Artificial Intelligence (AI) is advancing like never before and could have a huge impact on the world in the next decade. However, AI does not permeate from the ground like oil. Instead, massive amounts of data need to be processed quickly, requiring enormous computing power.

Advanced Micro Devices (AMD -1.96%) As a major semiconductor company, there should be many opportunities. Semiconductors are essentially the building blocks of computing systems and play a key role in building AI.

Rising demand for AI chips could drive exciting growth for AMD over the next decade. Here’s what investors can expect:

AMD leans heavily on AI

AMD is one of the world’s largest semiconductor companies. The company designs the central processing unit (CPU), the main brain inside a computer, and his GPU. AMD holds around 30% market share in the CPU market and just under 20% market share in the discrete GPU market. With AMD’s strong presence across the chip market, it should be broadly able to meet the growth in demand that AI will create for its chips.

Experts believe AI could add $13 trillion of economic output to the global economy by 2030. This could lead to significant growth in semiconductor stocks, with analysts expecting AMD to post strong growth over the next few years. The average forecast is that by 2027, sales will almost double and earnings per share (EPS) will almost triple.

More than a year ago, AMD bought Xilinx, a programmable chip specialist known for its forward-thinking designs, for $49 billion. Xilinx should offer AMD options in designing products specifically for AI applications. An investor event is planned next month to announce several new products aimed at the data center and AI markets.

Basically similar to Nvidia

AMD’s most direct competitors are Nvidiaspecializes in discrete GPUs and has around 80% market share. Nvidia has been garnering a lot of hype lately, largely thanks to his AI Catalyst. The stock has doubled since the beginning of the year.

Investors may need to compare companies in the same industry to identify the best investment opportunity for their capital. Consider Nvidia and AMD below. We can see that both companies have some similar financial metrics.

AMD Revenue (TTM) data by YCharts. TTM = subsequent 12 months. EPS = earnings per share.

For example, both companies have similar earnings, generate free cash flow at roughly the same conversion rate, and have similar expectations for long-term earnings growth.

at a much better price

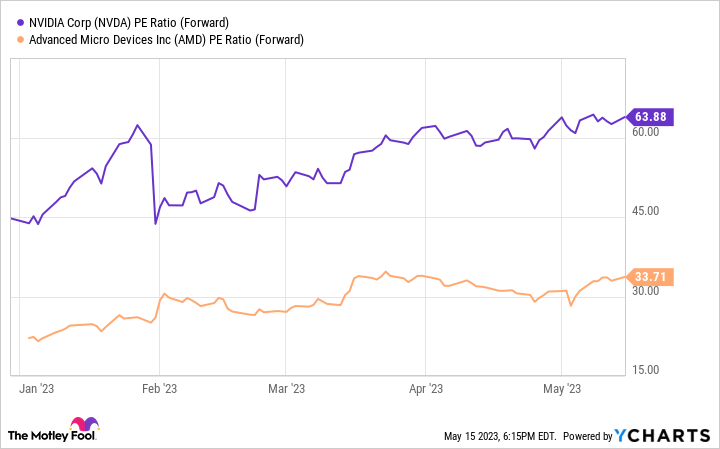

But looking at the valuations of each stock, we can see that the market is paying a hefty premium to Nvidia and AMD. At nearly double AMD’s price-to-earnings ratio, investors have hinted that NVIDIA’s earnings are of higher quality and deserve a premium. Is it the right decision some people may like AMD or Nvidia for whatever reason but from a pure numbers standpoint Nvidia justifies AMD having double his valuation I don’t know why.

NVDA PE ratio (forward) data by YCharts.

For investors looking for the best long-term returns, AMD seems to have fallen into Nvidia’s shadow. Meanwhile, the company has posted competitive financial numbers and is exposed to AI’s game-changing good news. Money wise, it sounds like AMD could be the winner in the next decade.

Justin Pope has no positions in any of the mentioned stocks. The Motley Fool has a position with Advanced Micro Devices and his Nvidia and endorses them. The Motley Fool has a disclosure policy.