Natera (NTRA) is back in the spotlight after posting 39% year-over-year revenue growth in its fourth quarter, a projected 35% revenue increase for the full year of 2025, and guidance on the latest in AI-powered oncology.

Check out our latest analysis for Natera.

The past year has been eventful for Natera, with AI-focused oncology partnerships, new clinical data readouts, and prenatal testing expansion all contributing to a one-year total shareholder return of 46.03% and a 90-day price return of 22.61%. This suggests momentum is building despite the recent share price decline.

If you’re focused on breakthroughs in cancer and prenatal testing, now might be a good time to see what else is in store for healthcare stocks.

Given Natera’s 2025 revenue target of US$2.3 billion, its AI-focused oncology partnerships, and its stock’s recent strength, the key question now is whether there is upside left at its current valuation or whether the market is already pricing in future growth.

Most popular story: 1.5% underrated

According to the most popular theory, Natera’s fair value is $234.68, slightly above its previous closing price of $231.25 and roughly above its market price.

With investments in new product launches (including Fetal Focus NIPT, Signatera Genome, and AI-based biomarkers) and a strong R&D pipeline, Natera is positioned to capture growth from long-term trends in personalized medicine and early detection and support future revenue growth.

Read the whole story.

Want to know what revenue path and margin shifts that valuation supports? This story relies on accelerating earnings, improving profitability, and premium forward multiples. The detailed numbers are where the story really gets interesting.

Result: Fair value $234.68 (approximately right)

Read the full explanation to understand what’s behind the predictions.

However, there remains a real risk that high R&D and AI spending will continue to pressure margins, or that clinical, regulatory, or reimbursement setbacks will slow growth.

Find out about the main risks in this Natella story.

Another look: Price vs. Sales sends out warning flags

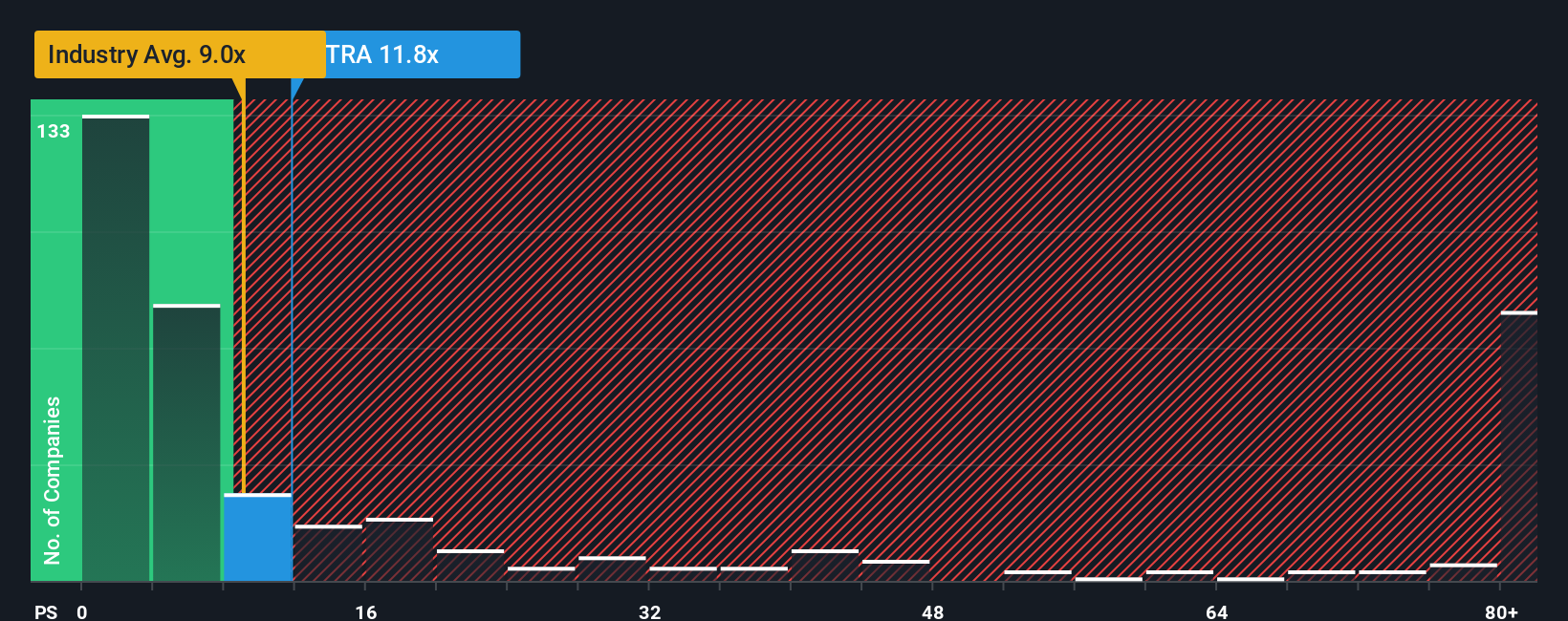

While the popular narrative points out that Natera is trading close to fair value, the P/S ratio tells a different story. At 15.1 times sales, the company’s stock price is significantly higher than the U.S. biotechnology industry’s 12.1 times, the peer average of 8.3 times, and the fair ratio of 8.7 times. This gap suggests investors are paying a high premium, so the real question is whether they are comfortable assuming that much at the current price.

See what the numbers say about this price. Please check the rating breakdown.

Build your own Natella story

If this description doesn’t exactly match how Natera sees it, you can see the numbers yourself and form a custom view in minutes. Do it your way.

A great starting point for Natera Research is our analysis, which highlights 1 significant payoff and 1 significant warning sign that could influence your investment decision.

Ready to explore more investment ideas?

If you’re interested in Natera, don’t stop here. Take a few minutes to look at other opportunities before the next wave of market moves passes.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

Evaluation is complex, but we will simplify it here.

Discover whether Natera is undervalued or overvalued with our in-depth analysis. Fair value estimates, potential risks, dividends, insider transactions, and financial condition.

Access free analysis

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.