International Business Machines (IBM) stock is reacting to two competing storylines. Starbucks is moving to replace IBM’s maintenance tools with in-house AI software, while IBM is rolling out new AI-focused products like Lightwell and an upgraded IBM Bob.

Check out our latest analysis for International Business Machines.

Over the past quarter, International Business Machines’ 90-day price-to-earnings ratio was 27.97% and one-year total shareholder return was 5.37%. This suggests that recent momentum is in contrast to a long period of gradual gains.

The stock’s recent reaction, including a one-day price decline of 2.23% and a 30-day stock return of 6.42%, reflects investors weighing the risks of moving customers in-house, like Starbucks, against the risks of IBM’s AI-focused launches, such as the Bob upgrade and Lightwell rollout.

If IBM’s AI push has you thinking about other areas where AI is reshaping software, now’s a good time to take a look at these 63 AI stocks that aren’t just burning cash, but are also profitable.

While it’s clear that International Business Machines is undertaking extensive AI and mainframe modernization efforts, the stock’s sharp 90-day move and current price, which is slightly above the latest analyst targets, begs a simpler question. Is that strength already factored into the valuation?

Most popular story: 15.3% overrated

The most followed article on International Business Machines puts the stock’s fair value at $256.08 compared to the recent share price of $295.30, and believes the current stock price increase is based on certain earnings, margins, and multiple assumptions, but that it exceeds expectations.

IBM represents an investment in defensive growth technology and is transitioning into a software and AI-driven enterprise platform company. Although top-line growth remains modest, the improving mix (software), high margins, and durable cash flows support an attractive long-term investment case, especially for investors seeking exposure to enterprise AI with less volatility than pure SaaS competitors.

Read the whole story.

Want to know how the fair value numbers are constructed? Kapirey says the story depends heavily on the software mix, the strength of cash generation, and future revenue multiples assuming IBM continues to transition into a high-margin business.

Result: Fair value $256.08 (overvalued)

Read the full explanation to understand what’s behind the predictions.

However, International Business Machines still faces two obvious variables. One is slower-than-expected adoption of AI across software and consulting franchises, and the other is the pressure from large customers like Starbucks accelerating internal replacement.

Find out about the key risks to this International Business Machines story.

Another look: SWS DCF fair value of overseas office equipment

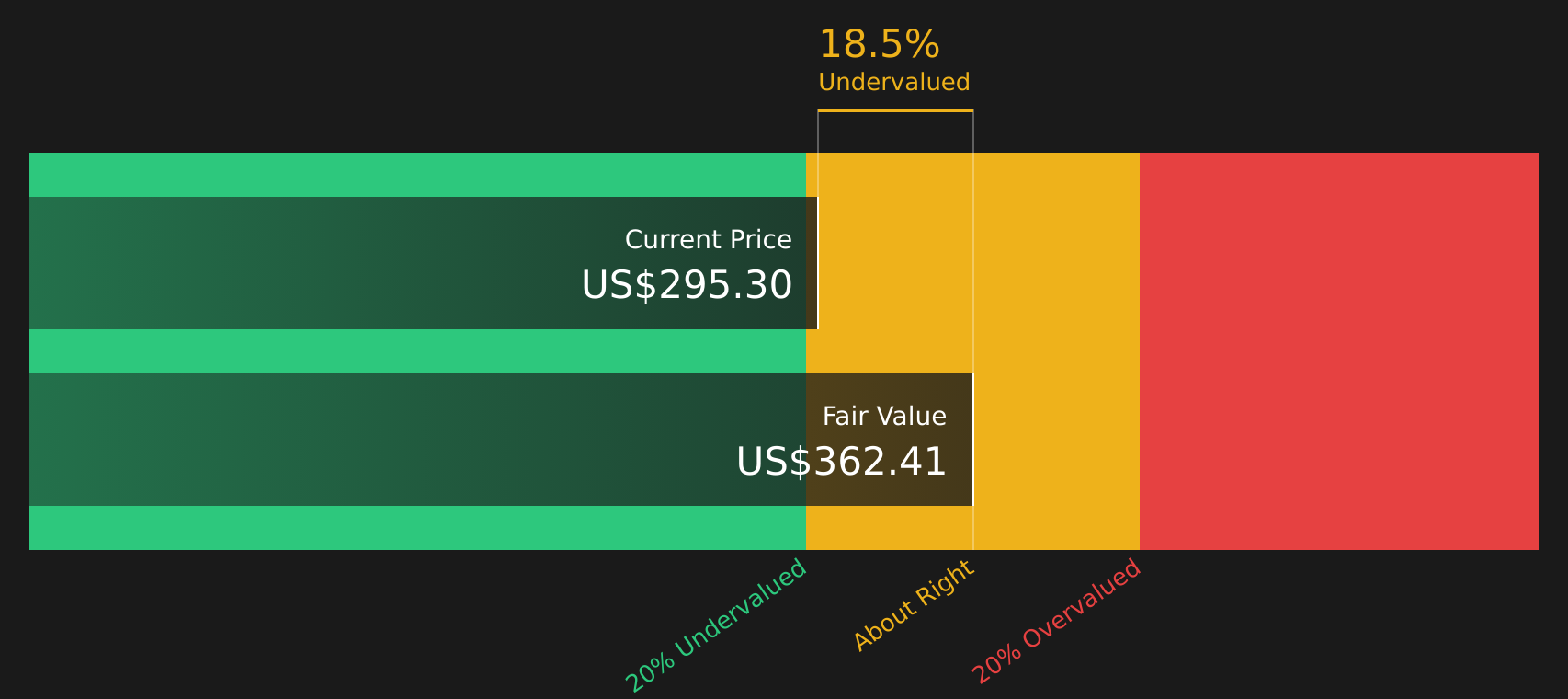

While our users believe that International Business Machines is overvalued by 15.3% at a fair value of $295.30 versus a fair value of $256.08, our DCF model shows the opposite, with a fair value of $362.41 and the stock trading at an 18.5% discount. Two thoughtful models, two very different answers. Which assumption do you trust more?

Find out how the SWS DCF model arrives at fair value.

Simply Wall St runs discounted cash flows (DCF) on every stock in the world every day (check out International Business Machines for example). The entire calculation is fully illustrated. Track your results with a watchlist or portfolio and get alerts when they change, or use our stock screener to discover 44 high-quality undervalued stocks. When you save your screener, you’ll also get alerts when new companies match, so you never miss out on potential opportunities.

next step

Since International Business Machines sits between clear risks and real rewards, now’s a good time to see the details for yourself, decide what’s most important to your portfolio, and weigh those trade-offs against 4 key rewards and 1 important warning sign.

Looking for investment ideas other than International Business Machines?

If IBM is focused on what’s next in your portfolio, don’t stop here. A good list of fresh ideas is equally important.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

new: AI stock screener and alerts

Our new AI Stock Screener scans the market for opportunities every day.

• Dividend powerhouse (yield 3% or more)

• Small-cap stocks that are undervalued due to insider purchases.

• High-growth technology and AI companies

Or build your own metrics from over 50 metrics.

Explore for free now

Do you have feedback on this article? Interested in its content? Please contact us directly. Alternatively, email editorial-team@simplywallst.com.