It’s not uncommon to look at stocks you didn’t buy or sell too early with regret. This is all part of the investment learning process and is healthy.

But I think three stocks are currently trading at such discounts that you’ll regret not buying them at today’s prices. These three are leaders in artificial intelligence (AI), but each is well down from its all-time highs.

The three stocks I’m paying attention to are: microsoft (MSFT 1.92%), Nvidia (NVDA 3.17%)and broadcom (AVGO 2.99%). These three are sure to be expensive in a year’s time, and at current prices they look like great buys.

Image source: Getty Images.

1.Microsoft

It’s not often that Microsoft stock is historically cheap, but I think it is at this point. Microsoft underwent a corporate transformation about 10 years ago, moving from a perpetual licensing model to a subscription model. Additionally, we have started to focus on cloud computing. This marked a transition to a new company nearly a decade ago, so the metrics by which Microsoft was evaluated back then are irrelevant to the current state of the business.

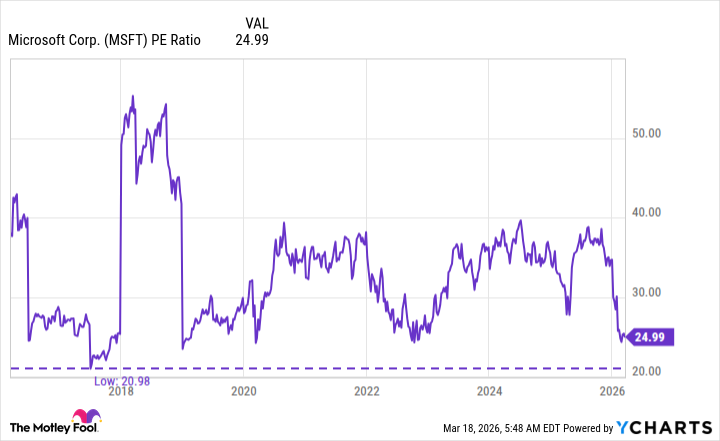

If you look at Microsoft’s price-to-earnings ratio over the past 10 years, it’s rarely been this cheap.

MSFT PE Ratio data by YCharts. P/E = price/earnings ratio.

We still have a ways to go before we are truly at the lowest price in the last decade, but we are rapidly approaching that point. Surprisingly, there’s actually nothing wrong with Microsoft’s stock, and this stock decline is unwarranted. While it looks like a great deal at the moment, investors will be hurting themselves later if they don’t act and buy now.

2. Nvidia

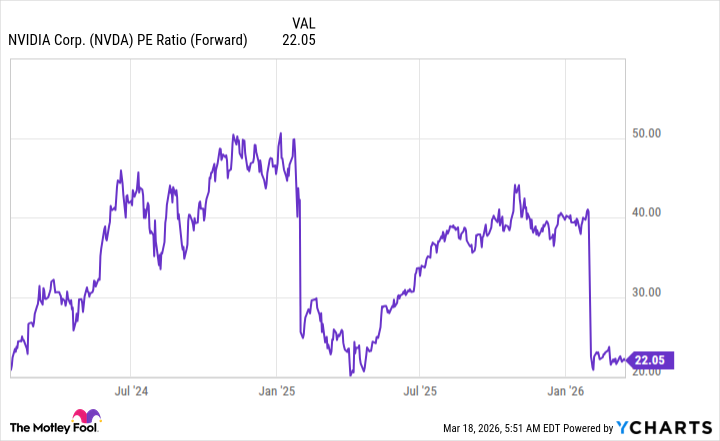

Nvidia is in a similar situation, but I’m going to use a different metric. Demand for Nvidia’s graphics processing units (GPUs) is off the charts, resulting in unrealistic growth. This fiscal year, Wall Street expects Nvidia to achieve an impressive 70% revenue growth rate. However, based on the stock’s valuation, this year will be the last of the rapid growth the market was expecting.

NVDA PE Ratio (Forward) data by YCharts. P/E = price/earnings ratio.

Nvidia’s forward price/earnings ratio is 22 times, and Nvidia’s price is S&P500 (^GSPC 1.51%)is trading at a forward P/E ratio of approximately 21 times. This low valuation essentially tells us that Nvidia will grow at a rapid pace this year, but will be a market-matching stock after that. But we know that’s not the case, as the demand for AI data centers is expected to last until at least 2030, and Nvidia continues to record new growth by launching new hardware.

As long as AI spending continues into next year and beyond, Nvidia is a bargain right now. I think this is a pretty safe bet and a no-brainer to buy the stock.

3.Broadcom

Finally, there’s Broadcom. Broadcom’s valuation isn’t cheap, but the company is expected to experience strong growth next year.

The main reason to invest in Broadcom now is the company’s custom AI chip business. These AI chips are designed in collaboration with end users and can deliver significant savings over traditional accelerated computing devices (such as Nvidia’s GPUs) for some applications. Demand for these chips is expected to grow further as AI hyperscalers seek to maximize capital expenditures, and Broadcom’s guidance supports that.

Today’s changes

(-2.99%) $-9.57

current price

$310.27

Key data points

Market capitalization

$1.5 trillion

daily range

$309.93 – $321.50

52 week range

$138.10 – $414.61

volume

1M

average volume

26M

gross profit

64.96%

dividend yield

0.78%

Broadcom expects its AI chip business to generate more than $100 billion in revenue by the end of 2027. For reference, the company’s AI semiconductor business (which includes products other than custom AI chips) generated $8.4 billion in revenue in its most recent quarter, up 106% year-over-year. With such growth expected over the next year, Broadcom is a must-buy stock right now. The market doesn’t expect Broadcom to achieve this outlook, otherwise the stock would be valued at a much higher level than its current market capitalization of $1.5 trillion.