AI essentially forms the semiconductor industry, and is the most important variable in this semiconductor cycle.

According to Hard AI News, in just five years, AI-related sales accounted for more than 25% of the overall semiconductor market, driving the first acceleration of the semiconductor industry's growth in 25 years.

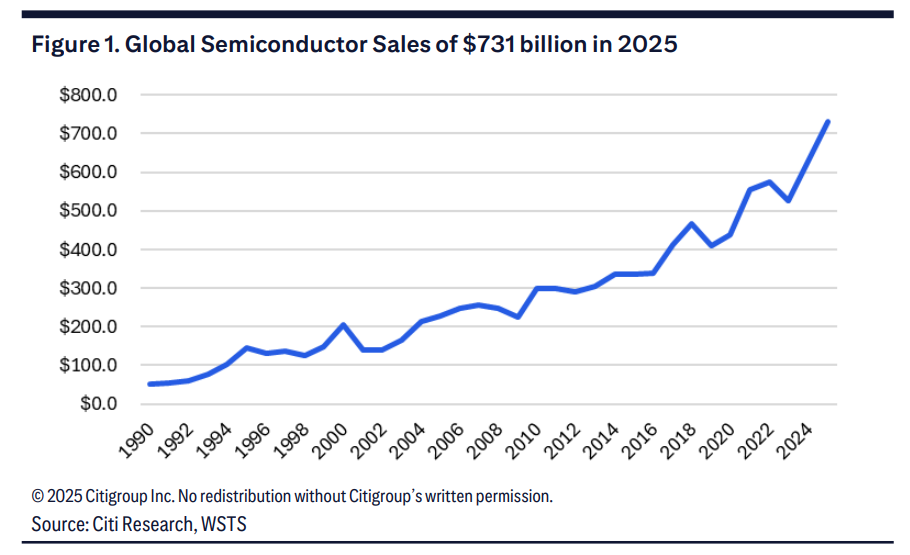

City analyst Christopher Denary is expected to reach a new historic high, with global semiconductor sales expected to rise 16% to US$731 billion in 2025, but this revenue growth has been driven entirely by price increases, with shipments still far below their peak. This phenomenon indicates low inventory levels and suggests ample room for further growth within the industry.

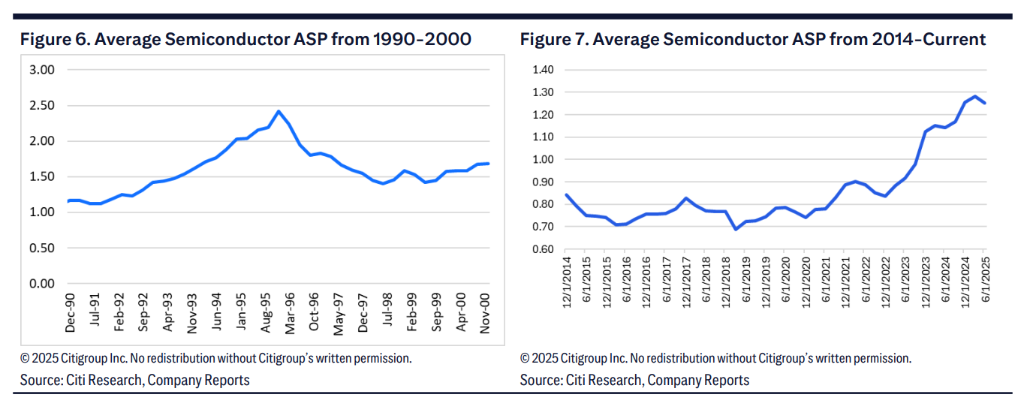

The average price for semiconductors has risen from around USD 0.72 in 2019 to around USD 1.26 in 2025, indicating a 75% increase. Since 2022, prices have risen 45%, marking the biggest increase in 30 years. This continuous four-year price rise is the first occurrence since 1992-1995.

