NVIDIA’s latest industrial AI announcements highlight Siemens (XTRA:SIE) as a core software partner, integrating GPU acceleration tools, agent AI, and digital twin technology into semiconductor design, automotive engineering, and large-scale industrial environments.

Check out our latest analysis for Siemens.

Despite all the attention the NVIDIA news has focused on Siemens’ AI and digital twin efforts, the company’s 30-day stock return of 13.81% and year-to-date stock return of 12.36%, although its three-year total shareholder return of 60.32% and five-year total shareholder return of 74.41% still represent a solid long-term track record. The decline suggests that sentiment has cooled recently.

If this AI partnership has you thinking about where else industrial and infrastructure demand might go, it might be worth checking out these 25 power grid technology and infrastructure stocks.

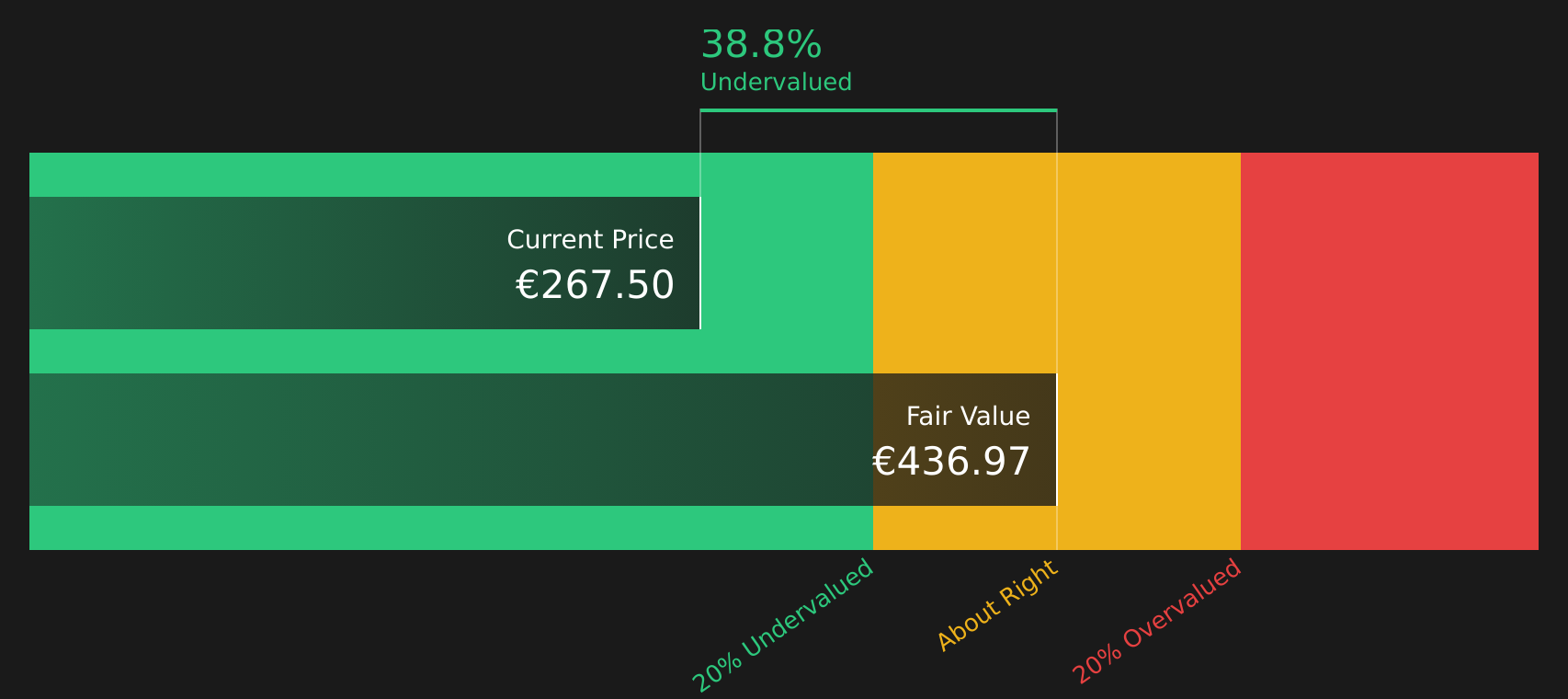

Siemens currently trades about 32% below certain intrinsic value estimates and about 31% below analysts’ average price target, a contrast to multi-year shareholder returns. Is this recent weakness a buying opportunity, or is future growth already priced in?

Most popular story: 1% overrated

The narrative fair value of 208.46 euros is slightly below Siemens’ closing price of 211.30 euros, raising questions about how much future growth is assumed.

Over the next five fiscal years, Siemens should see steady growth. The company’s financial framework targets comparable annual revenue growth of 5-7%. Using the 5% midpoint, sales would increase from 75.9 billion euros in 2024 to approximately 202.4 billion euros. 97 billion euros in 2029, which is a CAGR of approximately 5%. Margin growth is incorporated into segment targets: Digital Industries 17-23%, Smart Infrastructure 11-16%, Mobility 10-13%, Siemens Healthineers 17-21%. The revenue-weighted midpoint means group industry margins will be closer to 17% in FY2029, up from the current 15.5%.

Read the whole story.

Want to know why steady sales growth and improving margins are reflected in fair value numbers? This story is based on specific revenue bands, profit levels, and solid earnings multiples. A complete breakdown shows exactly how the parts stack up and how sensitive the results are to small adjustments.

Result: Fair value €208.46 (overvalued)

Read the full explanation to understand what’s behind the predictions.

However, this will depend on whether Siemens hits its revenue and margin targets, with a P/E ratio of around 18x and assuming current AI enthusiasm for industrial software continues.

Learn about the key risks to this Siemens story.

Another way to think about value

This 1% overvaluation thesis shows a fair value of €311.76 per share, in sharp contrast to our DCF model, which suggests Siemens is undervalued at its current price of €211.30. If your cash flow efforts are getting closer to your goals, is the narrative simply being too cautious?

Find out how the SWS DCF model arrives at fair value.

Simply Wall St runs Discounted Cash Flow (DCF) on every stock in the world every day (check out Siemens for example). The entire calculation is fully demonstrated. Track your results with a watchlist or portfolio and get alerts when they change, or use our stock screener to discover 242 high-quality undervalued stocks. When you save your screener, you’ll also get alerts when new companies match, so you never miss out on potential opportunities.

next step

With mixed signals regarding value and sentiment, it makes sense to look at the underlying data yourself without spending too much time forming a view. This includes weighing the 5 major rewards and 1 important warning sign.

Looking for more investment ideas?

If Siemens continues to strengthen its commitment to quality, don’t stop here. Screeners can surface other companies that fit different risk and income preferences.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: Manage all your stock portfolios in one place

What we created is The ultimate portfolio companion For stock investors, And it’s free.

• Connect an unlimited number of portfolios and see the total in one currency

• Alert you to new warning signs and risks via email or mobile phone

• Track the fair value of stocks

Try our demo portfolio for free

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.