The startup era is back, but this time founders are leveraging AI to avoid one of their biggest early costs: hiring employees.

A report released this week by the Bank of America Research Institute found that the number of “propensity businesses,” or businesses identified by the Census Bureau as likely to hire employees, increased 15.1% in January from the same month a year earlier. Meanwhile, the number of enterprise applications that explicitly plan to hire employees decreased by 4.4%.

The trend comes as small and medium-sized businesses invest at record levels in technology services, including AI, with spending up 14% last month from a year ago, according to Bank of America analysts.

“This may be associated with increased productivity,” the report states.

Among small businesses, retail led the way in tech spending last month, increasing by more than 25%, followed closely by manufacturing, BofA added.

Small businesses, typically defined as businesses with fewer than 500 employees, employ about 45% of Americans, and a significant decline in employment at this group of businesses could have a major impact on the labor market.

After the Federal Reserve decided to keep interest rates on hold this week, Chairman Jerome Powell said private sector employment is stagnant. Employers cut 92,000 jobs in February, leaving the unemployment rate at 4.4%.

“There is effectively zero net job creation in the private sector,” Powell added at a press conference this week.

Large enterprises are also increasingly leveraging AI to do more with less. The latest evidence: Fintech company Brock made the decision last month to lay off about half its workforce, but CEO Jack Dorsey said intelligence tools would “enable new ways of working that fundamentally change what it means to start and run a company.”

Some say Mr. Block’s move amounts to “AI cleaning” and that last month’s layoffs were actually aimed at correcting overhiring during the pandemic. Amrita Ahuja, Block Chief Financial Officer and Chief Operating Officer, said: luck That wasn’t the case earlier this month.

Meanwhile, AI was cited in about 8% of all layoff announcements in 2026, or about 12,304 announcements, according to a study by executive outplacement firm Challenger, Gray & Christmas.

