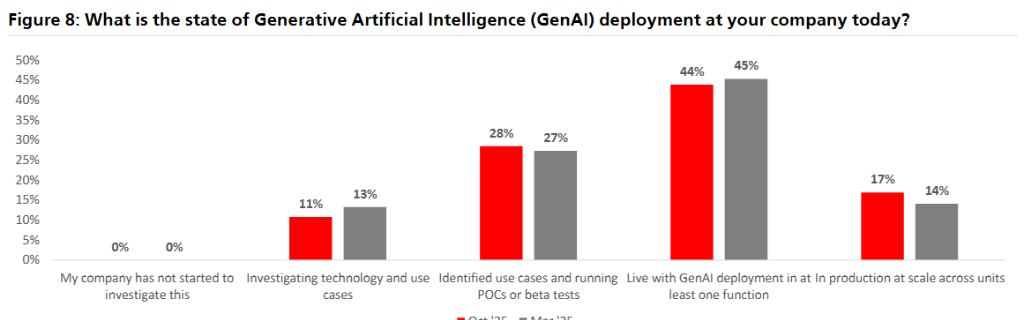

Despite the growing momentum in artificial intelligence (AI) technology, large-scale adoption of enterprise-level AI applications has been slow. A recent study by UBS Group found that only 17% of companies surveyed had achieved full-scale implementation of their AI projects, up slightly from 14% in March this year. As many as 60% of companies choose to develop AI applications in-house rather than purchasing off-the-shelf third-party solutions. The much-talked-about “AI agent” technology is currently being deployed at scale by only 5% of companies. The study also found that the introduction of AI applications has not led to widespread layoffs, with 40% of companies surveyed saying AI will drive job growth.

Despite continued advances in artificial intelligence (AI) technology, large-scale adoption of enterprise-level AI applications has been slow.

According to data from Zhui Feng Trading Desk, the latest 5th Corporate AI Survey, published by Karl Kjerstedt's team at UBS Group, found that only 17% of companies surveyed had achieved large-scale production implementation of their AI projects, up slightly from 14% in March this year.

Even more remarkable, as many as 60% of companies are choosing to develop their own AI applications rather than purchasing a third-party finished product. The much-talked-about “AI agent” technology is currently being deployed at scale by only 5% of companies.

Even more remarkable, as many as 60% of companies are choosing to develop their own AI applications rather than purchasing a third-party finished product. The much-talked-about “AI agent” technology is currently being deployed at scale by only 5% of companies.

The survey results show that Microsoft, OpenAI, and NVIDIA continue to dominate the enterprise AI market. In cloud infrastructure, Microsoft Azure maintains its leadership. Among large-scale language models, OpenAI's GPT series holds three of the top five spots, but Google Gemini and Anthropic Claude are quickly catching up. Microsoft's M365 Copilot remains the preferred enterprise-level AI tool, but OpenAI's ChatGPT Business Edition is rapidly closing the gap.

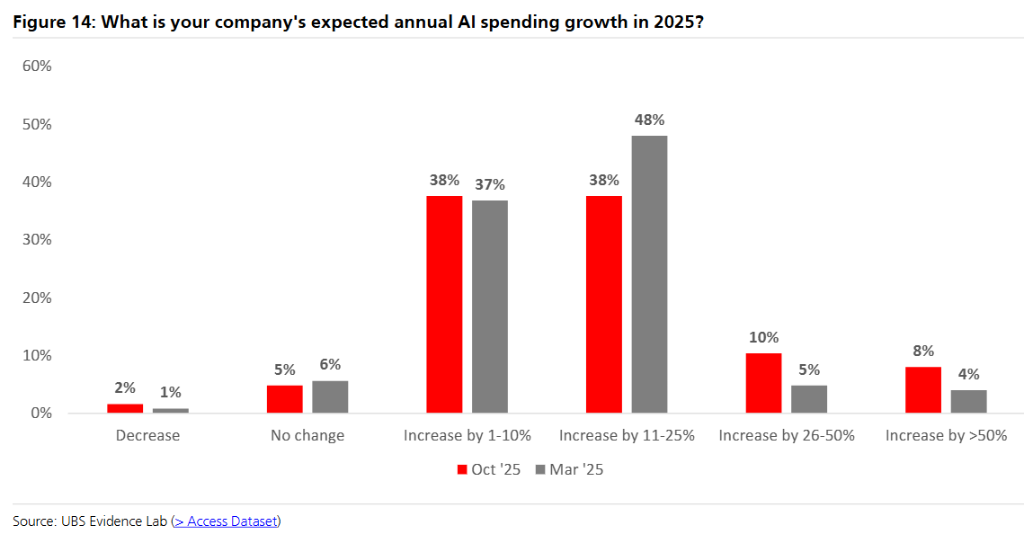

The survey was conducted in October 2025 and surveyed IT executives at 130 companies with an average of 8,200 employees and approximately $800 million in IT budgets. This research uncovers the key challenges businesses face in implementing AI. 59% of respondents believe that uncertain return on investment (ROI) is the biggest barrier, up significantly from 50% in March of this year. Concerns about compliance regulations (45%) and lack of in-house expertise (43%) rank second and third, respectively.

