- Recently, Elastic announced new integrations that bring observability for AI agents and applications running on Amazon Bedrock AgentCore directly into the Elasticsearch platform, as well as a $500 million stock repurchase program and enhanced Q2 2026 results.

- The company has also deepened its focus on AI through an investment in research software company Siren and the acquisition of the AWS Agentic AI specialization, highlighting its focus on production-grade autonomous AI systems.

- Next, consider how Elastic's enhanced AI observability using Amazon Bedrock AgentCore impacts its investment story and growth prospects.

The end of cancer? These 29 emerging AI stocks are developing technology that can identify life-altering diseases early on, such as cancer and Alzheimer's disease.

Resilient Investment Story Summary

To me, Elastic's core thesis is about its ability to transform AI search, observability, and security into a unified, must-have platform as workloads move to the cloud. While the Amazon Bedrock AgentCore integration and stronger guidance for FY2026 strengthens the short-term boost around AI-driven consumption, we feel the biggest risk remains increased competition from hyperscalers' native tools, which is not fully resolved by this news.

Amazon Bedrock AgentCore's observability integration stands out here because it directly supports Elastic's AI-centric growth catalyst by more tightly coupling Elastic's platform to AWS agent AI workloads. As enterprises increasingly seek end-to-end production-grade AI observability on LLM agents, this type of tight integration could help Elastic remain relevant as customers weigh native options for hyperscalers and specialized platforms.

But despite these AI tailwinds, investors still need to be aware of how quickly hyperscalers' native services can become a reality.

Read the full story on Elastic (it's free!)

Elastic's story projects revenue of $2.3 billion and revenue of $50.5 million by 2028. This would require annual revenue growth of 13.9% and an increase in revenue of $134 million from the current -$83.5 million.

We reveal how Elastic's projections yield a fair value of $106.22, 42% above the current price.

explore other perspectives

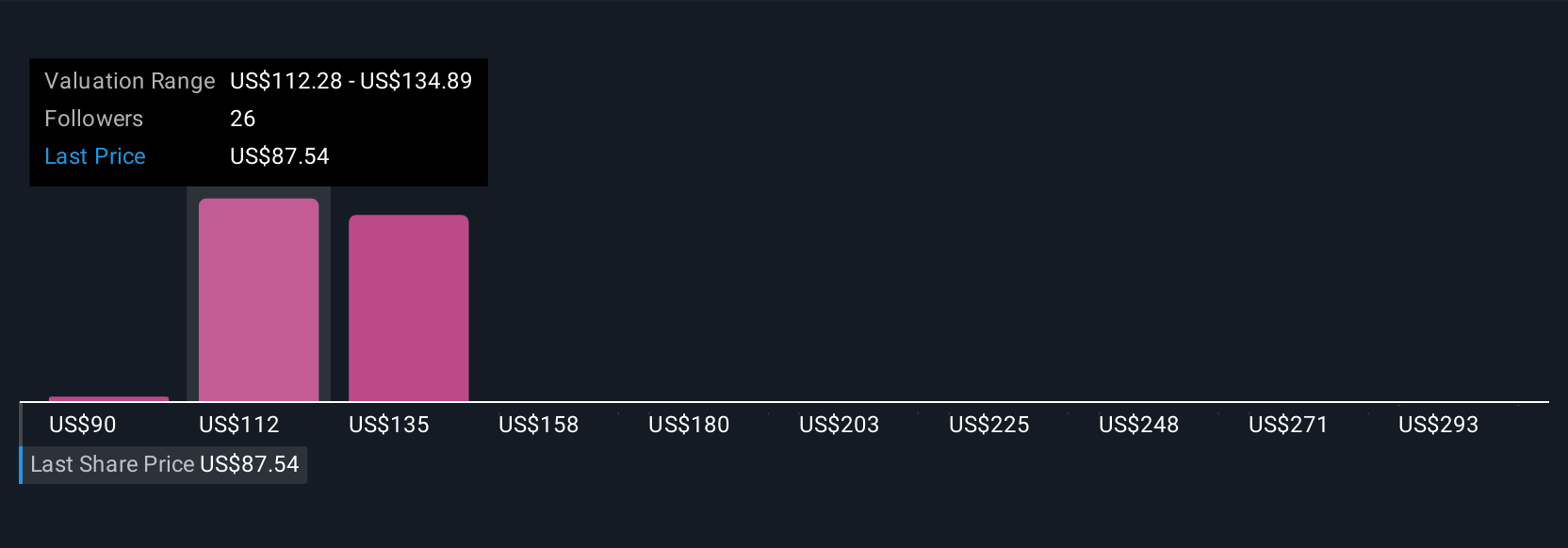

Six members of the Simply Wall St Community currently see Elastic's fair value at between US$89.66 and US$140.57, highlighting the wide range of expectations. Setting these views against the risk of hyperscalers eroding Elastic's market share highlights why different investors may come to very different conclusions about the company's long-term performance.

Check out 6 other fair value estimates for Elastic – why this stock is only worth $89.66!

Build your own resilient story

Don't agree with an existing story? Create your own in under 3 minutes. Following the herd rarely yields exceptional investment returns.

Is there a chance for Elastic?

First movers are already taking notice. Check out the stocks they are targeting before they leave the shed.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

Evaluation is complex, but we will simplify it here.

Discover whether Elastic is undervalued or overvalued with our in-depth analysis. Fair value estimates, potential risks, dividends, insider transactions, and financial condition.

Access free analysis

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.