- Cognex (NasdaqGS:CGNX) reported fourth-quarter 2025 financial results indicating a return to profitable growth.

- Management emphasized that portfolio optimization and cost measures have led to a turnaround in business.

- The quarter saw strong launches of new AI-powered machine vision products and new customer acquisitions.

Cognex, trading at $58.79, is back in the spotlight after its fourth-quarter 2025 results showed a shift to profitable growth supported by operational changes. The company’s stock has been on a roll lately, up 34.5% over the past week, 43.7% over the past month, and 59.2% since the beginning of the year, for a return of 78.7% over the past year. For investors focused on machine vision and industrial automation, this combination of earnings progress and stock price momentum is intriguing.

The company is attributing its improved performance to selling non-core businesses, consolidating its sales force and focusing on AI-powered products that are likely to resonate with customers. Efforts to expand margins and acquire new customers are reflected in the current reported results, and a central consideration for investors is how sustainable this profit profile is if Cognex continues to execute on its current strategy.

Add it to your watchlist or portfolio to stay up to date on Cognex’s most important news stories. Or explore our community and discover new perspectives on Cognex.

📰 Beyond the headlines: One risk and one right direction for Cognex that every investor should pay attention to.

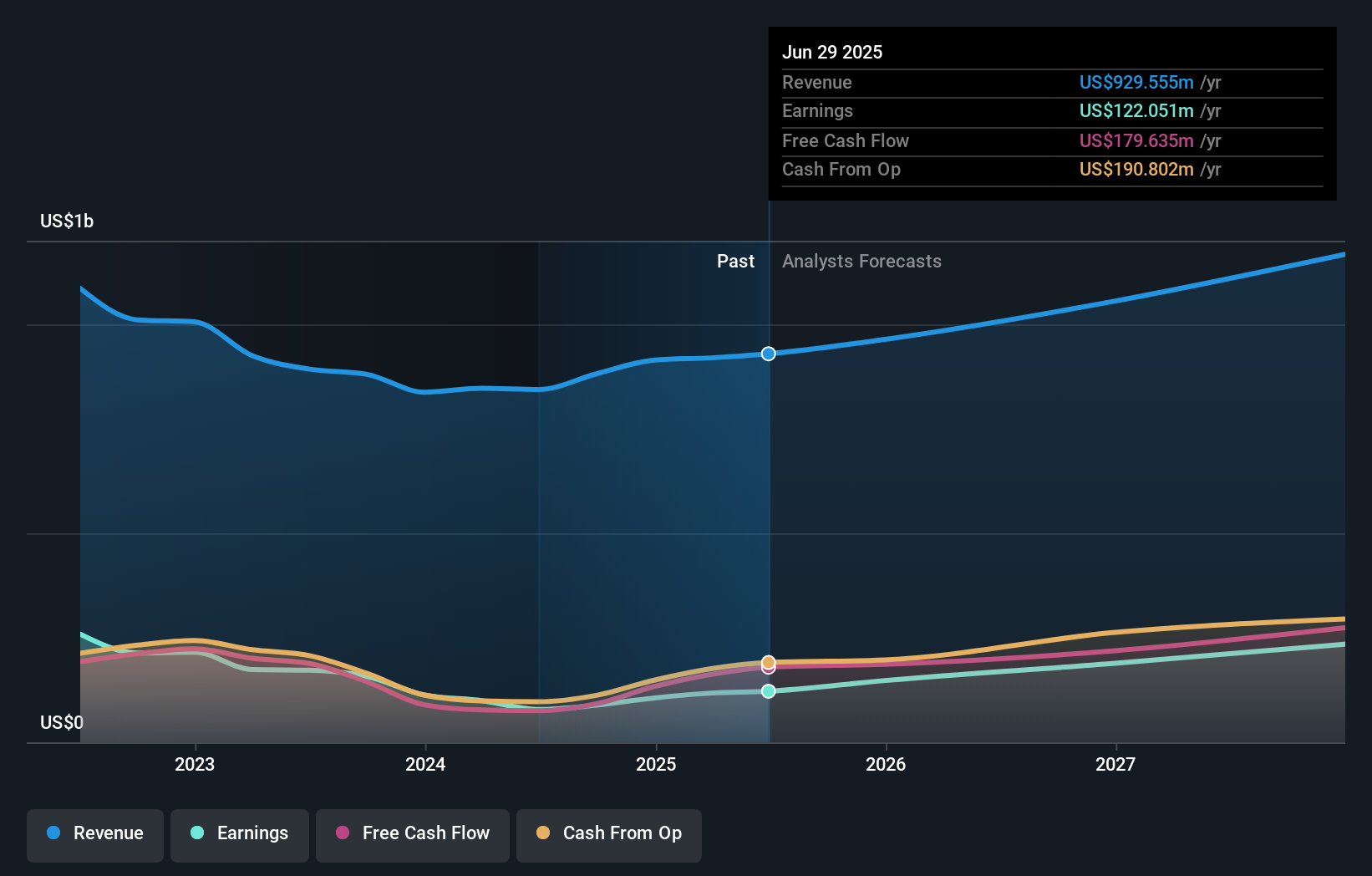

Cognex’s Q4 2025 update covers not only revenue and profit growth, but also how the business is being restructured. Revenue for the quarter was US$252.34 million, net income was US$32.66 million, and full-year sales were US$994.36 million, alongside initiatives such as exiting non-core businesses, rolling out AI-powered vision products, and overhauling the sales force. This combination is important for investors. This is indicative of business models that seek to rely more on high-value, software-rich systems and broader customer bases, such as logistics, consumer electronics, and packaging, where demand for automation is strong.

How does this fit into the Cognex story?

- A return to profitable growth in 2025, supported by AI-powered products and an overhauled sales force, is consistent with the narrative that cost discipline and automation demand could support margins and share buybacks.