Citi predicts that AI data centre's share of semiconductor sales will increase from under 5% in 2022 to about 27% in 2025, reaching an additional 40% by 2028. Due to AI demand, the semiconductor industry's revenue growth rate is expected to increase from 7% to 10% from its historic average.

AI-driven semiconductor pricing reaches 30 years' high

Citi data shows that current growth in semiconductor industry revenues is driven primarily by rising prices for logic chips.

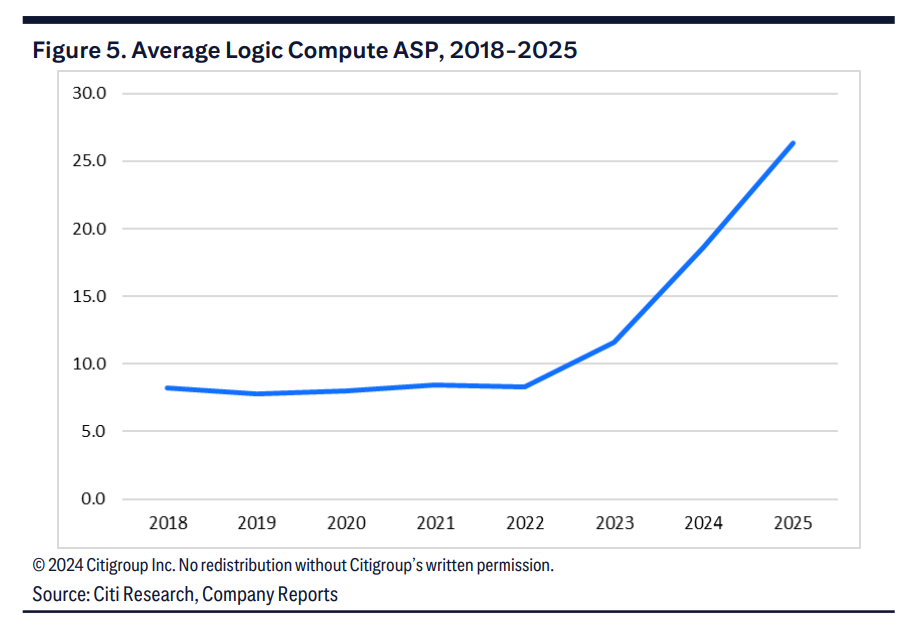

Citi said the average price of logic computing chips (including AI accelerators) has increased 24% over the past three years, far surpassing the 2% growth seen in the past decade. The share of logic computing chips in total semiconductor sales also increased from 27% in 2020 to 39% in 2025.

Among these, logic computing revenues have grown rapidly at a combined annual growth rate (CAGR) of 53%, up from around US$29.6 billion in 2022 to US$106.4 billion by 2025, with semiconductor sales increasing from 5% to 15%.

The average price of logic computing chips has skyrocketed from 7.80-8.50 between 2018 and 2022 to the expected US$26.40 for 2025, reflecting a combined annual growth rate of 47%.

