After the market closes tomorrow, NVIDIA will announce its fiscal 2026 fourth quarter financial results. This report goes far beyond standard financial results and will serve as an important reference point for semiconductor markets, institutional investors, and participants in the AI sector.

Nvidia is no longer just a chipmaker. The company is a barometer for the entire technology space, with its results reflecting the demand for AI in data centers, hyperscaler spending, and the pace of adoption of new generation GPUs like Blackwell and H200. This report will show whether demand for Nvidia’s products is based on stable long-term contracts, or whether the market is overestimating expectations for AI.

Why this report matters

Nvidia’s weight and index in the market

Nvidia has the largest weight in the S&P 500 technology sector and is an important component of the Dow Jones Industrial Average. Its stock price has a significant impact on market-tracking indexes and ETFs. The market’s reaction to NVDA’s results this quarter could determine the overall direction of the semiconductor sector and the sentiment of the technology index.

Hyperscaler Spend Test

Amazon, Google, Microsoft, and Meta continue to increase spending on data centers and AI infrastructure. Nvidia is the main beneficiary of these investments, and the report will show whether GPU revenue growth is truly being driven by sustainable demand or just one-off orders in an AI hype environment. The pace of hyperscalers’ spending will be a barometer of how strongly these companies believe in AI’s long-term potential.

Blackwell and H200

Newer GPU generations such as Blackwell and H200 are being watched closely by investors. These adoptions by enterprise customers, including China, will show whether Nvidia can maintain its technological edge and gain market share in the growing AI space. The report also examines the “AI 2026 peak” narrative. GPU revenue growth has been impressive in recent years, but the question remains whether AI will continue to be a sustainable growth driver.

