Why Zscaler’s new AI security hire matters to investors

Zscaler (ZS) has created a new senior role in Agent AI Security, hired Dr. Swamy Kocharakota to fill the role, and placed AI-driven security architecture at the center of its product roadmap.

The move ties in with a shift in AI from simple chat tools to autonomous agents that act as both users and applications, a shift the company sees as raising new security questions for large enterprises.

Check out our latest analysis for Zscaler.

Mr. Kocharakota’s appointment came at a time when Zscaler’s stock price was declining, with its 30-day price-earnings ratio dropping 10.08% and its 90-day price-earnings ratio dropping 34.54%, despite its one-year total shareholder return of 8.15% and three-year total shareholder return of 74.01%.

If you’re interested in seeing how the AI security theme ripples through the market, it might be a good time to explore other high-growth technology and AI names through High-Growth Technology and AI Stocks.

Although Zscaler’s stock price has declined over the past quarter, it still represents a solid multi-year total return and trades at a discount to both analyst targets and some internal estimates, so the key question is whether the gap represents an opportunity or whether the market is already pricing in future growth.

11.7x price-to-sales: Is it justified?

On a simple basis, Zscaler’s P/S of 11.7x is well above many of its peers, even though the stock’s price of $208.66 is below some fair value estimates.

P/S compares a company’s market value to its annual revenue. This is a common way to evaluate rapidly growing, often still unprofitable software names. At 11.7x, investors are paying a higher price for each dollar of Zscaler’s $2,833.27 million in sales than the average US software stock, suggesting the market values the company’s cloud security position and expected growth profile.

The gap is pretty obvious. The US Software industry has an average P/S of 4.5x, and Zscaler also rates it as expensive compared to its peers’ average of 10.8x. Compared to Simply Wall Street’s estimated fair P/S ratio of 10.5x, the current multiple remains high and indicates where valuations could be heading if sentiment and growth expectations reset.

Explore Zscaler’s SWS Fairness Ratio

Result: 11.7x price to sales (overvalued)

However, we also need to consider risks such as the continued net loss of US$41.04 million and the potential for compression of the high expectations built into the 11.7x P/S ratio.

Find out about the key risks to this Zscaler story.

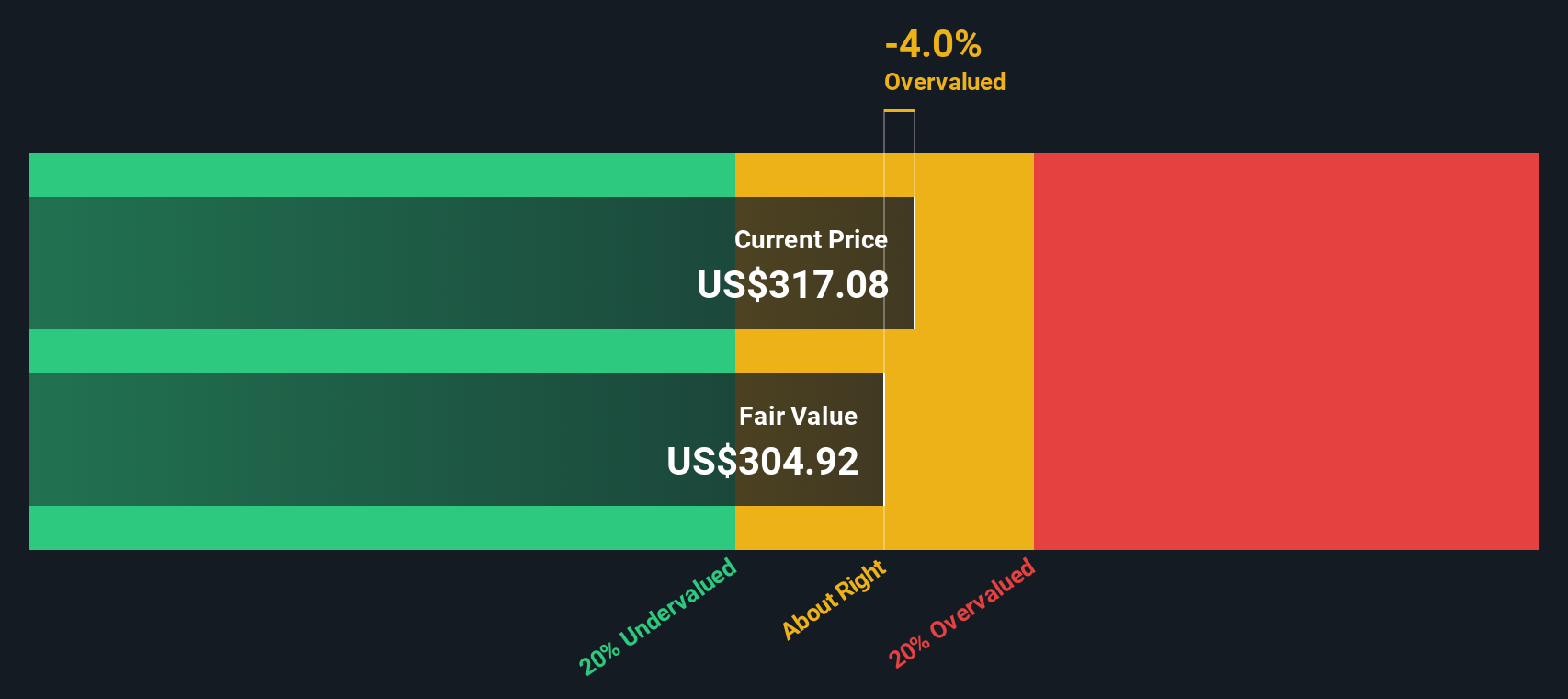

Another look: DCF is pointing in a different direction

Although the P/S ratio of 11.7x looks expensive, our DCF model tells a different story, with Zscaler trading at approximately 27.9% below its estimated fair value of US$289.50. One lens suggests premium, the other suggests discount. Which risk is more important to you: multiple compressions or potential reassessment?

Find out how the SWS DCF model arrives at fair value.

Simply Wall St runs Discounted Cash Flow (DCF) on every stock in the world every day (check out Zscaler for example). The entire calculation is fully illustrated. Track your results with a watchlist or portfolio and get alerts when they change, or use our stock screener to discover 880 stocks that are undervalued based on cash flow. When you save your screener, you’ll also get alerts when new companies match, so you never miss out on potential opportunities.

Build your own Zscaler story

If you look at the numbers and come to a different conclusion, or just want to rely on your own work, you can use Do it your way to build a complete view in minutes.

A great starting point for Zscaler’s research is our analysis, which highlights 3 key benefits and 1 key warning sign that could influence your investment decision.

Looking for more investment ideas?

If Zscaler catches your attention, don’t stop there. The same tool can quickly uncover other potential opportunities worthy of being on your watchlist.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

Evaluation is complex, but we will simplify it here.

Discover whether Zscaler is undervalued or overvalued with our in-depth analysis. Fair value estimates, potential risks, dividends, insider transactions, and financial condition.

Access free analysis

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.