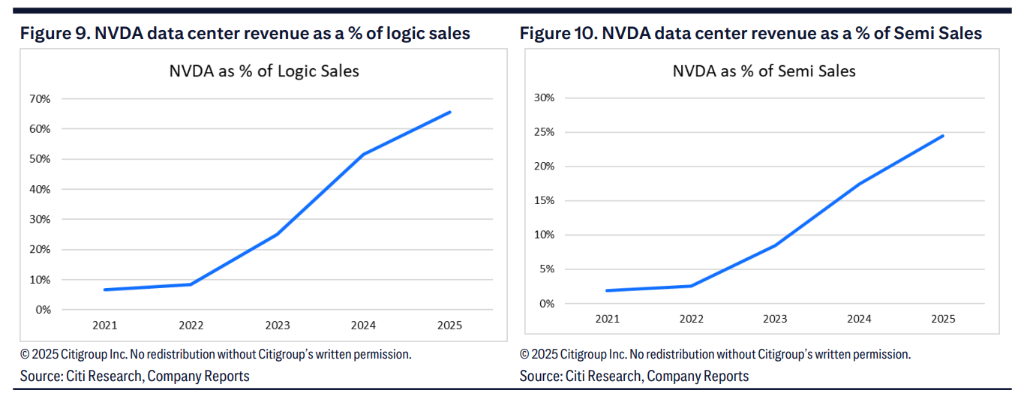

Citi said the rapid expansion of Nvidia's data center business is a key factor in this change. The share of logic chip sales due to this business has skyrocketed from under 10% in 2021 to 66% by 2025, while the share of total semiconductor sales has increased from under 3% in 2021 to 24%.

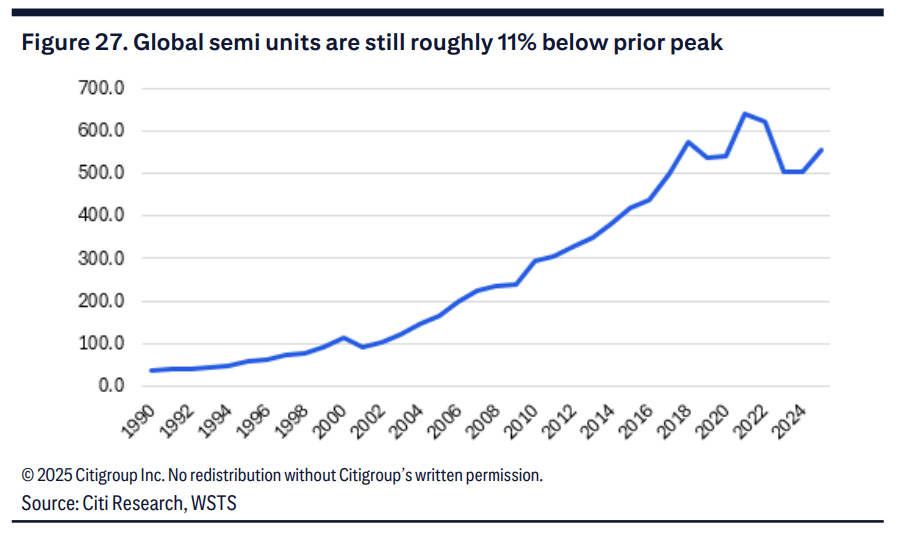

Shipping volumes are below peak levels and stock levels are still low.

Despite record revenue, Citi analysis shows that there is still room for growth in semiconductor shipments.

Current total semiconductor shipments are about 11% below previous peak levels, increasing just 18% during current upcycles, much lower than the historical average growth rate of 60%.

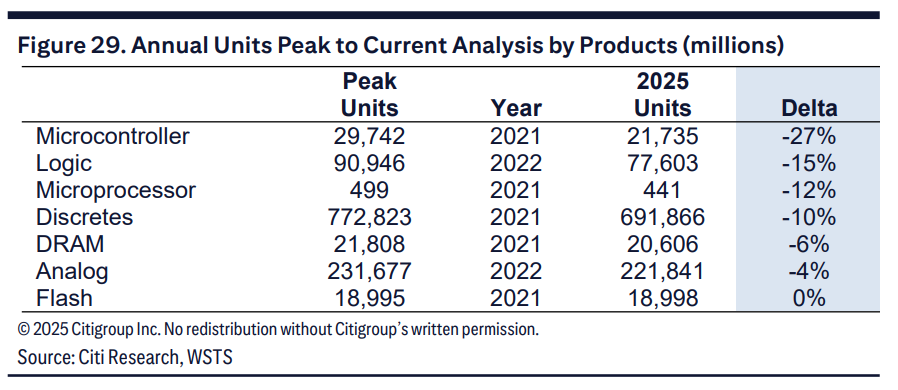

In the product category, microcontroller shipments are still 27% below the 2021 peak, with logic computing chips down 15% and microprocessors down 12%.