market expectations

-

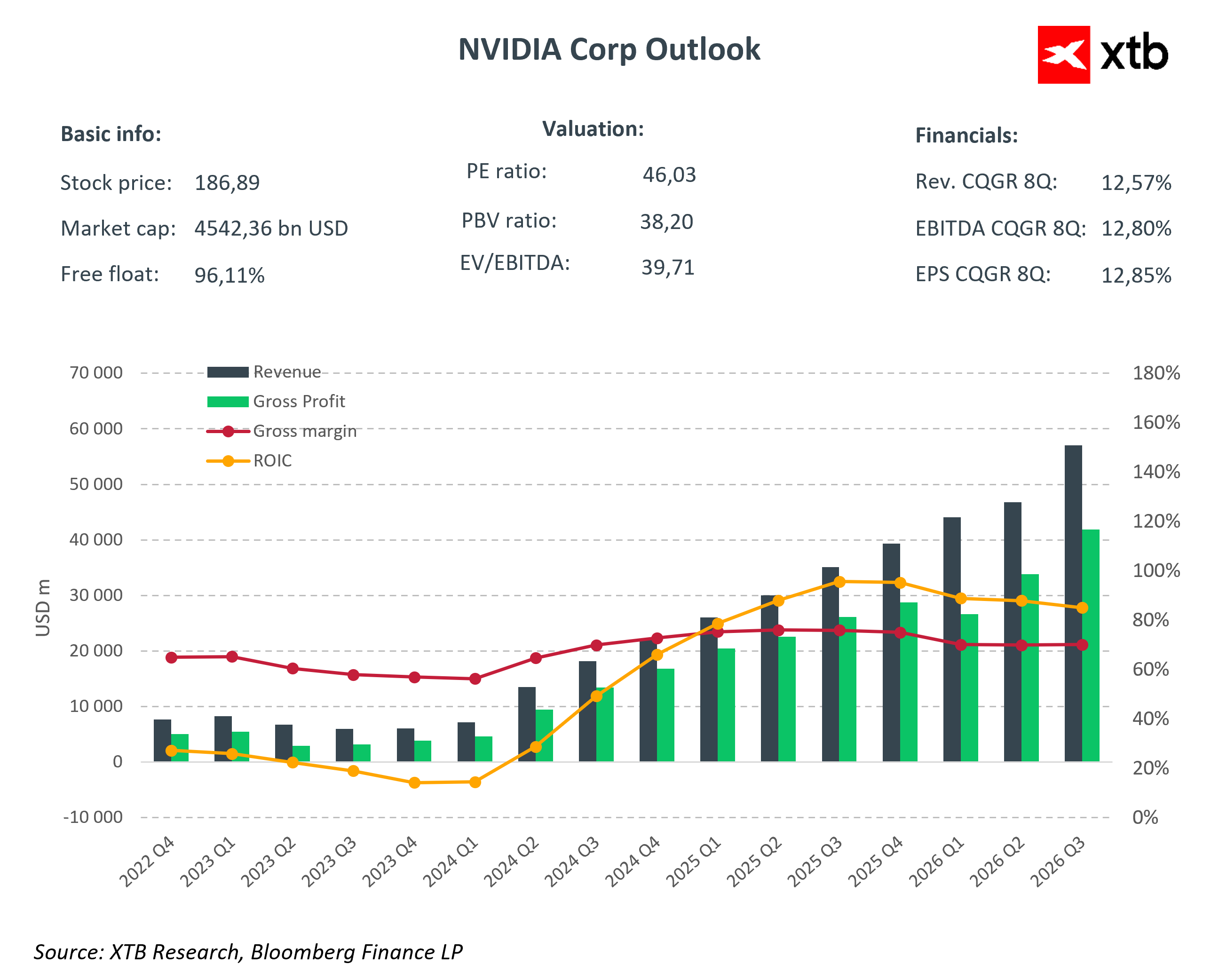

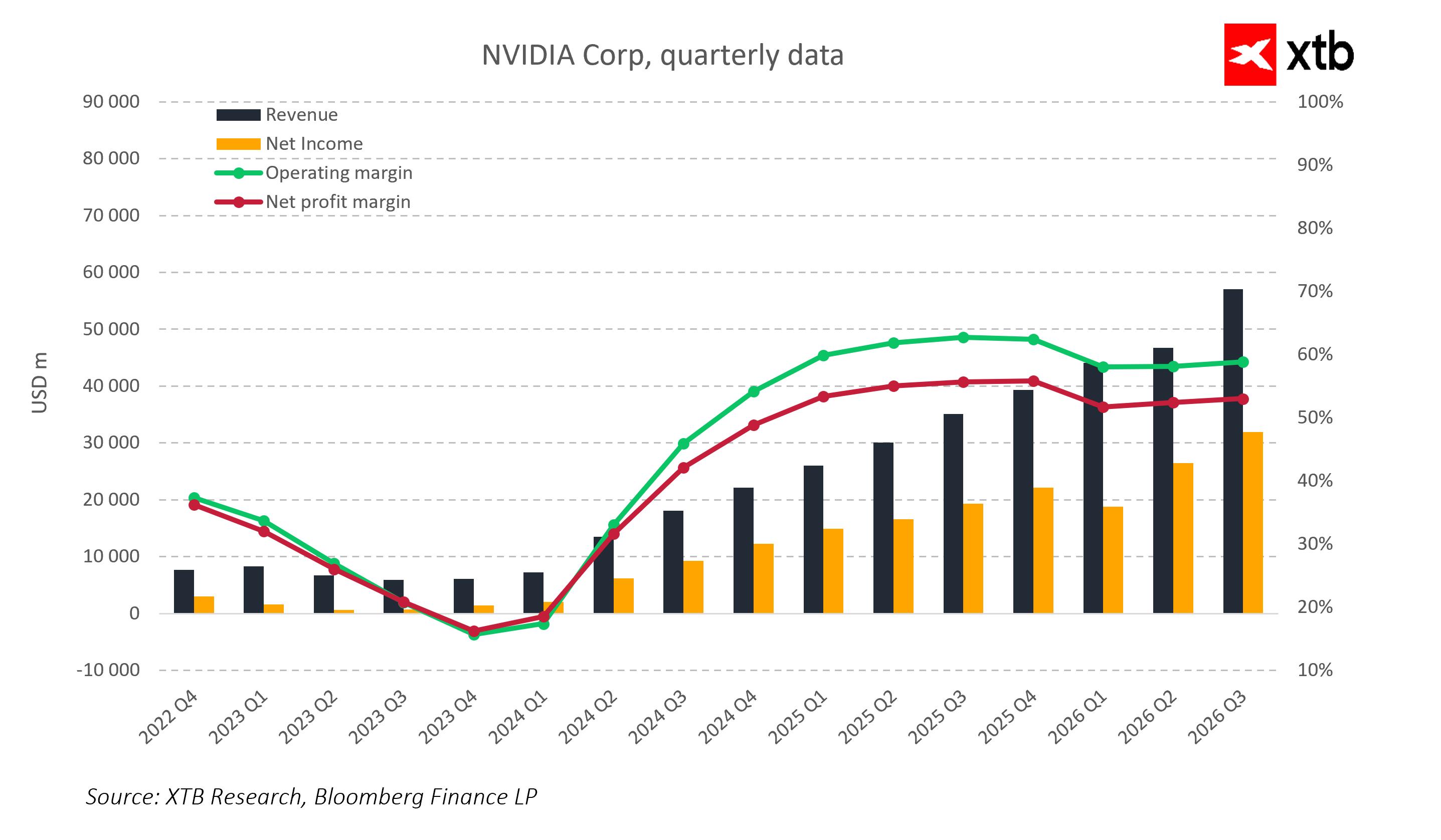

2026 Q4 Revenue: 65 billion to $66 billion, compared to $39.33 billion last year. This represents 66-67% year-over-year growth due to accelerated AI adoption and increased hyperscaler orders.

-

Adjusted EPS: $1.50 to $1.53, compared to $0.89 last year. The market expects to see solid profitability despite rising investment levels.

-

2027 Q1 Guidance: This represents continued growth of approximately 64% year over year and provides insight into whether the “peak AI” story will continue next year.

