Europe Artificial Intelligence in Robotics Market Size

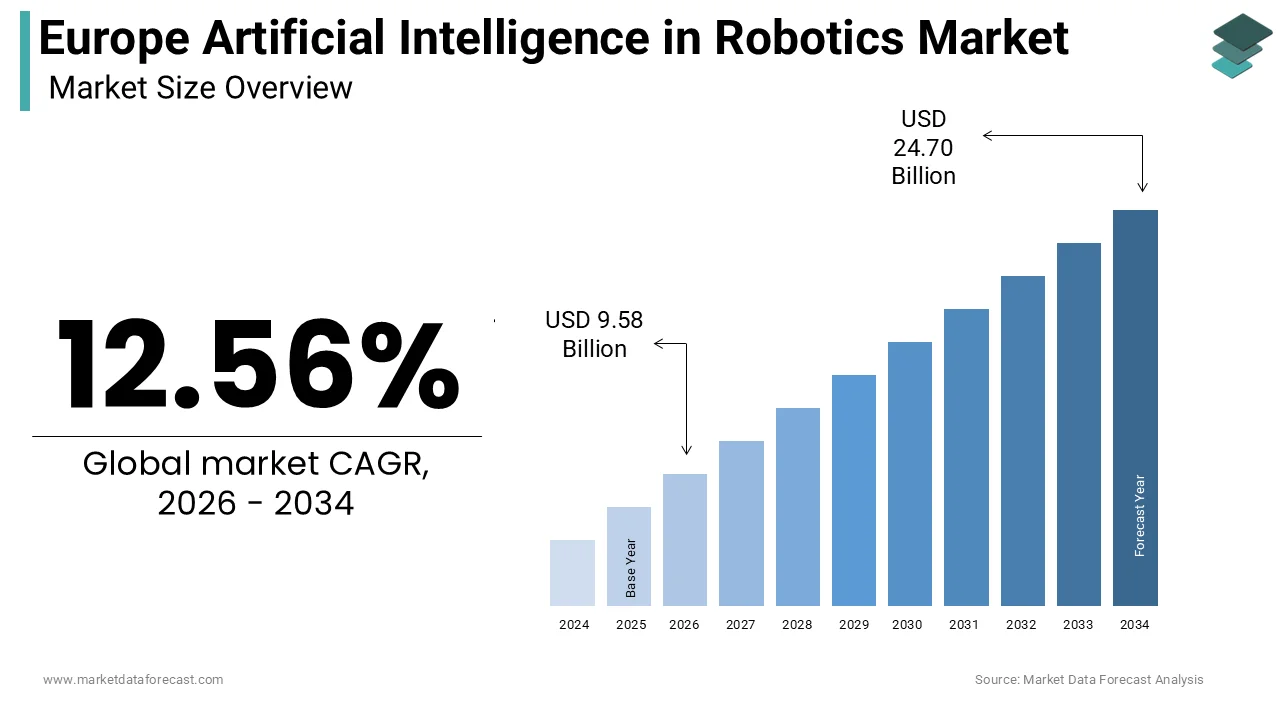

The Europe artificial intelligence in robotics market size was calculated to be USD 8.51 billion in 2025 and is anticipated to be worth USD 24.70 billion by 2034, from USD 9.58 billion in 2026, growing at a CAGR of 12.56% during the forecast period.

The artificial intelligence in robotics is advanced machine learning algorithms with autonomous mechanical systems designed to perform complex tasks with minimal human intervention. This sector encompasses industrial collaborative robots, service robots for healthcare and logistics, and autonomous mobile robots utilized in warehousing and agriculture. The integration of artificial intelligence enables these systems to perceive their environment, make real-time decisions, and adapt to dynamic conditions, thereby enhancing operational efficiency and safety. Furthermore, the European Commission reported that the adoption of robotics in manufacturing has increased productivity by up to 30% in sectors such as automotive and electronics. The region is also witnessing a surge in research and development initiatives supported by programs like Horizon Europe, which allocated over 95 billion Euros for innovation between 2021 and 2027. The emphasis on ethical AI and data privacy under the General Data Protection Regulation further shapes the development and deployment of these technologies, ensuring responsible innovation.

