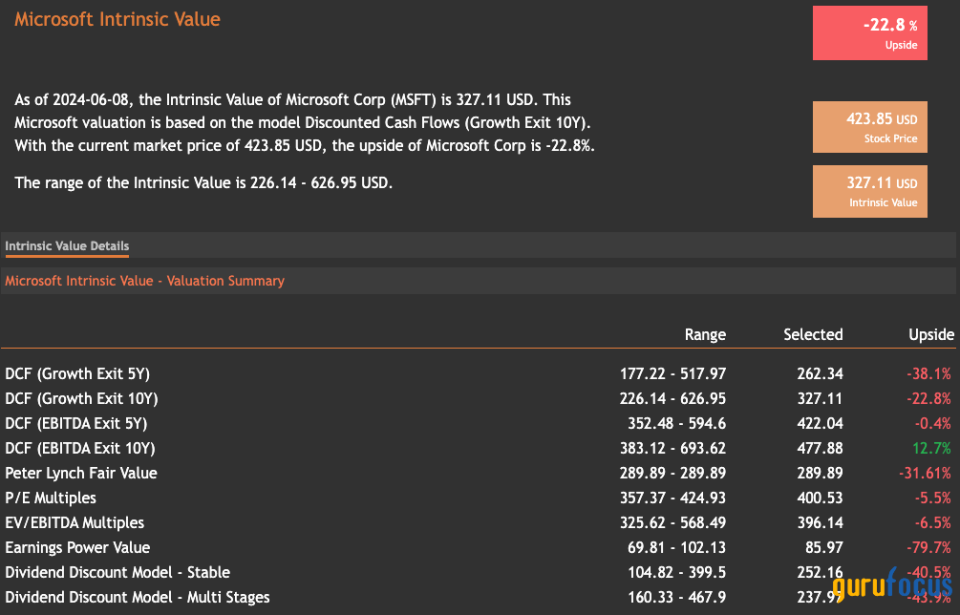

While Microsoft has significant upside potential if its generative AI goals proceed as planned, it is not the most affordable stock to buy at the moment, although it is a wise long-term investment. It is important to keep in mind that long-term investments often take a significant amount of time to pay off. While there are many growth factors in Microsoft's favor, the current stock price does not offer much of a margin of safety to justify a bullish valuation at this time. While Microsoft's business is exceptionally strong and will likely continue to thrive, we question whether it is wise to buy the stock at current levels. According to various valuation methodologies, none offer a sufficient margin to justify a purchase at the current price. Even with aggressive estimates for Microsoft's growth, profit margins, and free cash flow generation, it is difficult to justify a long position based on fundamentals alone.

Figure 8: Microsoft’s Current Valuation Doesn’t Offer Enough Upside.

Source: valueinvesting.io

Additionally, Microsoft may face more intense competition in its AI business, both from larger companies in the Magnificent Seven and from smaller startups. While the technology company is considered a leader in AI today, that may not be the case five or ten years from now. Additionally, economic uncertainty continues, with inflation remaining high and the possibility that the Federal Reserve could still raise interest rates. Microsoft's heavy investments in building out its cloud platform and AI tools could be viewed unfavorably by investors if the economy worsens.

Considering these factors, I do not give a buy recommendation to Microsoft shares at the current price. Therefore, I recommend holding the stock and will closely monitor the price movement. If there is any negative movement while the current fundamentals hold, my recommendation may change to buy at a lower price.

Conclusion

Microsoft's impressive financial performance, strategic investments in AI and cloud computing, and robust growth prospects underscore the company's potential for long-term success. However, given current valuations and economic uncertainty, the stock currently lacks a sufficient margin of safety to justify a bullish rating.

This article was originally published on GuruFocus.