Citi believes the current shipment-peak gap indicates low levels of supply chain inventory, leaving plenty of room for future growth.

Citi analysts said that in an industry with an average peak-to-peak unit growth rate of 50%, the current 11% shipping gap “gives confidence that this cycle still has important potential.”

Gross profits show clear divergence, and most companies still have room for improvement.

An analysis by 18 CITIs shows that the industry's gross profits are being significantly diverged.

Data show that the weighted average total margin reached 59% in the second quarter of 2025. This is close to the 60% peak level seen in the fourth quarter of 2024, but this was driven primarily by the gross profits of Nvidia and Broadcom.

When calculated using a simple average, the total margin is only 52%, which is significantly lower than the historical peak.

The total margins of target companies averaged 7.8% below their respective peaks, indicating the largest gap from the total margin peaks of 18.7%, 14.5% and 12.8%, respectively.

Of the 18 companies, eight have gross profits of more than 10% than their peak, while nine have operating profit margins of 10% below their peak. Citi believes it shows that there is still room for margin expansion as the semiconductor cycle progresses.

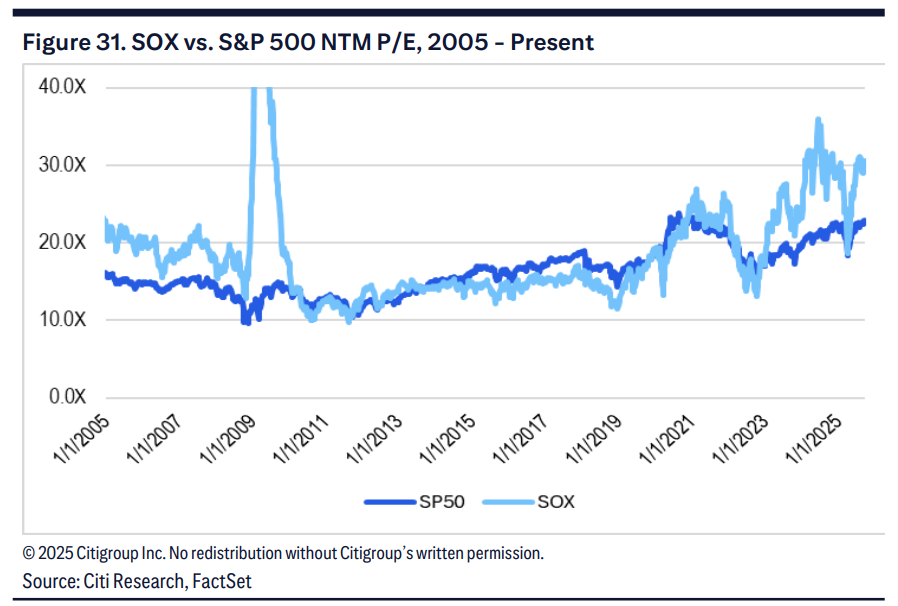

Justified rating premium. AI effects support high growth.

Semiconductor Index Sox is currently trading at 31x at a forward price-to-earning ratio, representing a 34% premium over the S&P 500 index, but Citi considers this valuation level to be reasonable.

Since the release of ChatGPT in November 2022, SOX has averaged 31% premium over the S&P 500.