MARKET DRIVERS

Labor Shortages and Demographic Shifts Drive Automation Demand

The persistent labor shortage, exacerbated by demographic changes and shifting workforce preference,s is the primary factor fuelling the growth of Europe’s artificial intelligence in robotics market. Many European countries face a shrinking working-age population, leading to significant gaps in sectors such as manufacturing, healthcare, and logistics. According to Eurostat, the old age dependency ratio in the European Union is projected to reach 54% by 20,50 indicating a substantial increase in the number of retirees relative to workers. This demographic shift creates an urgent need for automation to sustain economic output and provide essential services. In the manufacturing sector, companies are increasingly deploying collaborative robots equipped with AI to assist human workers and fill labor gaps. As per the International Federation of Robotics, the density of industrial robots in Europe reached 115 units per 10000 employees in 2022, with Germany and Sweden leading the adoption rates. The healthcare sector is also turning to AI-powered robots for patient care and administrative tasks to alleviate pressure on staff. For instance, service robots are being used in hospitals in France and Italy to deliver medications and monitor patients. The ability of AI-enabled robots to operate continuously without fatigue makes them an attractive solution for addressing labor constraints. Furthermore, the rise of remote work and changing job expectations has reduced the availability of workers for repetitive or physically demanding roles.

Government Initiatives and Strategic Investments in Industry 4.0 Accelerate Adoption

The strong support from European governments and institutions for Industry 4.0 initiatives is additionally leveraging the growth of Europe’s artificial intelligence in the robotics market. The European Union has prioritized digital sovereignty and technological leadership through strategies, such as the Digital Decade Policy Programme, which aims to ensure that 75% of EU companies use cloud computing, big data, and artificial intelligence by 2030. According to the European Commission, over 20 billion Euros have been invested in digital infrastructure and innovation projects under the Recovery and Resilience Facility. These funds are often directed towards modernizing industrial facilities and adopting advanced automation technologies. Countries like Germany have launched specific programs such as the High Tech Strategy 2025, which emphasizes the development of autonomous systems and AI applications in production. Similarly, the French government’s France 2030 plan includes substantial investments in deep tech and robotics startups. These initiatives create a favorable ecosystem for technology providers and end users by reducing financial barriers and encouraging collaboration between academia and industry. The standardization efforts led by the European Committee for Standardization also facilitate the interoperability of robotic systems, enhancing their appeal to manufacturers.

MARKET RESTRAINTS

High Implementation Costs and Complex Integration Processes Restrain Market Growth

The high cost of implementation and the complexity associated with integrating these advanced systems into existing operational frameworks are hampering the growth of Europe’s artificial intelligence in the robotics market. AI-enabled robots require significant capital expenditure for hardware, software licenses, and specialized infrastructure. The total cost of ownership includes not only the initial purchase but also ongoing maintenance, updates, and training for staff. Additionally, integrating AI robotics with legacy machinery and information technology systems often requires custom engineering solutions, which can be time-consuming and costly. The lack of standardized interfaces and protocols further complicates the integration process, leading to potential compatibility issues. In countries like Italy and Spain, where the industrial base consists largely of smaller firms, the financial burden of transitioning to smart robotics is particularly prohibitive. The return on investment may take several years to materialize, discouraging risk-averse businesses from making the switch.

Regulatory Uncertainty and Ethical Concerns Regarding AI Deployment Create Compliance Burdens

The regulatory environment, due to its complexity and evolving nature, is also impeding the growth of Europe’s artificial intelligence in the robotics market. The European Union’s Artificial Intelligence Act introduces strict requirements for high-risk AI applications, including those used in robotics, such as healthcare and transportation. According to the European Parliament, compliance with these regulations requires rigorous testing, documentation, and transparency measures, which can delay product launches and increase development costs. Companies must ensure that their robots do not inadvertently capture or misuse personal data, which requires sophisticated data management solutions. Additionally, ethical concerns regarding job displacement and algorithmic bias create societal resistance to widespread adoption. The lack of clear liability frameworks for accidents involving autonomous robots also creates legal uncertainty for manufacturers and users. These regulatory and ethical challenges require companies to invest heavily in compliance and risk management, potentially slowing down innovation and market expansion.