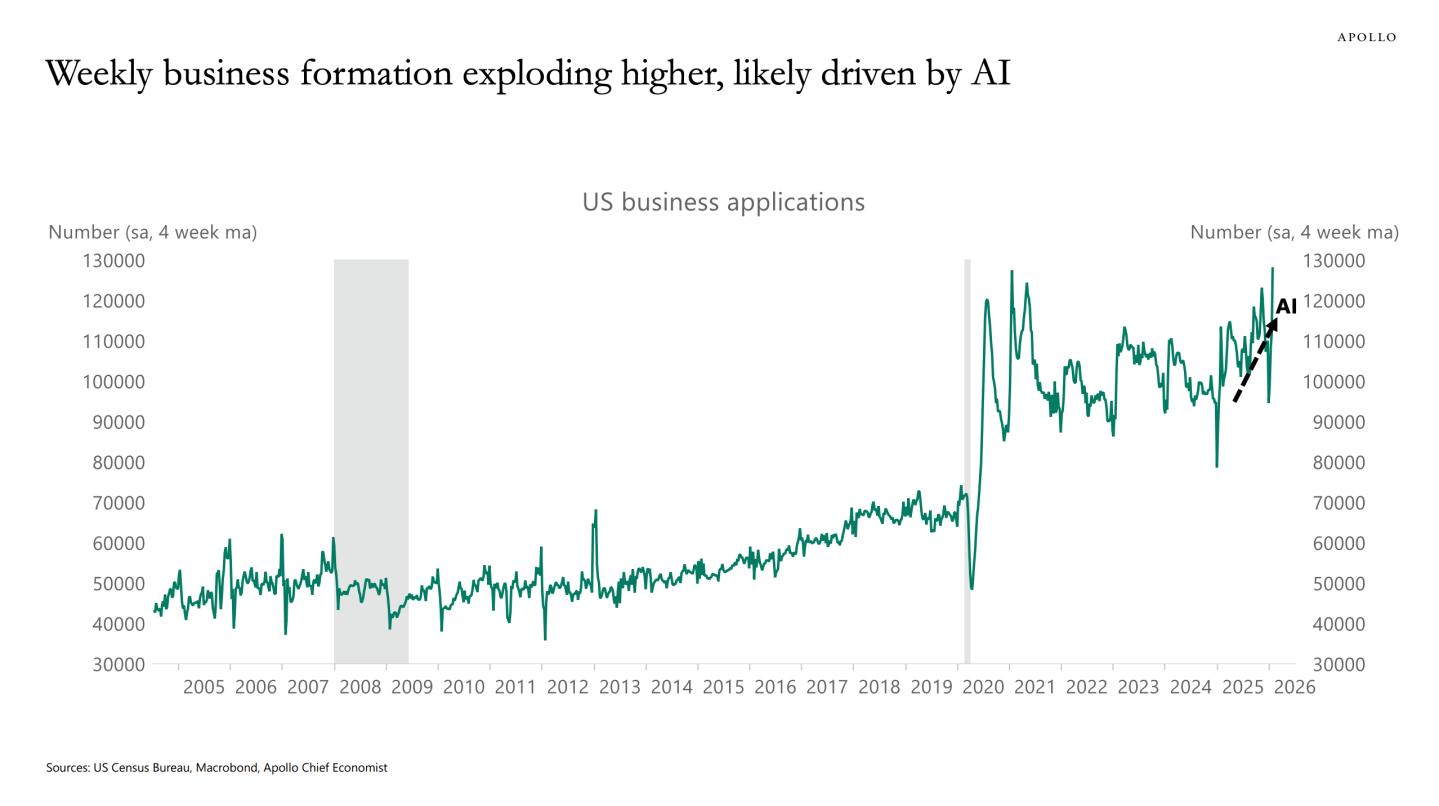

Indeed, Torsten Slok, chief economist at Apollo, predicted that the rapid increase in the number of companies being founded will be a boon for the labor market as a whole.

“As these companies scale, they create jobs, underscoring that AI is likely to strengthen rather than destroy the U.S. labor market,” he said in a memo earlier this month.

Engineer replacement

Others, like Andy Tan, a partner at Silicon Valley venture capital firm Draper Associates, aren’t so sure. On average, startups he spoke to last month are cutting their engineering teams by a third, he said. luck, It reveals how AI tools can be beneficial for early-stage founders.

In many cases, these startups find that putting money into AI tokens is a better investment than writing 3-5 times the nominal cost of code and increasing headcount.

“If you do the math, we don’t need that many engineers,” he says, adding that most knowledge work can be easily replaced.

In the future, Tan said, AI tools may even allow solopreneurs to cut down on staff entirely and instead create armies of agents, allowing them to create their own “founderless unicorns.”

new playbook

The idea of using AI tools to scale rapidly was quickly embraced by a new generation of young, tech-savvy entrepreneurs.

Two years ago, while attending Northwestern University and Duke University, respectively, Rudy Arora and Sarthak Dhawan launched TurboAI, an AI-powered tool that turns lecture notes into flashcards and quizzes for less than $300 in initial investment.

The childhood friends, now 21, have been able to grow the company to 8.5 million users over the past two years and, thanks in part to AI, have just 13 employees and earn about $1 million a month, the two said. luck. And despite raising $750,000 in a funding round two years ago, Arora said he preferred not to spend it because it was profitable.

“If we were the company we were two-and-a-half years ago, we would have needed more than 100 employees,” Arora said. “The only reason we’re able to do that now with 13 employees is because of AI.”

He added that what previously required a product manager and five engineers can now be done by one technical employee with an AI agent.

Dhawan, co-founder of Arora, added that he believes startups are just discovering how AI can enhance their businesses. Still, technology is already changing the way entrepreneurs work. During the startup boom that began more than a decade ago in 2008, starting a company often required experienced programmers and venture capital funding, Dhawan said. However, the co-founders’ experience building TurboAI proves that this is not necessarily the case.

“People who are even younger than us will be founding companies with even fewer resources,” Dhawan said.