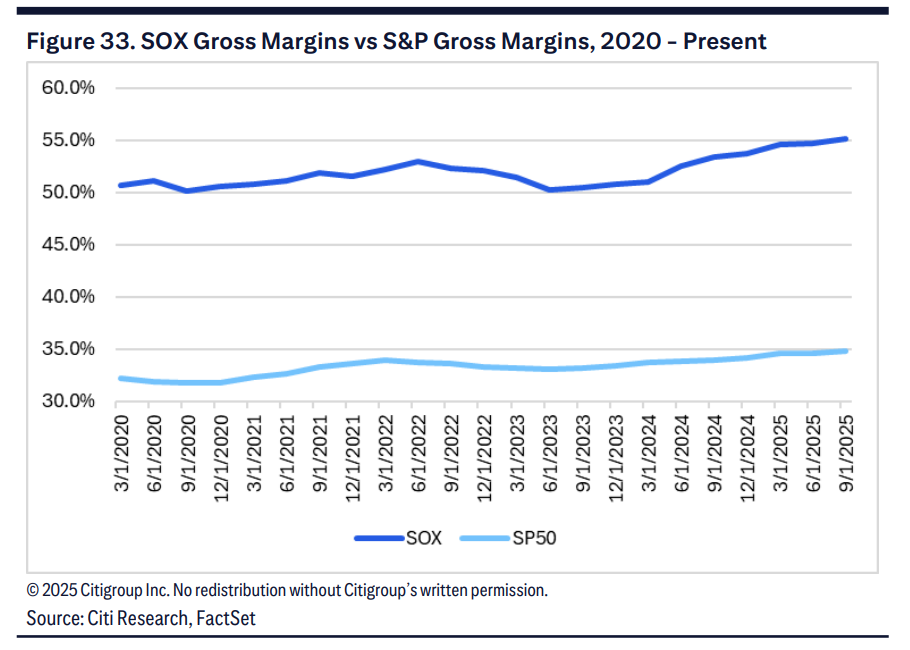

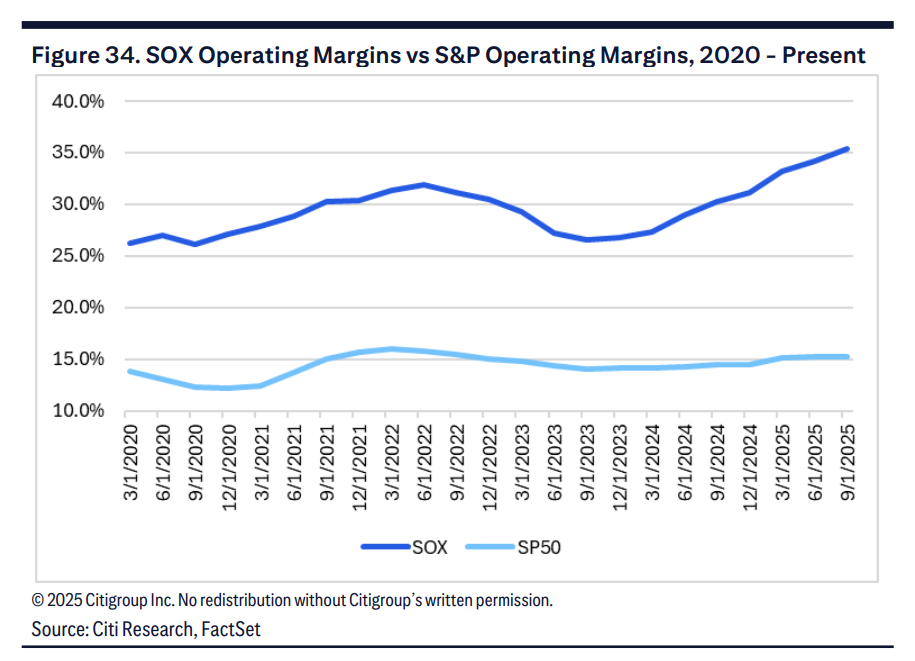

Citi emphasized that the semiconductor industry boasts a total margin of over 50% and over 25%. This means that the total margin of the S&P 500 is 30%-35% and the operating profit margin is 10%-15%.

From a growth perspective, the semiconductor industry surpasses the S&P 500 over a three-, five- and ten-year perspective.

Regression analysis shows that the operating margin, excluding stock-based compensation, is the biggest factor in the valuation, explaining 66% of the fluctuations in forward price to sales ratios.

Citi hopes that overall semiconductor demand will remain strong as long as the AI cycle continues and will support the industry's valuation premium.