MARKET OPPORTUNITIES

Growing demand for elderly care and medical assistance drives the development of AI-powered robotic solutions in the healthcare sector.

The expansion of healthcare and assistive robotics, driven by the increasing need for efficient and compassionate care services, is creating new opportunities for the growth of Europe’s artificial intelligence in robotics market. With an aging population, the demand for long-term care and medical assistance is rising sharply, creating a gap that AI-enabled robots can help fill. According to the World Health Organization, the number of people aged 60 years and older in Europe is expected to double by 2050, necessitating innovative care solutions. AI-powered robots can assist with patient monitoring, medication delivery, and physical therapy, reducing the burden on healthcare professionals. As per the European Innovation Partnership on Active and Healthy Ageing, several pilot projects in countries like Denmark and the Netherlands have demonstrated the effectiveness of social robots in improving the quality of life for elderly individuals. These robots can provide companionship, cognitive stimulation, and emergency alerts, enhancing patient safety and well-being. Furthermore, surgical robots equipped with AI algorithms are enabling minimally invasive procedures with higher precision and faster recovery times. The European Medicines Agency has approved several robotic-assisted surgical systems reflecting the growing acceptance of these technologies in clinical settings. Government funding for health technology innovation further supports this trend.

Advancements in Autonomous Mobile Robots for Logistics and Warehousing Create New Avenues

The advancements in autonomous mobile robots for logistics and warehousing are also contributing to creating new opportunities for the expansion of Europe’s artificial intelligence in the robotics market. The rapid growth of e-commerce has increased the demand for faster and more accurate order fulfillment, prompting companies to automate their distribution centers. According to Eurostat, e-commerce sales in the European Union grew by 14% in 2023, highlighting the pressure on logistics providers to optimize operations. AI-enabled autonomous mobile robots can navigate warehouses, dynamically pick and pack items, and collaborate with human workers to enhance productivity. As per the International Federation of Robotics, the sales of service robots for logistics have increased by over 20% annually in recent years. Major retailers and third-party logistics providers in countries like Germany and the United Kingdom are investing heavily in automated warehouses to meet customer expectations. These robots utilize computer vision and machine learning to optimize routes and avoid obstacles, ensuring efficient material handling. The flexibility of autonomous mobile robots allows for scalable solutions that can adapt to fluctuating demand patterns. Furthermore, the integration of these robots with warehouse management systems provides real-time visibility and data analytics for better decision-making. Government initiatives supporting smart logistics infrastructure also contribute to this trend.

MARKET CHALLENGES

Cybersecurity Vulnerabilities and Data Breaches Pose Significant Risks

The cybersecurity vulnerabilities, as these systems become increasingly connected and reliant on data exchange, are acting as a major barrier to the growth of Europe’s artificial intelligence in the robotics market. AI-enabled robots often operate within networked environments, making them susceptible to hacking, malware, and ransomware attacks. According to the European Union Agency for Cybersecurity, the number of cyber incidents involving Internet of Things devices, including robots, has risen significantly in recent years. A successful attack can disrupt operations, cause physical damage, or steal proprietary data, leading to severe financial and reputational consequences. As per a report by the European Defence Agency, state-sponsored actors have targeted critical infrastructure, including automated manufacturing facilities, highlighting the national security implications. The complexity of AI algorithms also makes it difficult to detect and mitigate subtle manipulations known as adversarial attacks. Manufacturers face the challenge of implementing robust security measures without compromising performance or usability. The lack of standardized cybersecurity protocols for robotics further exacerbates the problem. Users may hesitate to adopt advanced robotic systems due to fears of security breaches. Addressing these risks requires continuous investment in encryption, authentication, and intrusion detection systems.