-

Historical background: Nvidia has exceeded revenue estimates for 13 consecutive quarters and exceeded EPS for 12 consecutive quarters, setting a very high bar.

what is really important

Data center and AI

The data center division is central to Nvidia’s strategy. Revenue growth in this segment is not solely driven by the demand for gaming GPUs, but is primarily driving the AI business. Investors will analyze the pace of Blackwell and H200 deployments, number of deployments in hyperscaler data centers, and training and inference revenue sharing. This will help assess whether GPUs will create a stable demand cycle that can continue for years to come, and whether a product pipeline that includes projects like Vera Rubin will provide a competitive advantage from 2026 to 2028.

Blackwell and H200 in China

H200 could generate revenue of $3-3.5 billion per quarter. This is important because the Chinese market remains an important source of revenue. The pace of adoption of these chips and the impact of export restrictions demonstrate the extent to which geopolitical factors may limit revenue growth and impact NVIDIA’s global strategy.

Margin and component costs

Gross profit margins have hovered around 73% to 74% in previous quarters, and management has indicated a goal of maintaining it in the mid-70% range. The consensus is that despite HBM Memory’s rising costs and capacity expansion, the company expects it to maintain very high profit margins, in part due to long-term parts contracts. Investors will be scrutinizing commentary on product mix, discount levels for key customers, the impact of new generation GPUs on profits, and more.

Hyperscaler capital investment and business expansion

Increased spending by Amazon, Google, Microsoft, and Meta signals confidence in AI’s long-term potential, but also poses challenges for Nvidia’s profitability. Investors will be watching whether the company can grow revenue while maintaining high gross and operating margins, and how effectively it can manage costs as demand grows rapidly.

Market reaction scenario

Nvidia’s report will be taken as a barometer for the entire AI and semiconductor market, not just the results of one company. NVDA has consistently exceeded expectations for 13 consecutive quarters, and expectations are sky high. Even strong performance may be viewed as neutral if guidance and management commentary falls short of market expectations.

In a positive scenario, which implies strong revenue and EPS improvements, a better-than-expected 2027 outlook, and an earlier-than-expected introduction of Blackwell and H200 in China, we expect a dynamic reaction across the semiconductor sector. A rise in NVDA will likely benefit competitors and create positive sentiment for technology ETFs and indexes like the S&P 500. This strengthens the narrative of a sustained AI boom and could prompt institutional investors to increase their allocations to AI and data center companies.

In a neutral scenario, market reaction is likely to be muted. Results in line with expectations and stable guidance for 2027 probably won’t trigger strong price action or significantly change sentiment across the sector. This report confirms the existing growth trajectory without providing further stimulus for aggressive buying or profit-taking, and NVIDIA’s stock price should remain stable in line with its competitors and major indexes.

In a negative scenario, disappointing sales and EPS, weak guidance, delayed introduction of Blackwell and H200 in China, and margin pressure could trigger a correction in the broader semiconductor market. NVDA will likely fall, impacting its competitors, ETFs, and technology indexes including the S&P 500. Enthusiasm for AI may cool, and investors may adopt a more conservative view of the sector’s growth prospects in coming quarters.

Whatever the scenario, Nvidia’s report will increase short-term market volatility. Any nuance in management’s comments on demand, hyperscaler capital expenditures, margins, or the situation in China will be carefully analyzed and could cause significant price movements.

Important points

-

Nvidia will play a role in testing the durability of the AI boom and the scalability of GPUs in data centers.

-

The report will show whether hyperscaler spending translates into real revenue and whether demand for Blackwell and H200 remains stable, including in China.

-

Margins and management commentary on inference and training will reveal whether GPU demand remains strong over the next few years.

-

Guidance for 2026 and 2027 will indicate whether the “AI peak in 2026” thesis is justified or whether investors need to adjust their expectations.

-

NVDA’s results will impact sentiment across the semiconductor sector, the S&P 500, and technology and AI.

-

Management’s comments regarding the pace of H200 implementation in China and export restrictions could lead to further volatility.

-

This report tests Nvidia’s ability to effectively scale AI investments while maintaining high profitability and competitive advantage.

The contents of this report have been prepared by XTB SA, registered office in Warsaw, Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by the Polish Supervisory Board (No. DDM-M-4021-57-1/2005). This material is a marketing communication in the sense of art. Article 24(3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amendments to Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). The marketing communications are not information that recommends or suggests investment recommendations or investment strategies within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuses and of the European Parliament and of the Council, Repealing Directive 2003/6/EC and of the European Commission Directive 2003/124/EC. 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016, Regulation (EU) No. 596/2014. Other advice within the meaning of the Financial Instruments and Exchange Act of July 29, 2005 (i.e., Journal of Laws 2019, No. 875, as amended), including in the field of investment advisors. Marketing communications are prepared with the utmost diligence and objectivity, present the facts known to the authors on the date of their creation, and are free of any evaluation elements. Marketing communications are prepared without taking into account the client’s needs or personal financial situation and do not present any investment strategy. Marketing Communications do not constitute a sale, offer, offer to subscribe, solicitation of an offer to buy, advertisement, or promotion of any financial product. XTB SA is not responsible for any actions or omissions of the Customer based on the information contained in this marketing communication, in particular for the acquisition or disposal of financial instruments. Even if marketing communications contain information regarding the performance of financial products, they do not constitute any guarantee or prediction of future performance.