Rise tied to Fed, not fundamentals

November’s stock path was a textbook “policy beta.” As the probability of a December interest rate cut rose and fell, S&P 500 futures also moved in tandem. Seasonalists insisted on strength. Instead, AI optimism has cooled, and a prolonged government shutdown has clouded the outlook. As a result, macro expectations, rather than performance revisions, did the heavy lifting.

AI spending: From tailwind to challenge

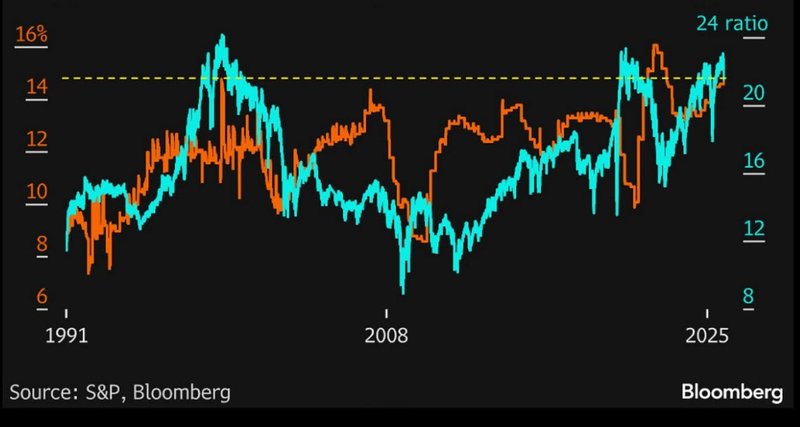

While the proliferation of AI infrastructure remains massive, its ability to float all boats is less certain. With circular financing, increased use of debt by cash-rich platforms, and pure capital concentration, investors are asking where marginal returns will settle. The S&P 500 is trading at more than 22 times expected earnings, a level associated with the dot-com peak and post-pandemic surge, and should maintain record operating margins. History says that’s a tall order.

Source: Bloomberg

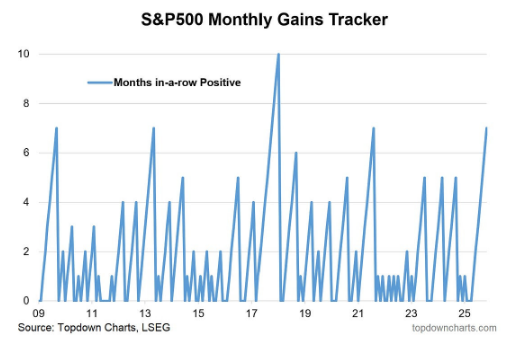

Good news. Since 2009, there have been five winning streaks of seven months or longer on the S&P 500. This includes current results. Bad news: 80% of streaks ended after 7 months.

Source: Todd Down Chart

Since 1928, the S&P 500 is up 73.2% in December, the most of any month. Average gain +1.28%. Since 1945, the average December return has been +1.50%. All-time highs may be within reach, but the Fed is in control.

Source: BofA

Trade tensions: slowing trend, still present

Although the U.S.’s effective tariff rate has eased from its spring peak, it remains well above the recent standard of less than 3%. The combination of levy and execution uncertainty is a slow-moving headwind for global supply chains and equity risk premia, easy to ignore in good times but hurt when growth stagnates.

Rate Pass: Less runway than the tape suggests

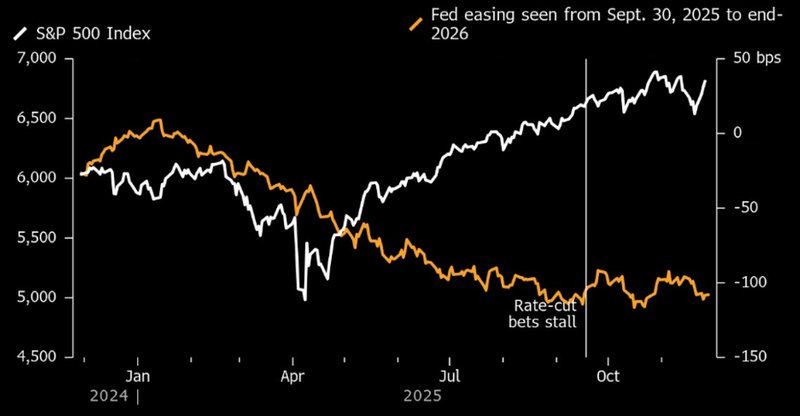

The market’s focus on whether the first rate cut will arrive on Dec. 10 or late January is missing the big picture. Pricing currently suggests cumulative rate cuts of around 75bps through the end of 2026. This is not a typical relaxation cycle. Recent momentum in stocks has waned as hopes for a quick and deep rate cut have stalled.

Source: Bloomberg

What must be right and what can go wrong

For this rally to last, three things will need to come together: resilient growth, sustainable profit margins, and modest but sustained policy support. Any of the following can cause an imbalance.

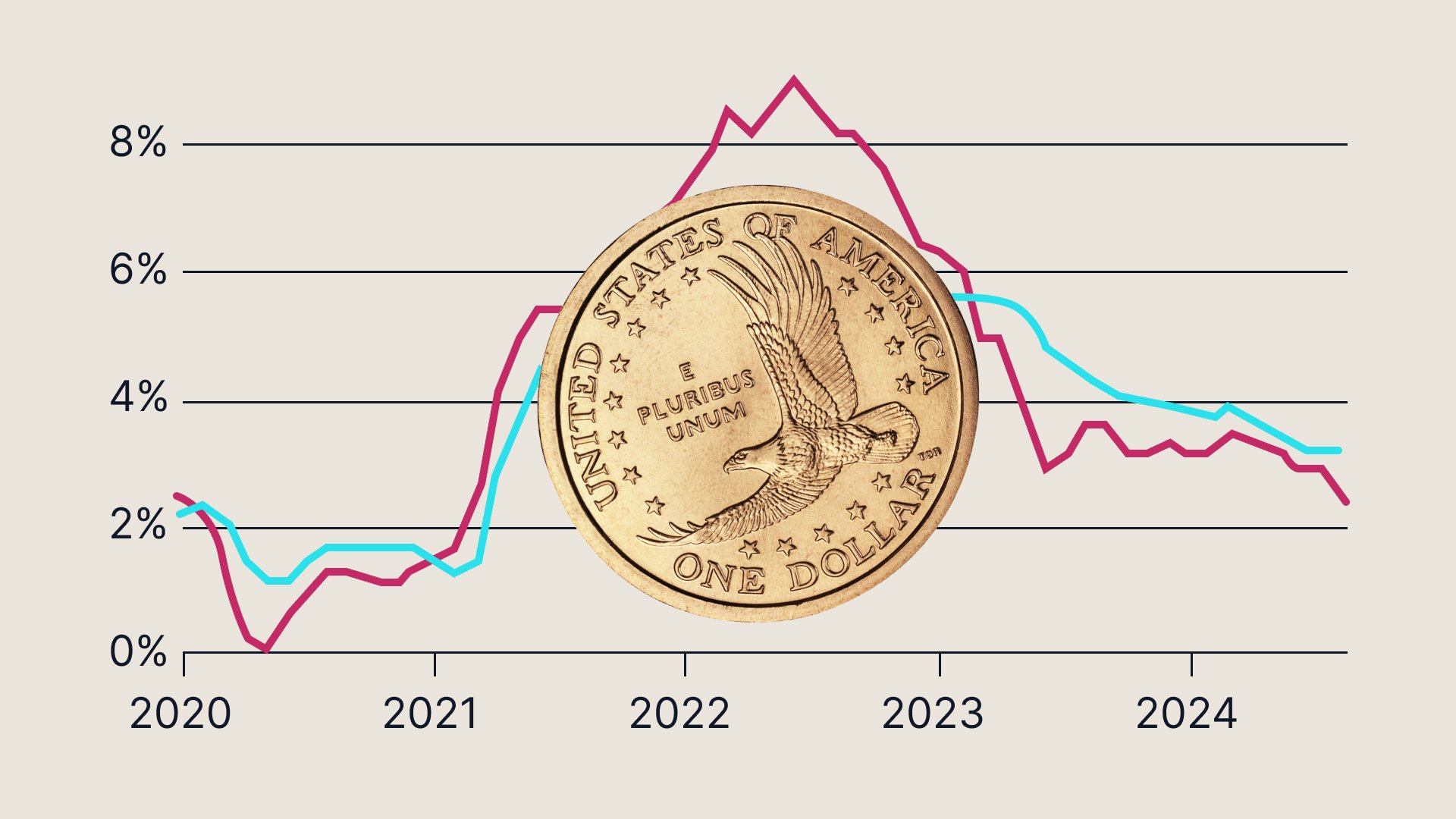

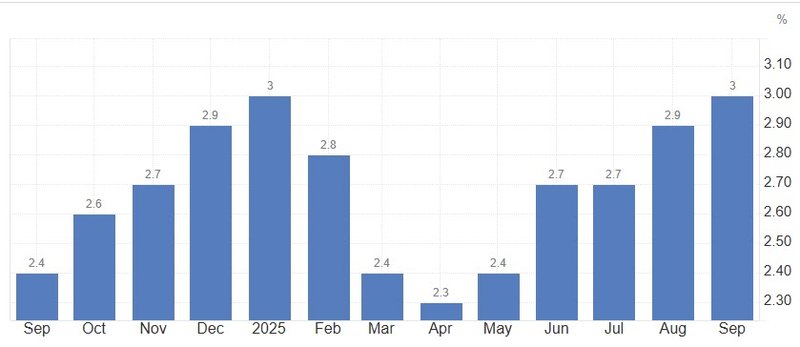

Sticky inflation: Running about 1pp above target will cause the cut to be paused and multiple pressures may be applied.

Source: Trading Economics

Growth rate: If labor and demand weaken further, even faster mitigation measures may not be able to offset the sell-off in stocks.

Financial situation: It’s already easy by historical standards. If you loosen it further, you risk creating boom-and-bust dynamics instead of a soft glide.