Interoperability Issues and Lack of Standardization Hinder Seamless Integration

The lack of interoperability and standardized communication protocols also inhibits the growth of Europe’s artificial intelligence in the robotics market. Robotic systems from different manufacturers often use proprietary software and hardware interfaces, making it difficult to integrate them into a cohesive operational ecosystem. According to the European Committee for Standardization, efforts to harmonize technical standards are ongoing, but progress is slow due to the rapid pace of technological change. As per the Industrial Internet Consortium, incompatible data formats and communication languages hinder the seamless exchange of information between robots and enterprise resource planning systems. This fragmentation forces companies to rely on single vendors or invest in costly custom integration solutions, limiting flexibility and increasing dependency. In large industrial settings where multiple types of robots are used, the inability to coordinate their actions efficiently reduces overall productivity. The absence of universal standards also complicates maintenance and upgrades, as components may not be interchangeable. Small and medium-sized enterprises are particularly affected as they lack the resources to manage complex multi-vendor environments. The European Union has recognized this issue and is promoting open standards through initiatives like the Digital Single Market, but widespread adoption remains a challenge.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

12.56% |

|

Segments Covered |

By Component, Robot Type, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

ABB Ltd., KUKA AG, Siemens AG, Bosch Rexroth AG, FANUC Europe Corporation, YASKAWA Europe GmbH, Universal Robots, Comau S.p.A., Stäubli International AG, Blue Danube Robotics |

SEGMENTAL ANALYSIS

By Component Insights

The hardware segment accounted in holding 55.4% of the Europe artificial intelligence in robotics market share in 2025, with the high cost associated with manufacturing and procuring the physical components of robotic systems, such as precision actuators, advanced sensors, microprocessors, and structural materials. According to the International Federation of Robotics, the average cost of an industrial robot unit in Europe ranges from 20000 to 50000 Euros, depending on payload and complexity, which constitutes a significant portion of initial deployment budgets. The integration of AI requires specialized hardware such as graphics processing units and neural processing units, which are expensive to produce and source. As per Eurostat, the manufacturing sector in the European Union invested over 150 billion Euros in machinery and equipment in 2023, with a growing share allocated to smart robotics. The durability and longevity of hardware components also mean that replacement cycles are longer, but the initial outlay remains high. Furthermore, the demand for collaborative robots equipped with force torque sensors and safety cameras has increased the bill of materials for each unit. Governments and private entities are investing heavily in upgrading factory floors with these physical assets to achieve automation goals.

The software segment is projected to witness the fastest CAGR of 18.5% from 2026 to 2034, owing to the role of software in enabling intelligence perception and decision-making capabilities in robots. Unlike hardware, which is a one-time purchase, software often involves recurring licensing fees, updates, and cloud services, creating a sustainable revenue stream. According to the European Commission, the adoption of artificial intelligence software in enterprises has grown by 25% annually as companies seek to enhance the autonomy of their robotic fleets. Advanced machine learning algorithms, computer vision systems, and natural language processing modules require continuous development and refinement, driving up software value. The rise of Robot as a Service models allows companies to access sophisticated AI capabilities without heavy upfront hardware costs, further boosting software adoption. Additionally, the need for seamless integration with enterprise resource planning and manufacturing execution systems necessitates robust middleware and application programming interfaces.

By Robot Type Insights

The industrial robots segment was expected to hold a significant share of the Europe artificial intelligence in robotics market in 2025, with the long-standing tradition of manufacturing excellence in Europe, particularly in the automotive and electronics industries, which rely heavily on automated assembly lines. According to the International Federation of Robotics, Europe installed over 60000 new industrial robots in 2022. AI-enabled industrial robots are used for tasks such as welding, painting, material handling, and quality inspection, where precision and speed are paramount. The integration of artificial intelligence allows these robots to adapt to variations in parts and perform complex tasks with minimal human intervention. As per the European Automobile Manufacturers Association, the automotive industry continues to be the largest user of industrial robots, driven by the transition to electric vehicle production, which requires new manufacturing processes. The push for Industry 4.0 has further accelerated the adoption of collaborative industrial robots that can work safely alongside humans. Government incentives for modernizing manufacturing infrastructure and improving productivity also support this segment.

