Dr. Rob Leclerc is a founding partner of AgFunder, a venture capital firm and parent company of AgFunderNews.

I’m currently reading Andrew Ross Sorkin’s new book. 1929which traces the people at the center of the pre-Great Depression market crash that lasted from 1929 to 1933. The Dow Jones Industrial Average fell 89% from a high of 381 in September 1929 to 41 in July 1932. In today’s terms, this is like returning the Dow to its 1996 levels.

Mr. Sorkin draws subtle parallels to today, including tariffs, a long bull market, and excessive speculation under Smoot-Hawley.

But the differences are just as important.

First, leverage. In 1929, margin debt amounted to about 9% of GDP, allowing investors to buy stocks even if they were down only 10-20%. Margin debt now stands at about $1 trillion, or about 3% of GDP, and most investors have to put down more than 50%. Credit debt is up from $700 billion a year ago, but relative to market size it is near the lowest level since 2005.

Second is policy response. In the late 1920s, the Federal Reserve did not intervene, and President Hoover resisted intervention. Without the FDIC, when banks started failing in 1930, deposits disappeared and panic spread. After the market crash of 1929, the economy began to stabilize, but a banking panic turned the financial collapse into a decade-long depression.

Given that context, today’s market correction is unlikely to mirror the 1929 collapse. Still, many investors are nervous about the AI boom, worried it could end like the railroad mania of the 1800s or the telecom bubble of the 1990s.

Two questions determine when the bubble bursts:

Are you facing GPU overcapacity? Probably not. We hear about overcapacity in railways and fiber optics, but not about electrification. AI is more like energy than transportation or communications, and the demand for intelligence is limited only by cost, not practicality. Even if the increase in intelligence from large-scale models reaches a plateau, we will likely move to long-term runs of parallel AI that brute-forces its way through the solution space (the universe of possible answers that the AI can search).

Taking advantage of this, many people are beginning to realize that what AI lacks is not intelligence. It’s an agency. I think agencies will need far more computing than intelligence.

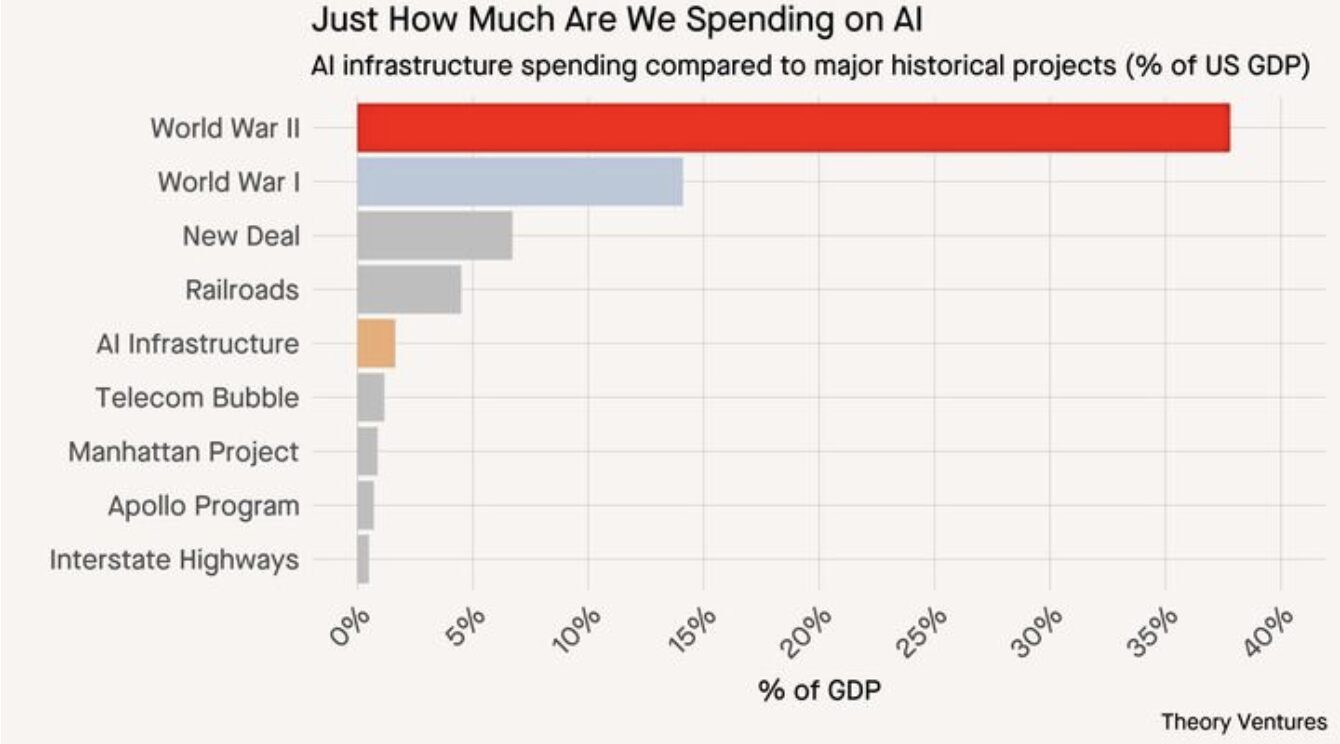

How much capital can flow into data centers? Spending on AI infrastructure currently represents approximately 1.3% of U.S. GDP. Approximately $350 billion annually. Although it sounds huge, it is small compared to other industrial buildings. Railways amounted to 6-7% of GDP in the late 19th century. Mobilization for World War II reached over 40%. Even the highway programs of the 1950s had mileage rates of 3 to 4 percent. If rail is the benchmark for commercial endeavors, AI capital spending could increase five times before hitting a ceiling.

But here’s the deeper point. This is not just a speculative boom for profit. It is also a race for national security. Just as the expansion of railways and communications was driven by greed, the AI boom is also driven by fear. If the West were to lose technological leadership to China, the consequences would be not just economic, but existential as well.

The US government knows this. That’s why we’re subsidizing AI chips, restricting exports, rapidly expanding the grid, and secretly linking commercial computing and defense infrastructure. If necessary, it would lower interest rates to negative, if not directly as a backstop, in order to direct as much money into this as possible.

The stakes are similar to periods of mobilization like the New Deal or World War II, moments when the allocation of capital coincided with the survival of the nation.

Yes, we are in the midst of a boom, but nothing fundamental has happened yet. Data center proliferation has not gone parabolic yet, but when it does, it could be driven by policy as well as profits.