You can hear about AI anywhere, whether it's news, board discussions, social media, personal conversations. New AI products and tools are constantly evolving, and discussions on their sustainability, safety and scope are becoming popular. Not much attention is paid to real-world corporate use, the risks generated by AI, and tools to minimize risk from a business perspective.

This set of white papers is designed to assess what risk managers can do to assess risk, the protections they can implement, and the coverage of insurance available under current insurance contracts.

Artificial intelligence has been based on a variety of machine learning technologies since the 1950s1. Deep learning techniques have been underway since 2010, allowing AI to become self-learning, and ultimately bringing generative AI, such as ChatGpt, to the forefront. These developments stimulate the imagination of businesses and individuals everywhere, resulting in significant investment in the field.

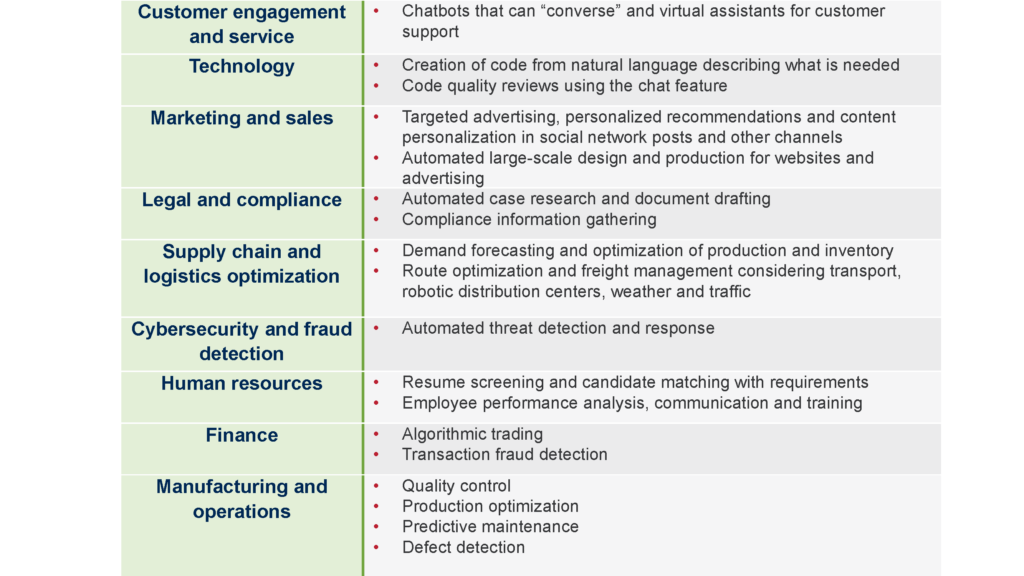

A Day of Commercial AI's Life

Exposure created by AI

Currently, existing examples of AI litigation are primarily focused on content creators who are suing AI companies to use content to train AI models without permission. However, the rapid rise in AI use indicates that litigation and direct impact risks continue to evolve. Perceived risks include:

- ai hallucination: AI models, especially large language models (LLMS), can make up things. In response to questions about crossing the English Channel on foot, LLM produced specific details about the world record holder and intersection. A legal investigation conducted by LLM has created and cited cases that do not exist.

- Privacy Invasion: Personal information shared with the AI model can lead to data breaches. Video Call AI Note Takers can infringe your non-disclosure agreement and obligations. The use of “Shadow AI,” or LLMS to analyze information without corporate approval, has been over 70%, according to some studies.

- IP loss or infringement: Content created by AI can infringe the photos, codes, music, trademarks and personal identifiers used to train algorithms. The court determines who is liable and the scope of damages.

- Model bias: Models can result in systematic errors that produce unfair or biased outcomes for a particular group. The employment resume review model supports a type of workforce that does not adhere to the requirements to limit bias and discrimination. Facial recognition systems sometimes have less accuracy for people of color.

- Loss of reputation: It is possible that content generated by inaccurate or discriminatory AI may be published. In one example, the airline's chatbot “hastisation” rules suggest that passengers can retrospectively apply for bereavement fares after their grandmother's death. The lawsuits continued in a wide range of media outlets that needed public relations response.

- Loss of business revenue: As businesses rely more on AI and staffing is tailored to take advantage of its efficiency, technology obstacles can cause business functions to halt for longer periods of time while technology problems are resolved without human backup. The resulting revenue losses depend on the use of the AI platform, but they may be important.

- Regulatory fines: Many of the proposed laws do not distinguish between new deep learning models and old established AI use. Once the proposed law comes into effect, some of its current use could become illegal.

At Brown & Brown, we believe that AI-related risks will evolve rapidly, with the impact being individualized depending on the implementation entities, the applications created, the development, and the technologies used. AI potentially affects insurance and uninsured risks across many coverages. The Brown & Brown team tracks development and can provide insight into developing dangers. Cyber risk models can include AI risk scenarios to assess individual exposures. To understand more about our capabilities, contact Brown & Brown representatives.