The service robots segment is anticipated to witness the fastest CAGR of 22.3% over the next five years, with the diversification of robotic applications beyond manufacturing into areas such as healthcare, delivery warehouse logistics, and customer service. According to the International Federation of Robotics, sales of professional service robots in Europe increased by 35% in 2023, reflecting strong demand in non-industrial settings. In the healthcare sector, AI-powered robots are increasingly used for patient monitoring, rehabilitation, and surgical assistance, addressing labor shortages and improving care quality. As per the European Health Telematics Observatory, the adoption of assistive robots in hospitals and care homes is accelerating due to the aging population and the need for efficient resource management. In logistics, autonomous, mobile robots are transforming warehousing operations by optimizing picking and packing processes. The hospitality industry is also adopting service robots for cleaning and concierge tasks to enhance guest experiences. The flexibility and adaptability of AI-enabled service robots allow them to operate in dynamic and unstructured environments. Government funding for health tech and smart logistics initiatives further supports this expansion.

By Application Insights

The manufacturing and assembly segment was the largest by holding 50.3% of the Europe artificial intelligence in robotics market share in 2025, with the imperative for manufacturers to enhance productivity, reduce waste, and maintain high quality standards in competitive global markets. AI-enabled robots in manufacturing can perform complex assembly tasks with micron-level precision, adapting to real-time changes in production parameters. The automotive industry in countries like Germany, France, and Italy extensively utilizes AI robotics for welding, painting, and final assembly. As per the International Federation of Robotics, the density of robots in the European automotive industry is among the highest globally, with over 1000 robots per 10000 employees. The shift towards customized production and small batch sizes requires flexible automation solutions that AI robotics can provide. Collaborative robots are increasingly deployed to work alongside human workers, enhancing ergonomics and efficiency. Government initiatives such as the German High-Tech Strategy promote the digitalization of manufacturing, further driving adoption. The proven ability of AI robotics to reduce cycle times and improve product consistency ensures that manufacturing remains the primary application area for these technologies in Europe.

The healthcare and surgery segment is expected to grow at the fastest CAGR of 24.5% from 2026 to 2034, with the increasing adoption of robotic-assisted surgical systems and AI-powered diagnostic tools that improve patient outcomes and reduce recovery times. According to the European Society of Medical Oncology, the use of robotic surgery has increased by 20% annually in major European hospitals due to its precision and minimally invasive nature. AI algorithms enable surgeons to plan procedures more accurately and execute them with greater control, reducing complications. As per the World Health Organization the aging population in Europe is driving demand for assisted care robots that help with mobility, medication management, and monitoring. Countries like Sweden and Denmark are pioneering the use of social robots in elderly care facilities to address staff shortages. The European Medicines Agency has streamlined approval processes for innovative medical devices, facilitating faster market entry for robotic solutions. Government investments in digital health infrastructure and telemedicine further support this trend. The ability of AI robotics to enhance the quality of care while reducing the burden on healthcare professionals ensures that this segment grows at an exceptional rate.

REGIONAL ANALYSIS

Germany Artificial Intelligence in Robotics Market Analysis

Germany was the largest contributor in the Europe artificial intelligence in robotics market by capturing 32.1% of the share in 2025 with its status as the industrial powerhouse of the continent. The country is home to major automotive and machinery manufacturers who are early adopters of AI-enabled robotics to maintain competitiveness. According to the German Federal Ministry for Economic Affairs and Climate Action, the government has invested billions in the High Tech Strategy 2025, which prioritizes AI and robotics research. The presence of leading robotics companies such as KUKA and Siemens fosters a vibrant ecosystem of innovation and supply chain integration. As per the International Federation of Robotics, Germany consistently ranks as the largest market for industrial robots in Europe, with high installation rates in the automotive and electronics sectors. The Fraunhofer Society conducts cutting-edge research in cognitive robotics, bridging the gap between academic advancements and industrial applications. Strong vocational training programs ensure a skilled workforce capable of operating and maintaining advanced robotic systems. Government subsidies for small and medium-sized enterprises to adopt automation technologies further stimulate market growth.