- The company’s focus on AI and cloud-enabled software could be tested by competition from peers such as Keyence, Teledyne and Rockwell Automation, which also target machine vision and factory automation and could pressure pricing or win deals if software transitions are slow.

- The completed US$500 million share buyback and new authorizations are important capital allocation moves, but they are not fully reflected in the business-focused narrative, and these may impact how future earnings per share trends compare to overall earnings growth.

Understanding a company’s value starts with understanding its story. Check out one of the top articles in Cognex’s Simply Wall St community and decide what it’s worth to you.

Risks and rewards investors should consider

- ⚠️ Cognex operates in a highly competitive machine vision market, and hardware pricing pressures and the presence of lower-cost providers could put pressure on profits if AI and software implementations fall behind schedule.

- ⚠️ Stock prices have been volatile compared to the U.S. market over the past three months, so news and guidance updates can lead to greater short-term volatility.

- 🎁 Management is aiming for continued efficiency improvements, and analysts expect revenues to increase over time, which, if achieved, could support Cognex’s efforts to maintain a higher quality profit mix.

- 🎁 The combination of AI-powered product launches, revamped sales approaches, and completed share buybacks suggests that management is proactively shaping its business and capital structure, rather than simply relying on end-market cycles.

Future points of interest

From here, it’s worth tracking whether Cognex can continue to add new customers at its 2025 pace while maintaining or improving profits as its AI-powered services are more widely rolled out. Stay tuned to see how Q1 2026 revenue and profitability compare to the company’s guidance range, and how quickly the newly authorized share buybacks are executed. Competitive responses from other industrial automation and machine vision players will also impact pricing and win rates in logistics and electronics projects.

To stay on top of how the latest news impacts the Cognex investment story, visit the Cognex Community page to stay up to date on the community’s top stories.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: AI stock screener and alerts

Our new AI Stock Screener scans the market for opportunities every day.

• Dividend powerhouse (yield 3% or more)

• Small-cap stocks that are undervalued due to insider purchases.

• High-growth technology and AI companies

Or build your own metrics from over 50 metrics.

Explore for free now

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.