One of the most anticipated events of the year has officially come to an end. Less than 24 hours after the close of trading on Friday, June 7, the foundation of the artificial intelligence (AI) revolution was announced. NVIDIA (NASDAQ: NVDA)completed a 10-1 forward split.

A “stock split” is an event that allows a publicly traded company to superficially change its stock price and the number of shares outstanding by the same amount. Stock splits are superficial in the sense that they have no effect on the company's market capitalization or financial performance. Stock splits make shares nominally more affordable to retail investors (as in a forward stock split). Stock splits also increase a company's stock price and help it remain listed on a major stock exchange (as in a reverse stock split).

Over the past three years, investors have gravitated toward stocks that split because of a history of them outperforming others. Since mid-2021, more than a dozen high-flying stocks have announced or completed stock splits, including Nvidia, which just completed its second split since July 2021.

Nvidia's market cap has increased by $2.68 trillion in just over 17 months

On paper, Nvidia is giving investors a reason to invest and have fun. On June 5, Nvidia's market cap surpassed $3 trillion for the first time, and the company apple It ranks second among the largest publicly traded companies in the United States. Since the start of 2023, NVIDIA's market capitalization has increased by approximately $2.68 trillion, all of which is driven by AI.

Nvidia's AI-inspired graphic processing units (GPUs) are the foundation of high-computing data centers. By various estimates, Nvidia's chips account for around 90% of the AI-GPU market share, with its hugely popular H100 GPUs powering generative AI solutions and helping train large-scale language models.

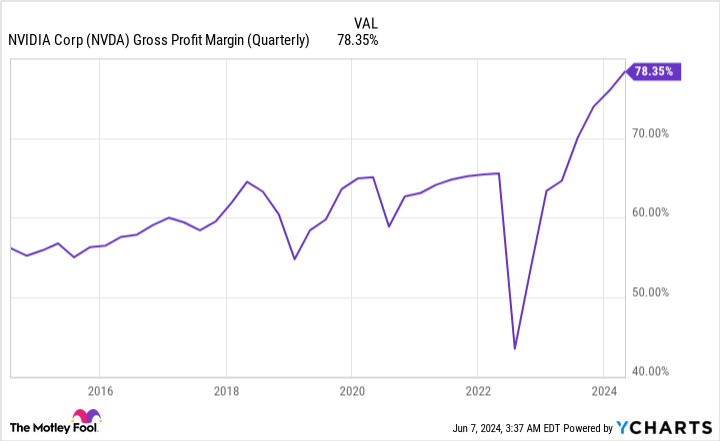

Nvidia's innovative advantage is also driving profits: The company's next-generation Blackwell chips, which sell for $30,000 to $40,000, are expected to sell out well into 2025 by Wall Street analysts. With demand overwhelming supply, Nvidia had no trouble raising prices for its AI-GPUs, reaping the benefits with a big jump in gross margins to 78.35% in the first quarter of fiscal 2025, which ended April 28.

Nvidia shares have risen 738% in just over 17 months, but they still look fairly cheap on a fundamental basis: The stock currently trades for roughly 34 times expected one-year earnings, but the Wall Street consensus is for 46.5% annualized earnings growth over the next five years.

On the surface, Nvidia looks perfect after its 10-for-1 stock split, but as an investor, I can't judge things by appearances.

History suggests Nvidia may be a ticking time bomb

Taking a step back, broadening the perspective, and using history as a guide will completely change how you view investing in Nvidia over the coming months and years. While there's no denying that the company has been going strong, handily beating even the loftiest expectations cast by Wall Street analysts, there are a few reasons why you shouldn't even touch Nvidia stock with a 10-foot pole following its 10-for-1 stock split.

The main reason I don't want to get involved with Nvidia has to do with their history of big next-gen innovations.

Since the advent of the internet nearly 30 years ago, Wall Street has hatched many of the next trends expected to change the trajectory of corporate America: innovations such as genome sequencing, the rise of nanotechnology, business-to-business commerce, 3D printing, blockchain technology, the metaverse, and now artificial intelligence.

While some of these trends have been successful in the long term, they all have one thing in common (except AI): an early stage bubble burst event. Investors have consistently overestimated the introduction of new technologies and innovations for over 30 years. Game-changing innovations come with high expectations and analysts' high hopes. Unfortunately, new innovations need time to mature, and artificial intelligence will be no exception. When the AI bubble bursts, no company will be hit harder than Nvidia.

It's unclear when the AI bubble will burst. History shows that stock prices can continue to rise for years before correcting. Finally (Keyword!), we have witnessed every new innovation weather a bubble-busting event.

We are also starting to see subtle “warnings” from Nvidia that they are nearing or nearing a peak.

If you dig into NVIDIA's first-quarter earnings report and conference call, you'll find nothing but positive commentary from management, but the company's second-quarter gross margin guidance of 75.5%, plus or minus 50 basis points, is what I would call a red flag.

After a one-year gross margin increase of 13.8 percentage points, a projected decline of 235-335 basis points (range 78.35%-75%-76%) may sound inconsequential. But it's notable given that external competitors are doing well with their own AI-GPUs. Moreover, Nvidia's top four customers, accounting for roughly 40% of its revenue, are developing AI-GPUs in-house for their own data centers.

This forecast of sequential quarterly gross margin declines seems to indicate that Nvidia's pricing power has peaked. As the GPU shortage eases, so will Nvidia's pricing power.

The third reason I don't want to have anything to do with Nvidia after the 10-for-1 stock split is, again, historical, but this time I'm talking about valuation.

As I said, NVIDIA is still relatively cheap based on its PEG ratio (price to earnings growth ratio). But based on trailing twelve months (TTM) sales, NVIDIA is reaching historic highs that can only be matched by Amazon and Cisco Systems Before the dot-com bubble burst.

Cisco Systems peaked at just under 39 times TTM sales in late March 2000, while Amazon was over 43 times TTM sales in January 1999 but has since fallen sharply. Nvidia currently trades at 38 times TTM sales.

History may not repeat itself perfectly on Wall Street, but it does tend to rhyme, and for these reasons, I would not touch this AI giant with a 10-foot pole.

Should I invest $1,000 in Nvidia right now?

Before you buy Nvidia stock, consider the following:

of Motley Fool Stock Advisor The analyst team Top 10 Stocks Here are the stocks investors should buy now… and Nvidia wasn't among them. The 10 stocks selected have the potential to generate big gains over the next few years.

Things to consider NVIDIA This list was created on April 15, 2005…If you invested $1,000 at the time of recommendation, That comes to $741,362.!*

Stock Advisor With portfolio construction guidance, regular updates from our analysts, and two new stock picks every month, we provide investors with an easy-to-follow blueprint for success. Stock Advisor The service is More than 4 times S&P 500 Recovery Since 2002*.

View 10 stocks »

*Stock Advisor returns as of June 3, 2024

John Mackey, former CEO of Amazon subsidiary Whole Foods Market, serves on The Motley Fool's board of directors. Sean Williams invests in Amazon. The Motley Fool invests in and recommends Amazon, Apple, Cisco Systems, and NVIDIA. The Motley Fool has a disclosure policy.

Nvidia completes 10-for-1 stock split: Here's why you wouldn't touch this artificial intelligence (AI) giant with a 10-foot pole This article was originally published by The Motley Fool.