United Kingdom Artificial Intelligence in Robotics Market Analysis

The United Kingdom artificial intelligence in robotics market was positioned next, holding 14.3% of the share in 2025. The UK is a leader in the development of service robots, particularly for medical applications such as surgical assistants and care bots. The National Health Service is increasingly exploring robotic solutions to improve efficiency and patient care, driving demand in the healthcare sector. As per the Centre for Process Innovation, the UK has a growing cluster of robotics companies specializing in agri-tech and logistics automation. The presence of world-class universities such as Oxford and Cambridge fosters innovation in AI algorithms and machine learning. The post Brexit regulatory environment has encouraged the development of domestic technology standards promoting local innovation. The logistics sector in the UK is rapidly adopting autonomous mobile robots to handle e-commerce demands. Government support for digital transformation and smart infrastructure projects further boosts market growth.

France Artificial Intelligence in Robotics Market Analysis

France’s artificial intelligence in the robotics market growth is majorly driven by the active government support for technological sovereignty and innovation. The French government’s France 2030 investment plan includes significant allocations for deep tech and robotics, aiming to double the production of industrial robots by 2030. Companies like Airbus and Renault are integrating collaborative robots into their production lines to enhance flexibility. As per the French National Research Institute for Digital Science and Technology, several research hubs are dedicated to advancing AI in robotics, fostering collaboration between academia and industry. The healthcare sector is also a key growth area with French startups developing innovative surgical and rehabilitation robots. Government grants and tax credits for research and development encourage companies to invest in advanced technologies.

Italy Artificial Intelligence in Robotics Market Analysis

Italy’s artificial intelligence in the robotics market growth is likely to grow with its diverse manufacturing base, particularly in machinery, automotive, and food processing. The country has a large number of small and medium-sized enterprises that are increasingly adopting collaborative robots to improve productivity and address labor shortages. The Made in Italy brand benefits from the precision and quality enabled by AI-driven automation. As per the Italian Robotics and Automation Association, the market for service robots is also expanding, particularly in agriculture and tourism. Government incentives such as Industry 4.0 tax credits encourage businesses to upgrade their equipment with smart technologies. The presence of research centers like the Italian Institute of Technology contributes to advancements in humanoid and soft robotics.

Sweden Artificial Intelligence in Robotics Market Analysis

Sweden’s artificial intelligence in the robotics market growth is propelled by its high level of digitalization and commitment to sustainability. Companies like ABB have a strong presence in Sweden, contributing to the industrial robotics sector. As per the Swedish Innovation Agency, Vinnova, significant funding is provided for research in human-robot interaction and autonomous systems. The healthcare sector in Sweden is actively piloting AI robots for elderly care and rehabilitation, addressing demographic challenges. The strong educational system produces a steady stream of skilled engineers and data scientists. The emphasis on green technology drives the development of energy-efficient robotic solutions. Sweden’s collaborative approach between public and private sectors fosters a conducive environment for innovation.

COMPETITION OVERVIEW

The competition in the Europe artificial intelligence in robotics market is characterized by intense rivalry among established industrial giants and agile startups vying for leadership in smart automation. Leading companies leverage their extensive research and development capabilities and broad product portfolios to maintain dominance, while niche players differentiate themselves through specialized AI algorithms and innovative applications. Price competition is moderate in the high-end segment, where performance and reliability are prioritized, but remains fierce in the entry-level sector. Strategic alliances with technology providers and system integrators are crucial for delivering comprehensive solutions that meet diverse industry needs. Companies compete on the basis of software sophistication, ease of use, and integration capabilities with existing enterprise systems. The threat of new entrants is moderate due to high barriers related to technical expertise and capital requirements.