The study also found that the introduction of AI has not led to large-scale layoffs. 40% of companies surveyed say AI will drive employee growth, but only 31% of companies expect to reduce their workforce, and only 1% of companies expect significant layoffs. This finding is advantageous for seat-based SaaS companies, alleviating market concerns about AI replacing human labor.

In-house development of AI becomes mainstream

The most notable finding from this study is that companies prefer procurement models for AI applications. While only 34% of companies surveyed reported relying entirely on AI products from third-party software vendors, up to 60% are opting for complete in-house development or a hybrid approach that combines in-house and sourcing.

This trend poses a challenge for traditional software vendors. SaaS companies have long believed that as the complexity of AI applications increases, companies will eventually move toward purchasing off-the-shelf solutions. However, research shows that this transition has not yet occurred.

Analysts at UBS noted that the popularity of “DIY AI” models is creating new opportunities for AI model providers such as OpenAI and Anthropic. These companies can enter the enterprise AI application market by selling their “models + tools” platform to companies that prefer the build-it-yourself route.

For certain application scenarios, the demand for AI deployment in internal IT help desks (75%) is significantly higher than in external customer support (52%). ServiceNow maintains its leadership in AI solutions that automate internal IT workflows, even surpassing Salesforce in the ranking of CRM AI technology providers, which is a surprising result.

Deployment of AI agents is still in its early stages.

Although AI agents are seen as the next important development direction, enterprise-level adoption is still in its infancy. According to the study, only 5% of companies have achieved large-scale production deployments of AI agents, 71% are in pilot or small-scale operations, and the remaining 22% have not started pilots yet.

This result contrasts with the optimistic forecasts of companies such as OpenAI and Anthropic regarding the market outlook for AI agents. These companies see AI agents as a key breakthrough for deeper penetration into the enterprise market and expect this technology to generate significant revenue and GPU consumption.

UBS Group believes that the delay in agent implementation supports its view that AI agents will not replace human labor on a large scale, and also serves as a reminder for investors to maintain reasonable short-term return expectations for relevant technology suppliers.

Analysts have suggested that the vision of big revenue growth from agents envisioned by many AI technology suppliers may not materialize until 2027 or later, as companies often adopt new technologies more slowly than expected.

The partnership between Microsoft and OpenAI remains strong.

Amid fierce competition in AI models, OpenAI continues to maintain its leading position in the enterprise market. Its GPT 5.0, 4.0, and 3.5 models occupy three of the top five for enterprise users, with ChatGPT 4.0 ranking first.

Notably, despite market rumors that “large-scale language models are becoming commoditized” and that Google is surpassing OpenAI at the model level, the findings show that OpenAI's position in the enterprise market remains strong. But competition is heating up, with Google Gemini's adoption rate jumping from 19% last May to 46%, and Anthropic Claude moving into third place.

In the general-purpose AI tools space, Microsoft M365 Copilot maintains its dominance, but OpenAI ChatGPT Business Edition is quickly emerging as the second most popular option. If you combine all enterprise versions of ChatGPT, its overall popularity could already rival M365 Copilot.

According to the survey, interviewed companies have an average of 2,050 paid M365 Copilot seats, a steady increase from 1,715 seats in March, representing 67% year-over-year growth. The average number of ChatGPT seats for a company is about 995, which is about half that of Copilot.

Data software vendors have benefited greatly.

AI projects are showing a clear pull effect on data infrastructure demand. Across the various data software categories, the percentage of respondents expecting spending increases (52% on average) is much higher than the percentage expecting budget cuts (10% on average).

The cloud data warehousing sector will benefit the most, with 69% of respondents expecting an increase in related spending and 25% expecting significant growth. This trend is favorable for vendors such as Snowflake, AWS Redshift, and Google BigQuery. When it comes to choosing a specific vendor, Snowflake has a slight lead, with Databricks following closely behind, indicating increased competition.

The cloud data lake and ML/AIOps sectors are also performing well, with 56% and 60% of respondents expecting spending to increase, respectively. In contrast, the growth in AI-enabled operational databases (MongoDB, Oracle, etc.) has been relatively modest, with only 10% of respondents expecting a significant increase in related spending.

UBS Group believes this difference reflects the current focus of AI applications on analytics and machine learning workloads rather than more complex transaction processing applications. As companies build more sophisticated “second generation” AI applications, the demand for operational databases is likely to increase significantly.