Following Openai's renowned partnership with major AI infrastructure projects SK Hynix and Samsung, investor sentiment has received a new boost across the semiconductor sector. Integris (ENTG) is one of the inventory that captures the wave of optimism.

Check out our latest analysis from Integris.

Although Integris has seen a pocket of momentum alongside the AI-fuel rally in semiconductors, even if enthusiasm returns to news of major chip demand drivers like Openai's new partnership, shareholder revenues remain below the flat for the year. While recent headlines have helped sentiment, investors are looking to see if new optimism leads to stronger, lasting benefits from here.

If you're looking for the next thing in AI buildouts for high-tech hardware, check out our full list for free.

Entegris trading is a big question of whether investors are seeing undervalued entries after achieving the analyst price target's shy target, and after a period of low performance, or whether prices are already reflecting expectations for future AI growth.

Most Popular Stories: 0.4% Underrated

Integris was last closed at $98.61 and is very close to fair value estimates according to the most widely held narrative. This setup frames the argument as the price of the stock is roughly consistent with what is calculated from growth forecasts and risk factors.

Investment and leadership in advanced materials for next generation nodes, such as CMP slurry, selective etching, deposition materials, and more, entegris leverages future node transitions (advanced logic, 3D NAND, HBM) to increase semiconductor complexity and support higher ASPS and improved gross profits.

Read the complete story.

Do you want to see what makes the Bulls believe that Etegris can continue to justify that premium? The story is leaned with the trust of the positive future growth and margins of 2028. What promotes such optimism? Find the bold number that translates this price target.

Result: Fair value of $99 (right)

Read the story in full and understand what lies behind the predictions.

However, sustained global trade uncertainty and continuous operational inefficiency could easily challenge the optimistic outlook that many analysts currently hold for Integris.

Find out about the important risks to this Entegris story.

Another view: Examine price ratio lenses

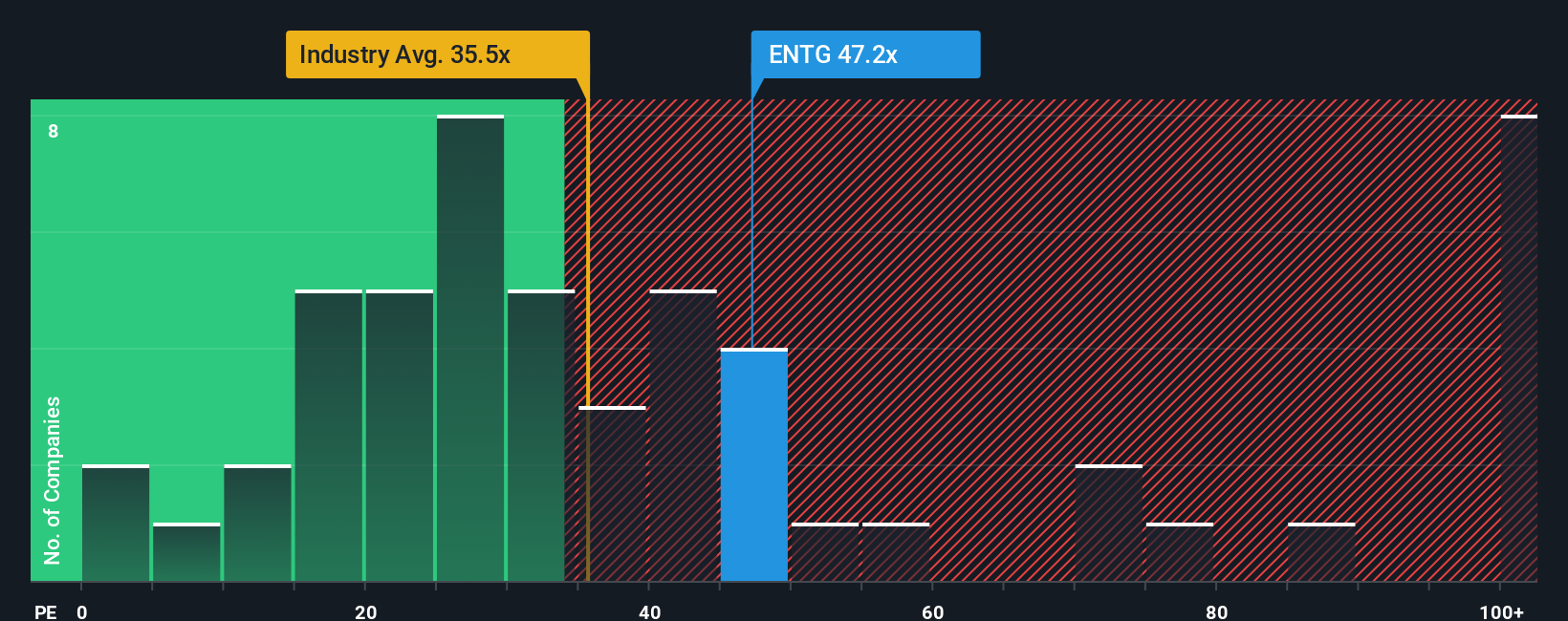

While many investors use the expected returns to set fair value, a closer look at Integris prices and rates of return reveals another picture. Traded at 50.6x revenues, Entegris is well above the industry average of 37.7 and its fair ratio of 32.3. This suggests that the stock may be priced for perfection. Does this premium reflect authentic growth intensity or will it put investors at higher risk if market expectations change?

See what the numbers say about this price. Find out our ratings breakdown.

Build your own entegris story

If you have another take, or if you want to dig deeper into the numbers, you can create your own Entegris story in just a few minutes. Do it your way.

A great starting point for Integris' research is an analysis that highlights two important rewards and one important warning sign.

Looking for more investment ideas?

Beyond the obvious choices, you may be missing out on the most powerful opportunity. Place yourself in front of the crowd and start searching smarter.

This article simply by Wall Street is inherently common. We provide commentary based on historical data and analyst forecasts, and use impartial methodologies, and our articles are not intended for financial advice. It is not a recommendation to buy or sell stocks and does not take into account your goals or financial situation. We aim to deliver long-term intensive analysis driven by basic data. Please note that the analysis may not take into account the latest price-sensitive company announcements and qualitative material. Simply put, the Wall ST has no position in the stock mentioned.

The evaluation is complicated, but we're here to simplify it.

Discover whether Entegris is underestimated or overrated in our in-depth analysis Fair value estimates, potential risks, dividends, insider trading, and its financial position.

Access Free Analytics

Do you have feedback in this article? Are you worried about the content? Please contact us directly. Alternatively, please email editorial-team@simplywallst.com