KEY MARKET PLAYERS

A few major players of the Europe market include

- ABB Ltd

- KUKA AG

- Siemens AG

- Bosch Rexroth AG

- FANUC Europe Corporation

- YASKAWA Europe GmbH

- Universal Robots

- Comau S.p.A

- Stäubli International AG

- Blue Danube Robotics

Top Strategies Used by Key Market Participants

Key players in the Europe artificial intelligence in robotics market primarily employ strategies focused on strategic partnerships and ecosystem development to enhance technological capabilities. Companies are increasingly collaborating with software firms and academic institutions to integrate advanced machine learning algorithms into their robotic platforms. This approach accelerates innovation and ensures compatibility with emerging industry standards. Manufacturers are also investing heavily in research and development to create autonomous systems capable of complex decision-making. Product differentiation through specialized applications in healthcare logistics and manufacturing is a common tactic to capture niche markets. Additionally, firms are expanding their service offerings by providing comprehensive training and support programs to address the skills gap. Digital transformation initiatives such as cloud-based monitoring and predictive maintenance services are being prioritized to create recurring revenue streams.

Leading Players in the Market

- ABB Ltd is a global technology leader headquartered in Switzerland with a dominant presence in the Europe artificial intelligence in robotics market. The company specializes in industrial automation and robotics, offering advanced solutions that integrate AI for enhanced precision and efficiency. ABB has recently strengthened its position by launching new collaborative robots equipped with machine learning capabilities that adapt to dynamic environments. They have expanded their digital ecosystem through the ABB Ability platform, enabling seamless connectivity and data analytics for predictive maintenance. Their commitment to sustainability drives the development of energy-efficient robotic systems. This holistic approach ensures they remain at the forefront of technological advancement, providing robust and intelligent automation tools that empower industries across Europe to achieve higher productivity and operational excellence.

- KUKA AG, a German robotics manufacturer, is a key player in the Europe artificial intelligence in robotics market, known for its innovative industrial and service robots. Owned by Midea Group, KUKA leverages global resources while maintaining strong European roots. The company has recently focused on integrating AI into its robot controllers to enable easier programming and adaptive task execution. They have introduced new lightweight robots designed for flexible assembly lines in the automotive and electronics sectors. KUKA actively collaborates with academic institutions to advance research in human-robot interaction and cognitive robotics. Their expansion into the healthcare and logistics sectors demonstrates versatility beyond traditional manufacturing. Their continuous investment in digital twins and simulation software allows customers to optimize processes before deployment. This strategic focus on intelligence and flexibility solidifies KUKA’s reputation as a pioneer in delivering smart automation solutions that drive industrial transformation across the continent.

- Siemens AG is a powerhouse in the Europe artificial intelligence in robotics market leveraging its expertise in industrial digitalization and automation. The company provides comprehensive solutions that combine hardware with powerful software platforms like Siemens Xcelerator. Siemens has recently strengthened its market position by enhancing its AI-driven analytics tools for real-time decision-making in robotic operations. They have partnered with leading tech firms to develop edge computing capabilities that reduce latency in robotic control systems. Their focus on open ecosystems encourages interoperability among different robotic brands and enterprise systems. Siemens actively promotes the adoption of digital twins, allowing manufacturers to simulate and optimize robotic workflows virtually. Their strong presence in critical infrastructure and heavy industry ensures widespread implementation of their technologies. This integrated approach enables Siemens to deliver scalable and intelligent robotic solutions that enhance efficiency and resilience for diverse industrial applications throughout Europe.

MARKET SEGMENTATION

This research report on the European artificial intelligence in robotics market has been segmented and sub-segmented based on component, robot type, application & region.

By Component

By Robot Type

- Industrial Robots

- Service Robots

- Others

By Application

- Manufacturing and Assembly

- Logistics and Warehousing

- Healthcare and Surgery

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe